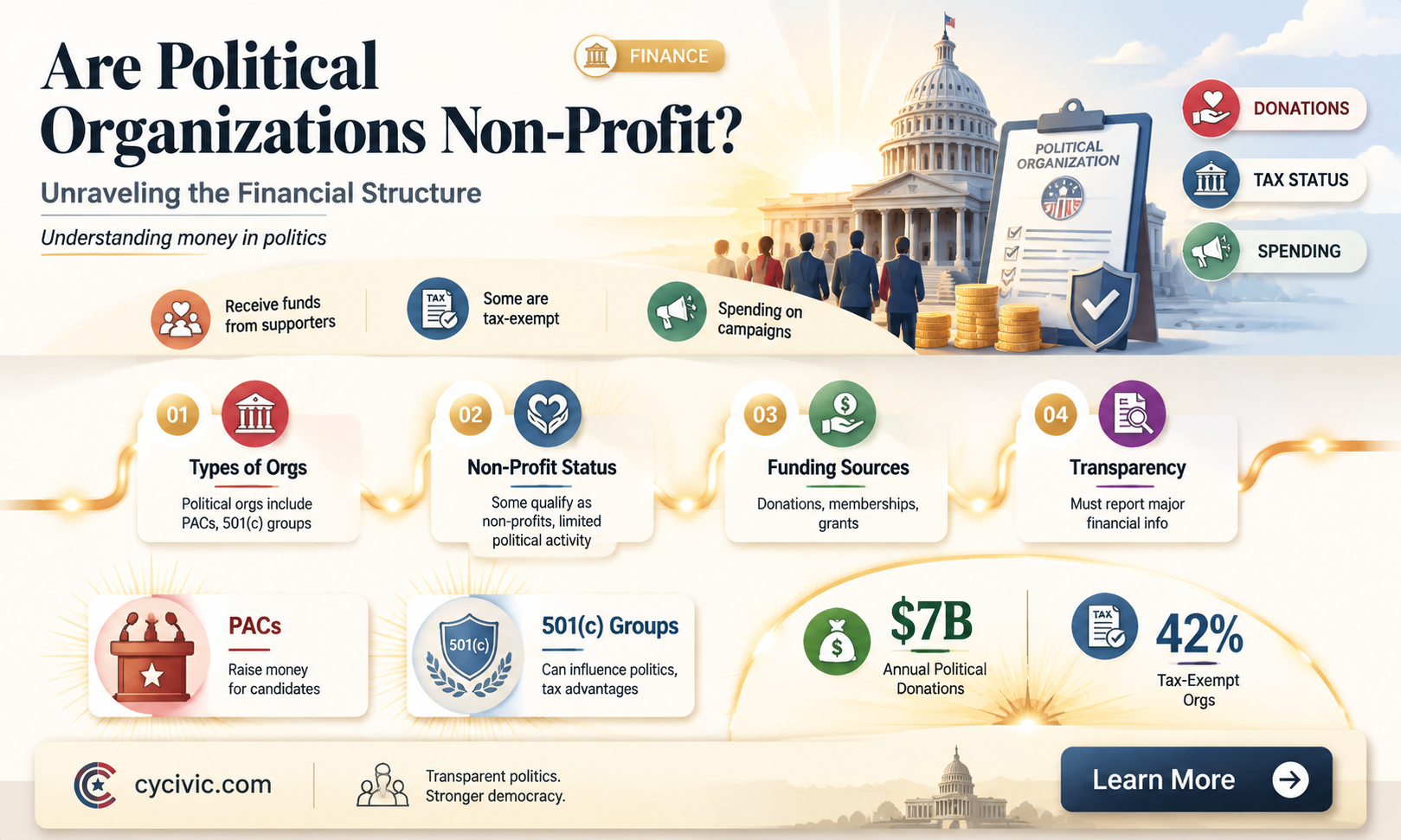

Political organizations often operate as non-profit entities, primarily because their core mission is to advocate for specific causes, influence public policy, or support political candidates rather than generate profit. These organizations typically rely on donations, grants, and membership fees to fund their activities, which are then used to advance their political goals. While some political groups may engage in fundraising or merchandise sales, any revenue generated is reinvested into their operations rather than distributed as profit. This non-profit status allows them to maintain tax-exempt benefits and focus on their advocacy efforts, though it also subjects them to strict regulations regarding lobbying, campaign finance, and transparency. As a result, the non-profit structure is a common and strategic choice for political organizations seeking to maximize their impact while adhering to legal and ethical standards.

Explore related products

What You'll Learn

- Legal Definitions: Non-profit vs. political organization classifications under IRS and state laws

- Funding Sources: How political non-profits raise and allocate funds without profit motives

- Tax Exemptions: Criteria for tax-exempt status and compliance for political entities

- Advocacy Limits: Rules governing political activities for non-profits to maintain non-profit status

- Transparency Requirements: Reporting and disclosure mandates for political non-profit organizations

![]()

Legal Definitions: Non-profit vs. political organization classifications under IRS and state laws

Under U.S. law, the classification of organizations as non-profit or political hinges on distinct criteria outlined by the Internal Revenue Service (IRS) and state statutes. Non-profits, typically structured under Section 501(c) of the Internal Revenue Code, are primarily formed for charitable, educational, religious, or scientific purposes. These entities must operate exclusively for their exempt purposes, with any earnings dedicated to their mission rather than distributed to private individuals. In contrast, political organizations, often classified under Section 527, are formed to influence the selection, nomination, election, or appointment of individuals to federal, state, or local public office. While both types may engage in advocacy, the IRS scrutinizes their activities to ensure compliance with their respective classifications.

A critical distinction lies in the tax treatment and reporting requirements. Non-profits under 501(c)(3) enjoy tax-exempt status and can receive tax-deductible donations, but they face strict limitations on political campaign intervention. Engaging in substantial lobbying or endorsing candidates can jeopardize their status. Political organizations, however, are taxed on their political expenditures but are not subject to the same restrictions on political activities. They must file periodic reports with the IRS detailing their income, expenditures, and political activities, ensuring transparency but allowing direct political engagement.

State laws further complicate this landscape by imposing additional registration, reporting, and operational requirements. For instance, some states require non-profits to register as charitable organizations and submit annual financial reports, while political organizations may need to register as political action committees (PACs) and disclose donor information. These state-level regulations often align with federal guidelines but can introduce unique compliance challenges. Organizations operating across multiple states must navigate a patchwork of laws, ensuring adherence to both federal and state mandates.

Practical considerations arise when an organization’s activities straddle the line between non-profit and political purposes. For example, a 501(c)(4) social welfare organization can engage in political activities as long as they do not constitute its primary purpose. However, the IRS’s “facts and circumstances” test evaluates the organization’s activities, expenditures, and messaging to determine compliance. Misclassification or overstepping boundaries can result in penalties, loss of tax-exempt status, or legal action. Organizations must carefully document their activities and consult legal counsel to ensure alignment with both IRS and state regulations.

In conclusion, while non-profits and political organizations share some operational similarities, their legal classifications under IRS and state laws are distinct and carry significant implications. Understanding these differences is essential for compliance, strategic planning, and maintaining public trust. Organizations must carefully assess their mission, activities, and goals to determine the appropriate classification and navigate the complex regulatory environment effectively.

Is Non-Binary Identity Political? Exploring Gender Beyond the Binary

You may want to see also

Explore related products

![]()

Funding Sources: How political non-profits raise and allocate funds without profit motives

Political non-profits, often classified as 501(c)(4) organizations in the U.S., operate without profit motives but still require substantial funding to advance their missions. Unlike traditional businesses, their revenue streams are tightly regulated and must align with their tax-exempt status. These organizations primarily rely on donations from individuals, corporations, and other entities, though the rules governing these contributions differ significantly from those for charitable non-profits. For instance, while 501(c)(3) charities must disclose large donors to the IRS but not the public, 501(c)(4)s can keep all donor identities private, a feature that has sparked both strategic use and public scrutiny.

To raise funds effectively, political non-profits often employ targeted campaigns that resonate with specific ideological or policy-driven audiences. Membership fees, crowdfunding, and merchandise sales are common tactics, but the bulk of their revenue typically comes from major donors and foundations. For example, organizations like the Sierra Club or the National Rifle Association leverage their large membership bases to generate steady income, while also courting wealthy benefactors who share their goals. The key is framing contributions as investments in a shared cause rather than transactions, which helps maintain donor engagement without promising financial returns.

Allocating funds in political non-profits requires a delicate balance between advocacy, operational costs, and compliance with legal restrictions. While these organizations can engage in lobbying and political campaigns, such activities cannot be their primary function. Funds are often directed toward research, public education, grassroots mobilization, and legal battles. For instance, a non-profit focused on climate policy might allocate 40% of its budget to advocacy campaigns, 30% to research and reports, and the remainder to administrative costs. Transparency in spending is critical, as misuse of funds can lead to loss of tax-exempt status or public backlash.

One challenge political non-profits face is navigating the "dark money" debate, where undisclosed donations raise questions about influence and accountability. To counter this, some organizations voluntarily disclose their funding sources or adopt stricter internal policies. For example, the League of Conservation Voters publishes an annual report detailing its major donors and expenditures, even though it is not legally required to do so. Such practices not only build trust with supporters but also differentiate these organizations from less transparent counterparts in the political sphere.

In conclusion, political non-profits raise and allocate funds through a combination of strategic outreach, diverse revenue streams, and careful adherence to legal boundaries. Their success hinges on aligning donor interests with organizational goals while maintaining public trust. By focusing on mission-driven initiatives and transparent operations, these entities demonstrate that impact, not profit, is the ultimate measure of their effectiveness. For those looking to support or start such an organization, understanding these funding dynamics is essential to ensuring long-term sustainability and influence.

Quakers and Politics: Understanding Their Stance on Political Engagement

You may want to see also

Explore related products

$25.1 $29.95

![]()

Tax Exemptions: Criteria for tax-exempt status and compliance for political entities

Political organizations often seek tax-exempt status to operate efficiently while fulfilling their missions. In the United States, the Internal Revenue Service (IRS) grants tax exemption under Section 501(c) of the Internal Revenue Code, with specific provisions for different types of organizations. For political entities, the most relevant categories are 501(c)(3) and 501(c)(4). Understanding the criteria for these designations is crucial, as they dictate not only tax obligations but also permissible activities and compliance requirements.

To qualify for 501(c)(3) status, an organization must be organized and operated exclusively for charitable, educational, religious, or scientific purposes. Political entities, however, face a significant limitation: they cannot engage in partisan political activities. This means no endorsing candidates, contributing to campaigns, or participating in election-related advocacy. For example, a non-profit focused on voter education can qualify under 501(c)(3) if it provides unbiased information without favoring any candidate or party. Compliance requires meticulous record-keeping and ensuring all activities align with the organization’s stated mission. Violations can result in penalties, loss of tax-exempt status, or even legal action.

In contrast, 501(c)(4) organizations, known as social welfare organizations, have more flexibility in political engagement. These entities can lobby for legislation and participate in political campaigns, provided that such activities do not become their primary focus. The IRS requires that promoting social welfare remain the organization’s primary purpose. For instance, a grassroots advocacy group pushing for environmental policies can qualify under 501(c)(4) if it spends the majority of its resources on community education and outreach rather than political campaigns. Compliance here involves tracking expenditures and ensuring political activities are secondary to social welfare efforts.

Achieving and maintaining tax-exempt status requires careful planning and adherence to IRS guidelines. Organizations must file Form 1023 or 1024 to apply for exemption, providing detailed information about their structure, activities, and finances. Annual reporting via Form 990 is mandatory, with additional disclosures for lobbying or political expenditures. Practical tips include establishing clear bylaws, maintaining transparent financial records, and consulting legal or tax professionals to navigate complex regulations. Regular audits and internal reviews can also help identify compliance gaps before they escalate.

The choice between 501(c)(3) and 501(c)(4) hinges on an organization’s goals and activities. While 501(c)(3) offers broader public support and donation incentives, its restrictions on political activity may limit advocacy efforts. Conversely, 501(c)(4) allows for more direct political engagement but with stricter scrutiny and fewer donor benefits. For example, a non-profit focused on systemic change might opt for 501(c)(4) to lobby for policy reforms, while a charity providing direct services might prefer 501(c)(3) to maximize donor contributions. Ultimately, aligning tax status with organizational objectives ensures sustainability and compliance in the long term.

Mastering Political Growth: Strategies for Success in Public Service

You may want to see also

Explore related products

![]()

Advocacy Limits: Rules governing political activities for non-profits to maintain non-profit status

Non-profits must navigate strict rules to maintain their tax-exempt status while engaging in advocacy. The IRS prohibits 501(c)(3) organizations from participating in any amount of political campaign activity, including endorsing or opposing candidates. However, they can engage in limited lobbying if it aligns with their mission and remains under a certain threshold. For instance, the "substantial part test" allows lobbying as long as it doesn’t constitute a substantial portion of the organization’s activities. Exceeding this limit risks losing tax-exempt status, making compliance critical.

To stay within bounds, non-profits should distinguish between lobbying and non-partisan advocacy. Lobbying involves attempting to influence specific legislation, while advocacy can include educating the public or policymakers on broader issues. For example, a non-profit focused on environmental conservation can lobby for a specific bill reducing carbon emissions but must avoid endorsing a candidate who supports it. Tools like the "501(h) election" provide clearer lobbying limits based on organizational expenditures, offering a safer framework for those planning extensive advocacy efforts.

Practical steps include tracking all advocacy-related expenses and ensuring they fall within IRS guidelines. Non-profits should also train staff and volunteers to recognize the difference between permissible advocacy and prohibited political activity. For instance, hosting a voter education forum is acceptable, but distributing materials that favor one candidate is not. Regularly consulting legal counsel or using IRS resources can help organizations avoid unintentional violations, especially during election seasons when scrutiny intensifies.

Despite these restrictions, non-profits can still drive meaningful change through strategic advocacy. By focusing on issues rather than individuals, they can amplify their mission without jeopardizing their status. For example, a health-focused non-profit can advocate for increased funding for disease research without endorsing a specific politician’s healthcare plan. Balancing passion for change with adherence to rules ensures long-term sustainability and impact.

In summary, while non-profits face strict limits on political activities, understanding and adhering to these rules allows them to advocate effectively. By differentiating between lobbying and campaigning, leveraging tools like the 501(h) election, and maintaining meticulous records, organizations can navigate advocacy limits confidently. The key lies in staying mission-focused, issue-driven, and compliant, ensuring their work remains both impactful and protected.

Navigating Corporate Politics: Strategies for Success and Career Advancement

You may want to see also

Explore related products

$11.99 $14.95

![The Art of Advocacy: Briefs, Motions, and Writing Strategies of America's Best Lawyers [Connected eBook] (Aspen Coursebook)](https://m.media-amazon.com/images/I/71nFTPUXCiL._AC_UL320_.jpg)

![]()

Transparency Requirements: Reporting and disclosure mandates for political non-profit organizations

Political non-profit organizations, often classified under Section 501(c)(3) or 501(c)(4) of the U.S. Internal Revenue Code, operate with distinct transparency requirements. These mandates are designed to balance their tax-exempt status with public accountability, particularly when engaging in political activities. For instance, 501(c)(4) organizations, known as social welfare groups, can participate in political campaigns but must disclose their donors to the IRS, though not publicly. In contrast, 501(c)(3) organizations face stricter limits on political involvement and must avoid endorsing candidates altogether. This distinction highlights the varying degrees of transparency required based on an organization’s tax classification and political engagement.

Reporting mandates for political non-profits are not one-size-fits-all. Organizations must file Form 990 annually with the IRS, detailing finances, activities, and governance practices. For those involved in lobbying or political campaigns, additional disclosures are required. For example, the Federal Election Commission (FEC) mandates that groups spending over $250 on political ads disclose their expenditures and donors if the ads explicitly support or oppose a candidate. However, "dark money" groups, often structured as 501(c)(4)s, exploit loopholes by avoiding direct candidate endorsements, thus sidestepping donor disclosure requirements. This underscores the complexity and occasional ambiguity in current transparency rules.

Internationally, transparency requirements for political non-profits vary widely. In Canada, organizations must disclose political activities exceeding CAD 500 annually, while the UK requires charities to report any political spending over £20,000. These examples illustrate how different jurisdictions prioritize transparency differently, often reflecting cultural attitudes toward the role of non-profits in politics. Comparative analysis reveals that while the U.S. system emphasizes financial reporting, other countries focus more on activity-based disclosures, offering alternative models for balancing accountability and operational freedom.

Practical compliance with transparency requirements demands proactive measures. Non-profits should maintain meticulous records of expenditures, donations, and political activities, ensuring alignment with IRS and FEC guidelines. Utilizing specialized software to track and categorize expenses can streamline reporting processes. Additionally, organizations should conduct regular internal audits to identify potential compliance gaps. For those navigating the complexities of political engagement, consulting legal experts in non-profit law can provide tailored guidance. Transparency is not merely a legal obligation but a cornerstone of public trust, making it essential for organizations to exceed minimum requirements where possible.

Ultimately, transparency requirements for political non-profits serve as both a safeguard and a challenge. While they ensure accountability, the varying mandates across classifications and jurisdictions create a fragmented landscape. Stakeholders, including donors, policymakers, and the public, must advocate for clearer, more uniform standards that enhance accountability without stifling legitimate political participation. As political non-profits continue to shape public discourse, robust transparency mechanisms will remain critical to maintaining their credibility and democratic integrity.

Is Burping Polite in China? Cultural Etiquette Explained

You may want to see also

Frequently asked questions

Political organizations can be structured as non-profits, but they are typically classified under specific tax codes, such as 501(c)(4) in the U.S., which allows them to engage in political activities while maintaining non-profit status.

Yes, political non-profits can accept donations, but contributions are generally not tax-deductible for donors, and the organizations must comply with campaign finance laws and disclosure requirements.

Disclosure requirements vary by jurisdiction. In the U.S., 501(c)(4) organizations are not required to disclose donors publicly, but they must report certain financial information to the IRS.

Yes, political non-profits, particularly those under 501(c)(4) status, can endorse candidates and engage in political campaigns, but their primary activity must still align with their non-profit mission.