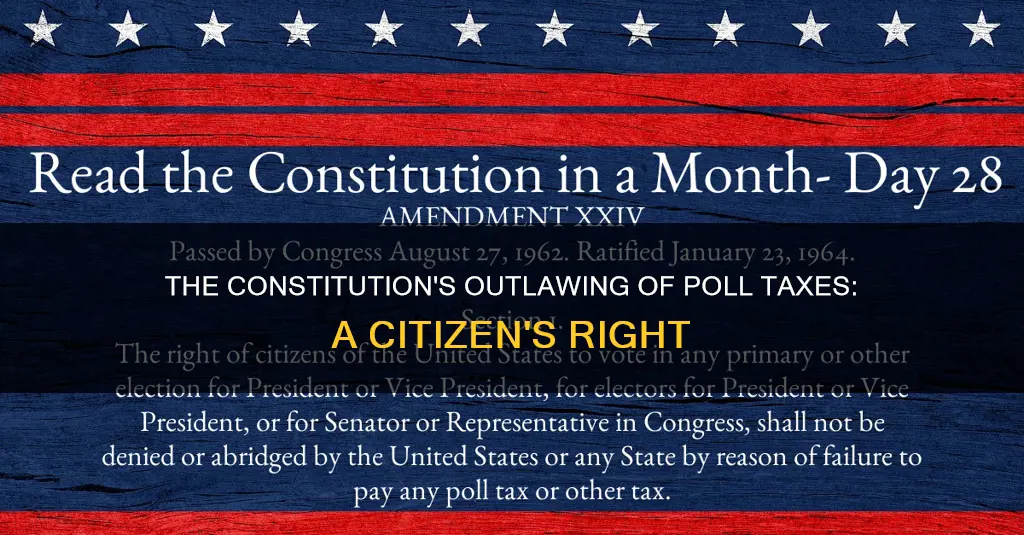

The 24th Amendment to the US Constitution outlaws poll taxes, which had been used to prevent African Americans and poor whites from voting. The Amendment was ratified in 1964 and abolished the use of poll taxes as a pre-condition for voting in federal elections. The official text of the Amendment states that the right of US citizens to vote shall not be denied or abridged...by reason of failure to pay poll tax or other tax. The 1965 Voting Rights Act further eliminated all forms of discrimination in voting, making it a constitutional right for all American men and women for the first time in history.

| Characteristics | Values |

|---|---|

| Date of Amendment | 23 January 1964 |

| Amendment Number | 24th Amendment |

| What it Outlaws | Poll taxes |

| Type of Amendment | Abolition of poll taxes |

| What it States | The right of citizens of the United States to vote in any primary or other election shall not be denied or abridged by the United States or any State by reason of failure to pay poll tax or other tax |

| Powers Granted | The Congress shall have the power to enforce this article by appropriate legislation |

| Affected States | Alabama, Arkansas, Mississippi, Texas, and Virginia |

| Affected Groups | African Americans and poor whites |

| Previous Poll Tax Amounts | $1 in Georgia, $1.50-$1.75 in Texas, $2.00 in Mississippi |

Explore related products

What You'll Learn

![]()

The 24th Amendment

> "The right of citizens of the United States to vote in any primary or other election for President or Vice President, for electors for President or Vice President, or for Senator or Representative in Congress, shall not be denied or abridged by the United States or any State by reason of failure to pay poll tax or other tax. The Congress shall have power to enforce this article by appropriate legislation."

Even after the 24th Amendment was ratified, several states continued to impose poll taxes in violation of the new law. It was not until the 1966 Supreme Court decision Harper v. Virginia Board of Elections that poll taxes were completely eliminated, with the Court ruling that poll taxes in all elections—federal, state, and local—were unconstitutional. This ruling was followed by the Voting Rights Act of 1965, which made it enforceable by law and eliminated all forms of discrimination in voting, making voting a Constitutional right for all American men and women.

The Constitution's Eighth Amendment: Unfair Punishments and Their Illegality

You may want to see also

Explore related products

![]()

Poll tax as a prerequisite for registration to vote

The poll tax was a prerequisite for registration to vote in several states in the United States until 1965. The tax was introduced in some states in the late 19th century as part of the Jim Crow laws, following the end of Reconstruction. This was after the Fifteenth Amendment had granted the right to vote to all American men, and the new laws were designed to restrict voting rights.

The poll tax required voters to pay a fee to enter polling places to cast their ballots. This disproportionately affected African Americans in the Southern states, where there were higher levels of poverty, as well as poor Whites. The laws often included a "grandfather clause", which allowed any adult male whose father or grandfather had voted in a specific year prior to the abolition of slavery to vote without paying the tax. This was designed to exclude African-Americans, as well as Native and Asian-American voters, from voting.

The poll tax was also used in conjunction with other methods of intimidation and violence, such as by the Ku Klux Klan, to prevent people from voting. The tax was imposed by Southern states of the former Confederate States of America, and it was adopted into both their state laws and constitutions throughout the late 19th and early 20th centuries.

The 24th Amendment, ratified in 1964, abolished the use of the poll tax as a pre-condition for voting in federal elections. However, it did not mention state elections. The Voting Rights Act of 1965 helped to outlaw the practice nationwide, and it was enforced by law. The 1966 Supreme Court case Harper v. Virginia Board of Elections ruled that poll taxes in all elections were unconstitutional, and this finally eliminated poll taxes in the United States.

The Constitution's Clause on Presidential Term Limits

You may want to see also

Explore related products

![]()

Poll tax laws as a device for restricting voting rights

Poll tax laws were used in the United States as a device for restricting voting rights, particularly for African Americans, Asian Americans, Native Americans, and poor whites. The tax emerged in some states in the late 19th century as part of the Jim Crow laws, following the end of the Reconstruction Era. During this period, states across the former Confederacy imposed a series of laws that restricted the civil liberties of African Americans, who had recently been granted the right to vote through the Fifteenth Amendment.

Poll taxes required voters to pay a fee to enter polling places and cast their ballots. The amount of the tax was typically fixed, regardless of the individual's income. For example, the Texas poll tax was between $1.50 and $1.75, which was considered a significant amount of money at the time and created a barrier for the working classes and the poor. Georgia had a cumulative poll tax requirement, where men aged 21 to 60 had to pay a sum of money for every year since they turned 21 or since the law took effect.

The poll tax, along with other methods such as unfairly administered literacy tests and extra-legal intimidation, effectively disenfranchised many voters. While the laws that allowed the poll tax did not specify a particular group, they were crafted with discriminatory intent to exclude African Americans from voting due to their higher levels of poverty in the Southern states. Additionally, these laws often included "grandfather clauses," which allowed white males whose ancestors had voted before the abolition of slavery to vote without paying the tax, further perpetuating racial disparities in voting rights.

The 1937 Supreme Court case of Breedlove v. Suttles upheld the constitutionality of poll taxes, but a wave of criticism emerged during the Roosevelt Administration of the 1930s and 1940s. President Franklin D. Roosevelt publicly opposed the tax, calling it "a remnant of the Revolutionary period." However, his efforts to abolish the poll tax through legislation were blocked by conservative Southern Democrats. The debate around the poll tax continued, and in 1948, President Harry S. Truman's Committee on Civil Rights investigated the issue, concluding that a constitutional amendment might be necessary to abolish it.

Finally, in 1964, the Twenty-fourth Amendment to the United States Constitution was ratified, abolishing the use of poll taxes in federal elections. However, several states continued to maintain their poll taxes in opposition to the new law. It was not until 1966 that the Supreme Court, in Harper v. Virginia Board of Elections, ruled that poll taxes were unconstitutional in all elections, including federal, state, and local ones. This ruling, along with the Voting Rights Act of 1965, which eliminated all forms of discrimination in voting, marked a significant step in the pursuit of civil rights and ended the use of poll taxes as a device for restricting voting rights in the United States.

Pledge of Allegiance: Is 'Under God' Unconstitutional?

You may want to see also

Explore related products

![]()

The Voting Rights Act of 1965

The Act included several key provisions to protect voting rights. Section 2, which closely followed the language of the Fifteenth Amendment, applied a nationwide prohibition of the denial or abridgment of the right to vote on account of race or color. Section 4 contained several provisions, such as Sections 4(e) and 4(f), that guaranteed the right to register and vote for those with limited English proficiency. Section 5 required covered jurisdictions to obtain "preclearance" from the District Court for the District of Columbia or the U.S. Attorney General for any new voting practices and procedures.

McCulloch v Maryland: Confirming the Supremacy Clause

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

Harper v. Virginia Board of Elections

In the case of Harper v. Virginia Board of Elections (1966), the U.S. Supreme Court ruled that Virginia's poll tax was unconstitutional. The case was filed by Virginia resident Annie E. Harper, who, along with other poor residents, was unable to register to vote without paying a poll tax.

The poll tax in Virginia was established in the state's revised constitution of 1902. It was part of a movement among former Confederate states to disenfranchise African Americans through a combination of poll taxes and literacy tests. By 1964, most states had decided to eliminate poll taxes, but Virginia, Alabama, Mississippi, and Texas continued to impose them for state and local elections.

The decision closed a loophole in the 24th Amendment, which had abolished poll taxes for federal elections but did not address poll taxes for state and local elections. With this ruling, the Supreme Court officially banned the use of poll taxes in any type of election, ensuring that the right to vote was protected for all citizens regardless of their financial status.

The Constitution's Guide to Dealing with Terrorism

You may want to see also

Frequently asked questions

A poll tax is a tax of a fixed sum on every liable individual, typically every adult, without reference to income or resources.

The poll tax was used as a tool to prevent African Americans and poor whites from voting.

Poll taxes required voters to pay a fee to enter polling places to cast their ballots.

The Twenty-fourth Amendment to the Constitution, ratified on January 23, 1964, abolished poll taxes.

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)