Simplified Employee Pension (SEP) plans are retirement plans established by employers for the benefit of their employees and themselves. They are designed to encourage businesses that would otherwise not set up employer-sponsored plans to offer retirement benefits to their employees. SEPs are advantageous because they are easy to set up, have low administrative costs, and allow employers to determine how much to contribute each year. They also have higher annual contribution limits than traditional IRAs. However, it's important to note that only employers can contribute to SEP plans, and these contributions vest immediately. To establish a SEP, employers must follow certain steps, including choosing a financial institution to serve as a trustee and executing a written agreement to provide benefits to eligible employees.

Explore related products

What You'll Learn

- Only employers can contribute to SEP plans

- Contributions are made to an employee's Individual Retirement Account or Annuity (SEP-IRA)

- Employers can contribute up to 25% of each employee's pay

- Employees must meet eligibility requirements, including a minimum compensation threshold

- Employers receive tax benefits for their contributions

![]()

Only employers can contribute to SEP plans

A Simplified Employee Pension (SEP) plan is a retirement savings plan that employers can set up for their employees. It is a tax-deferred benefit that allows employers to contribute to their employees' retirement savings. Self-employed individuals can also set up a SEP plan for themselves.

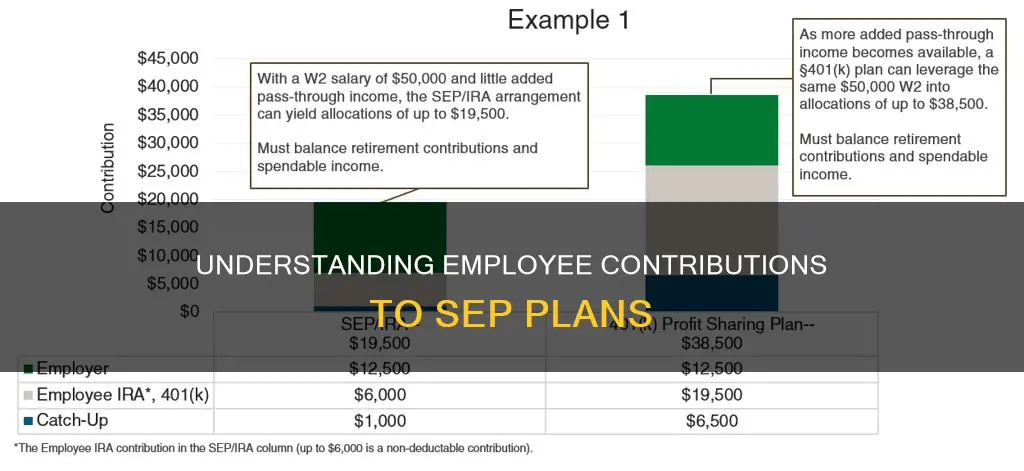

SEP plans are advantageous because they are easy to set up, have low administrative costs, and allow employers to determine how much to contribute each year. They also have higher annual contribution limits than traditional Individual Retirement Accounts (IRAs). For example, for the 2023 tax year, the contribution limit for a SEP plan is up to 25% of the employee's compensation or $66,000, whichever is less. This is significantly higher than the $6,500 limit imposed on standard IRAs for that year.

While employers have the flexibility to decide the contribution amount each year, they are required to contribute uniformly for all employees. Additionally, employers must provide each participant with a notice of the contributions made to their SEP-IRA each year, as well as the value of their account at the end of the year.

It is important to note that only employers can contribute to SEP plans. Employees are not allowed to contribute directly to these plans, although they do have control over the investment decisions within the limits set by the plan's trustee.

Democracy's Danger: The Founders' Constitution Conundrum

You may want to see also

Explore related products

![]()

Contributions are made to an employee's Individual Retirement Account or Annuity (SEP-IRA)

A Simplified Employee Pension (SEP) plan is a retirement savings plan that allows employers to contribute to traditional IRAs (SEP-IRAs) set up for their employees. SEPs are advantageous because they are easy to set up, have low administrative costs, and allow employers to determine how much to contribute each year. They are also flexible, as employers are not locked into an annual contribution and can change the amount they contribute from year to year.

SEPs are an attractive option for many business owners, especially small businesses and self-employed individuals, as they do not have the start-up and operating costs of a conventional retirement plan. They also allow for higher annual contribution limits than traditional IRAs, with the ability to contribute up to 25% of each employee's pay or a maximum of $66,000 for the 2023 tax year, $69,000 for 2024, and $70,000 for 2025.

To establish a SEP, employers must first choose a financial institution, such as a bank or mutual fund company, to serve as the trustee of the SEP-IRAs. The trustee holds each employee's retirement plan assets and manages the investment decisions. Employers then need to execute a written agreement, which includes information such as the name of the employer, employee participation requirements, and a definite allocation formula. This agreement must be signed by a responsible official and provided to all eligible employees.

It is important to note that only employers can contribute to a SEP plan, and these contributions are tax-deductible. Employees are not allowed to contribute their salary deferrals. Additionally, all eligible employees must participate in the plan, including part-time and seasonal employees. Employers must provide each participant with a notice of the contributions made and the value of their SEP-IRA at the end of each year.

In-text Referencing the South African Constitution: A Guide

You may want to see also

Explore related products

![]()

Employers can contribute up to 25% of each employee's pay

A Simplified Employee Pension (SEP) plan allows employers to contribute to traditional IRAs (SEP-IRAs) set up for employees. A SEP is a retirement savings plan established by employers for the benefit of their employees and themselves. It can also be established by self-employed individuals.

The decision about whether and how much to contribute each year can vary, and employers are not locked into an annual contribution. This flexibility is advantageous for businesses, especially in cyclical industries with good times and downtimes. Employers receive a tax deduction for their contributions, and they are not responsible for making investment decisions. Instead, the IRA trustee determines eligible investments, and individual employees make specific investment decisions within the limits set by the trustee.

To establish a SEP, employers must first choose a financial institution to serve as the trustee of the SEP-IRAs. Then, they must execute a written agreement to provide benefits to all eligible employees, give employees certain information about the agreement, and set up an IRA account for each employee. The written agreement must include the name of the employer, the requirements for employee participation, a signature from a responsible official, and a definite allocation formula.

It is important to note that employees cannot contribute to SEP-IRAs, and the contribution rate must be uniform for all employees.

Compromise: The Constitution's Cornerstone

You may want to see also

Explore related products

![]()

Employees must meet eligibility requirements, including a minimum compensation threshold

A Simplified Employee Pension (SEP) plan is a retirement savings plan established by employers for their employees and themselves. It is a tax-deferred benefit that allows employers to contribute to traditional IRAs (SEP-IRAs) set up for employees.

To be eligible for a SEP contribution, employees must meet certain requirements. These include working for the employer in at least three of the previous five years and earning a minimum compensation of at least $600 in 2019 and 2020, $650 in 2021 and 2022, and $750 in 2023. This minimum compensation threshold is expected to remain the same for 2024 and 2025.

The eligibility criteria also include the type of employee, such as part-time, seasonal, leased, or non-resident alien employees. Employers can customize eligibility requirements within limits and change them annually. For example, they can choose to cover employees under a collective bargaining agreement or include non-resident alien employees who did not earn income from the company.

It is important to note that employers are not allowed to be more restrictive in their qualification requirements than IRS rules. The IRS provides a model SEP plan document, Form 5305-SEP, which outlines the requirements for employee participation and the allocation formula for contributions. This form must be provided to each employee, along with certain information about the SEP-IRAs.

Whiskey Rebellion: Constitutional or Not?

You may want to see also

![]()

Employers receive tax benefits for their contributions

A Simplified Employee Pension (SEP) plan is a tax-deferred benefit that helps self-employed individuals and small-business owners save for retirement. It is a retirement plan that allows employers to contribute to their employees' retirement savings. SEPs are a great way for employers to receive tax benefits for their contributions.

SEPs are funded only by employer contributions, and employees cannot contribute to them. Employers can decide whether and how much to contribute to their employees' SEP-IRAs each year, and contributions are limited to 25% of each employee's pay. This flexibility allows employers to make larger contributions during good years and reduce the amount during downtimes.

Contributions to a SEP are tax-deductible, and employers do not pay taxes on investment earnings. Additionally, SEP contributions are not subject to federal income tax withholding, social security, Medicare, or federal unemployment (FUTA) taxes. This means that employers can deduct their contributions, and employees can exclude these contributions from their gross income.

To maintain the tax benefits of a SEP, employers must ensure that the plan satisfies the Internal Revenue Code requirements. If errors occur, employers can use IRS correction programs to correct them and retain the tax benefits. These programs encourage early error correction and help protect participants' interests.

In summary, Simplified Employee Pension (SEP) plans offer tax benefits to employers who contribute to their employees' retirement savings. Employers can deduct contributions, avoid certain taxes, and retain benefits by ensuring the plan complies with regulations.

Exploring Agency Affiliations: Cabinet Conundrum

You may want to see also

Frequently asked questions

Only employers can contribute to a SEP plan for their employees. Self-employed individuals can also establish a SEP.

To qualify for a SEP contribution, an employee must have worked for the employer in at least three of the previous five years and have received a minimum of $650 in compensation from the employer during the current year.

The contribution limit for a SEP is up to 25% of each employee's pay or a maximum of $66,000 for the 2023 tax year, $69,000 for 2024, and $70,000 for 2025.

To establish a SEP, employers must choose a financial institution to serve as a trustee of the SEP-IRAs, execute a written agreement to provide benefits to eligible employees, and set up an IRA account for each employee.