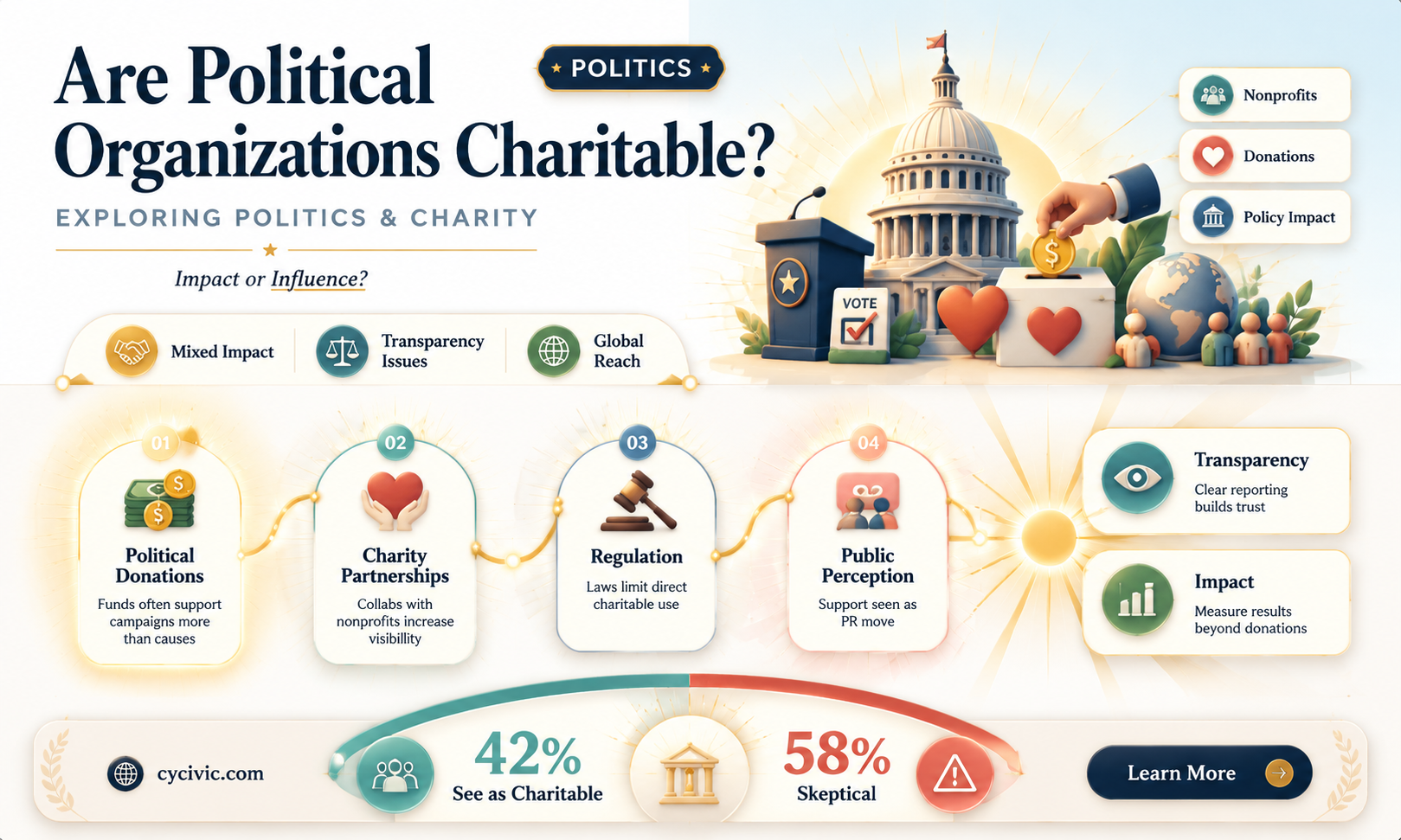

The question of whether political organizations can be considered charitable is a complex and contentious issue, as it intersects with legal, ethical, and societal norms. While charitable organizations are typically defined by their focus on alleviating suffering, advancing education, or promoting public welfare, political groups primarily aim to influence government policies, elections, or public opinion. In many jurisdictions, charitable status confers tax benefits and regulatory advantages, but these are often restricted to entities that avoid partisan political activities. Critics argue that allowing political organizations to claim charitable status could blur the lines between advocacy and public service, potentially undermining the integrity of both charitable work and democratic processes. Conversely, proponents contend that certain political activities, such as voter education or advocacy for systemic change, can align with charitable goals. Ultimately, the classification depends on how narrowly or broadly one defines charity and the extent to which political engagement is deemed to serve the public good.

| Characteristics | Values |

|---|---|

| Tax-Exempt Status | Political organizations are generally not eligible for tax exemption under section 501(c)(3) of the U.S. Internal Revenue Code, which is reserved for charitable, religious, educational, and other qualifying purposes. Instead, they may qualify under 501(c)(4) as social welfare organizations, but this does not grant donors tax deductions for contributions. |

| Primary Purpose | Political organizations primarily focus on influencing legislation, elections, or public policy, whereas charitable organizations aim to provide public benefit through education, poverty relief, health, or other charitable activities. |

| Donor Disclosure | Political organizations (especially 501(c)(4)s) often have less stringent donor disclosure requirements compared to charities, allowing for anonymous contributions in some cases. |

| Lobbying Activities | Political organizations can engage in unlimited lobbying as their primary activity, while charitable organizations (501(c)(3)s) face strict limits on lobbying to maintain tax-exempt status. |

| Campaign Intervention | Political organizations may directly participate in political campaigns and endorse candidates, whereas charitable organizations are prohibited from such activities to avoid jeopardizing their tax-exempt status. |

| Public Perception | Political organizations are often viewed as partisan or advocacy-driven, while charitable organizations are perceived as neutral and focused on public welfare. |

| Funding Sources | Political organizations rely heavily on donations from individuals, corporations, or PACs, often with fewer restrictions, whereas charitable organizations depend on tax-deductible donations, grants, and public funding. |

| Regulatory Oversight | Political organizations are regulated by the FEC (Federal Election Commission) and IRS, while charitable organizations are primarily overseen by the IRS and state charity regulators. |

| Global Perspective | In many countries, political organizations are not considered charitable and are subject to separate legal frameworks, though some nations allow limited charitable status for non-partisan political education efforts. |

| Transparency Requirements | Political organizations often face lower transparency standards compared to charities, which are required to disclose financials and activities publicly. |

Explore related products

$25.1 $29.95

What You'll Learn

- Legal Definitions: Distinguishing charitable vs. political activities under tax laws and regulatory frameworks

- Lobbying Limits: Rules governing charitable organizations' engagement in political advocacy or lobbying efforts

- Campaign Involvement: Restrictions on charities supporting or opposing political candidates or parties

- Public Perception: How political ties impact public trust and donor confidence in charitable organizations

- Funding Sources: Transparency requirements for charitable organizations receiving political or government funding

![]()

Legal Definitions: Distinguishing charitable vs. political activities under tax laws and regulatory frameworks

Tax laws and regulatory frameworks meticulously delineate charitable and political activities, a distinction critical for organizations seeking tax-exempt status. Charitable activities, as defined by the IRS under Section 501(c)(3), must serve public interests in areas like education, religion, science, or poverty relief. Political activities, conversely, involve influencing legislation or supporting candidates, which can jeopardize charitable status if they become a substantial part of an organization’s operations. For instance, a nonprofit advocating for environmental policy changes must ensure such advocacy remains secondary to its charitable mission, such as educating the public about conservation.

Distinguishing these activities requires a nuanced understanding of regulatory boundaries. The IRS employs the "facts and circumstances" test to evaluate whether an organization’s actions align with charitable purposes. For example, voter education campaigns are permissible if nonpartisan and designed to inform, not persuade. However, endorsing candidates or lobbying for specific bills crosses into political territory. Organizations must document their activities carefully, ensuring compliance through clear mission statements, activity logs, and financial records that separate charitable expenditures from political ones.

A comparative analysis of regulatory frameworks across jurisdictions reveals varying thresholds for political engagement. In the U.S., 501(c)(3) organizations face strict limits on lobbying, while 501(c)(4) social welfare groups enjoy more flexibility but forfeit certain tax benefits. In contrast, the UK’s Charity Commission allows charities to engage in political activity if it directly supports their charitable objectives. This disparity underscores the importance of understanding local laws, as misalignment can result in penalties, loss of tax-exempt status, or reputational damage.

Practical tips for navigating these distinctions include adopting a "primary purpose" test, where organizations prioritize charitable goals over political advocacy. For instance, a health-focused nonprofit can advocate for healthcare policy changes but must ensure such efforts complement its core mission of providing medical services. Additionally, establishing separate entities for charitable and political activities can provide clarity, though this approach requires careful legal structuring to avoid attribution issues. Regular audits and legal consultations are essential to maintain compliance in this complex landscape.

Ultimately, the legal distinction between charitable and political activities hinges on intent, proportion, and documentation. Organizations must balance their desire to effect systemic change through advocacy with the need to uphold their charitable mission. By adhering to regulatory guidelines and adopting proactive compliance measures, nonprofits can navigate this divide effectively, ensuring their work remains both impactful and legally sound.

Am I Made for Politics? Exploring My Potential in Public Service

You may want to see also

Explore related products

![]()

Lobbying Limits: Rules governing charitable organizations' engagement in political advocacy or lobbying efforts

Charitable organizations often navigate a delicate balance when engaging in political advocacy or lobbying, as their tax-exempt status under Section 501(c)(3) of the U.S. Internal Revenue Code imposes strict limits on such activities. While these organizations can advocate for policy changes that align with their charitable missions, they must avoid partisan political activity and ensure lobbying efforts do not become a substantial part of their operations. The IRS defines "substantial" as more than a negligible amount, though it lacks a precise percentage, leaving organizations to tread carefully. For instance, a health-focused charity can lobby for healthcare policy reforms but cannot endorse candidates or spend the majority of its resources on political campaigns.

To comply with these rules, charitable organizations must adopt clear strategies. First, they should track lobbying expenditures meticulously, ensuring they remain within the "insubstantiality" threshold. The IRS offers two safe harbor tests: the 501(h) election, which allows organizations to spend a specific percentage of their budget on lobbying (based on their annual expenditures), or the "no substantial part" test, which is less defined but riskier. For example, a small nonprofit with $500,000 in annual expenditures can spend up to $25,000 on lobbying if it elects 501(h) status. Second, organizations should distinguish between direct lobbying (e.g., contacting legislators) and grassroots lobbying (e.g., urging the public to contact legislators), as both count toward the lobbying limit but require different reporting.

Despite these guidelines, ambiguity persists, creating challenges for charitable organizations. The lack of a clear percentage for "substantial" lobbying leaves room for interpretation, and the consequences of exceeding limits—including loss of tax-exempt status—are severe. For instance, a charity advocating for environmental protection might inadvertently cross the line by organizing large-scale public campaigns urging legislative action. To mitigate risk, organizations should consult legal counsel, document all advocacy activities, and consider electing 501(h) status for clearer boundaries.

Comparatively, non-charitable organizations under Section 501(c)(4) face fewer restrictions on political activity but cannot offer tax deductions for donations. This distinction highlights the trade-off charitable organizations make for their tax-exempt status: greater public trust and funding opportunities in exchange for limited political engagement. For example, while a 501(c)(3) charity can advocate for education reform, a 501(c)(4) organization can explicitly support candidates who champion similar policies.

In practice, charitable organizations can maximize their advocacy impact without violating rules by focusing on non-partisan issues, leveraging grassroots education campaigns, and collaborating with non-charitable allies for more explicit political work. For instance, a charity promoting affordable housing might educate the public about policy gaps while partnering with a 501(c)(4) group to endorse specific legislation. By understanding and respecting lobbying limits, these organizations can remain compliant while advancing their missions effectively.

Music's Political Pulse: Exploring the Hidden Agendas in Every Note

You may want to see also

Explore related products

![]()

Campaign Involvement: Restrictions on charities supporting or opposing political candidates or parties

Charities often face a delicate balance when navigating the realm of political campaigns. While they may advocate for issues aligned with their mission, directly supporting or opposing specific candidates or parties can jeopardize their tax-exempt status. The IRS strictly prohibits 501(c)(3) organizations, the most common type of charity, from engaging in partisan political activity. This includes endorsing candidates, making contributions to their campaigns, or distributing materials that favor one party over another. Violating these rules can result in severe penalties, including loss of tax exemption and hefty fines.

Example: Imagine a charity dedicated to environmental conservation. They can lobby for policies promoting renewable energy and educate the public about climate change. However, they cannot publicly endorse a candidate who supports these policies or use charitable funds to purchase ads attacking a candidate with opposing views.

Understanding the nuances of permissible versus prohibited activities is crucial for charities. They can engage in non-partisan voter education, such as hosting candidate forums where all qualified candidates are invited, or registering voters without influencing their choices. Additionally, charities can participate in ballot measure campaigns, as long as they do not align with a specific party’s platform. For instance, a charity focused on education reform can advocate for a ballot initiative to increase school funding, provided their efforts remain issue-specific and non-partisan.

Despite these restrictions, charities can still amplify their impact by collaborating with non-charitable arms of their organization, such as 501(c)(4) social welfare groups or political action committees (PACs). These entities are allowed to engage in political campaigning but are subject to different tax rules and disclosure requirements. For example, a charity’s affiliated 501(c)(4) can endorse candidates, run ads, and mobilize voters, while the charity itself focuses on issue advocacy and community programs.

In practice, charities must establish clear internal policies and safeguards to ensure compliance. This includes training staff and volunteers on permissible activities, maintaining separate bank accounts for charitable and political work, and documenting all expenditures. Charities should also consult legal counsel when in doubt, as the line between issue advocacy and political campaigning can be thin. By adhering to these guidelines, charities can remain effective advocates for their causes without risking their charitable status.

Ultimately, while charities cannot directly support or oppose political candidates or parties, they have ample opportunities to shape public discourse and influence policy. By focusing on issue-based advocacy, non-partisan education, and strategic partnerships, charities can navigate the political landscape responsibly and continue to drive positive change in their communities.

How Political Polarization Tears Apart Well-Intentioned Individuals and Communities

You may want to see also

Explore related products

![]()

Public Perception: How political ties impact public trust and donor confidence in charitable organizations

Political ties can act as a double-edged sword for charitable organizations, significantly influencing public trust and donor confidence. On one hand, aligning with political entities can amplify an organization's reach and resources, leveraging political networks to advance its mission. For instance, a charity focused on climate change might partner with a political party advocating for green policies, gaining visibility and support. However, this alignment often comes at a cost. Donors and the public may perceive such partnerships as compromising the organization's neutrality, questioning whether the charity’s actions are driven by genuine altruism or political agendas. This skepticism can erode trust, particularly among those who hold opposing political views, leading to reduced donations and engagement.

Consider the case of a well-known humanitarian organization that accepted funding from a politically divisive corporation. Despite the funds being earmarked for disaster relief, public backlash was swift. Social media campaigns highlighted the corporation’s controversial practices, prompting donors to withdraw support. This example underscores the delicate balance charities must strike when engaging with political or politically affiliated entities. Transparency becomes critical in such scenarios. Organizations must clearly communicate the purpose and boundaries of these partnerships to mitigate mistrust. For instance, publishing detailed reports on how funds are used and ensuring decision-making remains independent can reassure donors of the charity’s integrity.

The impact of political ties varies across demographics, further complicating public perception. Younger donors, aged 18–35, tend to be more skeptical of politically aligned charities, often viewing them as extensions of partisan interests. In contrast, older donors, aged 55 and above, may be more forgiving, prioritizing the charity’s outcomes over its affiliations. Charities must tailor their messaging to address these generational differences. For younger audiences, emphasizing grassroots initiatives and community impact can rebuild trust. For older donors, highlighting long-term achievements and accountability measures may be more effective. Practical steps include conducting donor surveys to gauge sentiment and adjusting communication strategies accordingly.

To navigate this landscape, charitable organizations should adopt a proactive approach. First, establish a clear policy on political partnerships, outlining criteria for collaboration and safeguards against undue influence. Second, engage in open dialogue with stakeholders, hosting town halls or webinars to address concerns. Third, diversify funding sources to reduce reliance on politically tied donors, ensuring financial stability regardless of public sentiment shifts. Caution is advised when accepting large donations from politically affiliated entities, as these can trigger immediate public scrutiny. By prioritizing transparency and adaptability, charities can maintain trust and donor confidence even in politically charged environments.

Corporate Law Firms and Their Political Influence: A Deep Dive

You may want to see also

Explore related products

$11.99 $14.95

![The Art of Advocacy: Briefs, Motions, and Writing Strategies of America's Best Lawyers [Connected eBook] (Aspen Coursebook)](https://m.media-amazon.com/images/I/71nFTPUXCiL._AC_UL320_.jpg)

![]()

Funding Sources: Transparency requirements for charitable organizations receiving political or government funding

Charitable organizations often navigate a complex web of funding sources, and those receiving political or government funding face heightened scrutiny. Transparency in this context is not just a moral imperative but a legal requirement in many jurisdictions. For instance, in the United States, organizations with 501(c)(3) status must disclose significant contributions on their IRS Form 990, though the names of individual donors are typically shielded. In contrast, 501(c)(4) organizations, which can engage in political activities, are not required to disclose donors, creating a transparency gap that critics argue undermines accountability.

To ensure compliance and maintain public trust, charitable organizations must adopt robust transparency practices. First, establish a clear funding disclosure policy that outlines which sources will be publicly reported and at what thresholds. For example, any government grant exceeding $50,000 or political donation above $10,000 could trigger a disclosure. Second, leverage digital platforms to publish real-time updates on funding sources, ensuring the information is easily accessible to stakeholders. Tools like interactive dashboards or annual reports with detailed breakdowns can enhance clarity. Third, proactively engage with auditors and regulatory bodies to verify compliance and address potential red flags before they escalate.

A comparative analysis reveals that countries with stricter transparency laws tend to foster greater public trust in charitable organizations. For instance, the UK’s Charity Commission mandates that all charities disclose government grants and political donations in their annual returns, regardless of size. This contrasts with Canada, where disclosure requirements are less stringent, leading to occasional controversies over opaque funding. Organizations operating internationally must therefore navigate these varying standards, adopting best practices that exceed the minimum legal requirements to build global credibility.

Despite the benefits of transparency, challenges persist. One major hurdle is the administrative burden of tracking and reporting diverse funding streams, particularly for smaller organizations with limited resources. To mitigate this, charities can invest in donor management software that automates tracking and reporting. Another challenge is balancing transparency with donor privacy, especially when political or government funding is involved. Here, organizations can adopt a tiered disclosure approach, providing detailed information to regulatory bodies while offering aggregated data to the public.

Ultimately, transparency in funding sources is a cornerstone of ethical charitable practice, particularly for organizations receiving political or government support. By implementing clear policies, leveraging technology, and learning from global standards, charities can navigate this complex landscape effectively. The takeaway is clear: transparency is not just about compliance—it’s about building trust, ensuring sustainability, and upholding the integrity of the charitable sector in an increasingly scrutinized environment.

Inquisitors: Religious Zealots or Political Tools in Historical Context?

You may want to see also

Frequently asked questions

Generally, political organizations are not considered charitable under U.S. tax law. Section 501(c)(3) organizations, which are tax-exempt charities, are prohibited from engaging in substantial lobbying or political campaign activities. Political organizations typically fall under Section 527 of the Internal Revenue Code, which covers groups organized to influence elections or nominate candidates.

Yes, but with strict limitations. Charitable organizations under Section 501(c)(3) can engage in some lobbying activities if they are not a substantial part of their overall activities. However, they are strictly prohibited from supporting or opposing political candidates or parties. Violating these rules can result in penalties or loss of tax-exempt status.

No, donations to political organizations are generally not tax-deductible. Contributions to Section 501(c)(3) charities are tax-deductible for the donor, but donations to political organizations, such as those under Section 527, are not eligible for tax deductions. However, some political donations may be deductible as business expenses under specific circumstances.