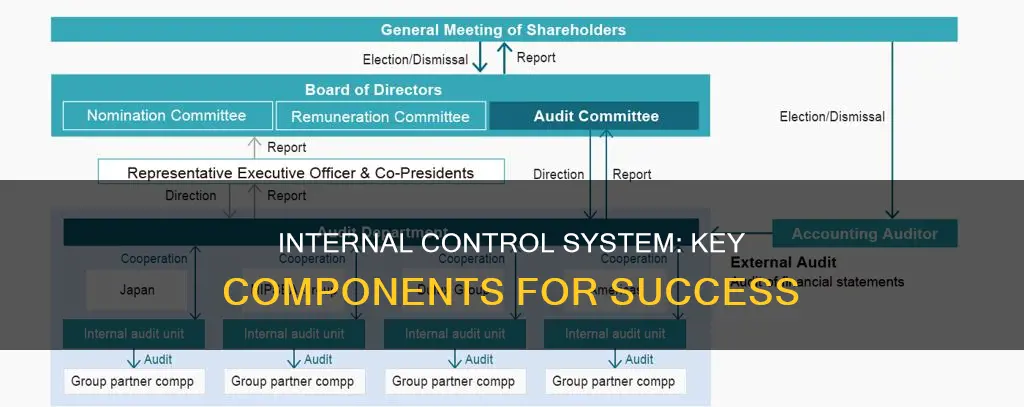

An effective system of internal control is essential for organisations to ensure integrity, compliance, and efficiency. Internal controls are mechanisms, rules, and procedures implemented to maintain the integrity of financial and accounting information, prevent fraud, and promote accountability. These controls can vary across organisations depending on their needs, risk environments, and stakeholder demands. While there are different types of controls, such as hard, soft, manual, and automated, they all play a role in identifying risks, detecting issues, and implementing corrective actions. Effective internal control systems consist of interconnected elements, including control environment, risk assessment, control activities, information and communication, and monitoring. These elements work together to safeguard assets, ensure compliance, and promote ethical behaviour.

| Characteristics | Values |

|---|---|

| Control Environment | The control environment sets the tone of an organization, influencing the control consciousness of its people. |

| Risk Assessment | Identification and analysis of relevant risks to achievement of objectives, forming a basis for determining how the risks should be managed. |

| Control Activities | The policies and procedures that help ensure management directives are carried out. |

| Information and Communication | Pertinent information must be identified, captured, and communicated in a form and timeframe that enables people to carry out their responsibilities. |

| Monitoring | A process that assesses the quality of the system's performance over time. |

| Compliance with Laws and Regulations | An organization's financial activities must adhere to all relevant laws, regulations, and standards. |

Explore related products

What You'll Learn

![]()

Control environment

An effective system of internal control is comprised of five interrelated components, one of which is the control environment. The control environment is the foundation of an organization's internal control system, setting the tone and influencing the control consciousness of its people. It includes the standards, processes, policies, and rules that enable an organization to implement and improve its internal controls.

Senior management plays a crucial role in establishing a strong control environment by inculcating a strong sense of ethics and high performance across the enterprise. They promote a culture of transparency, honesty, and accountability, ensuring that the organization's values and commitment to "toeing the line" are communicated effectively.

The control environment is not static; it involves ongoing risk assessment and management. Risks can be internal or external, and they must be identified, analysed, and managed to ensure they do not compromise the achievement of organizational objectives. This includes economic, industry, and regulatory changes, as well as evolving entity activities. Mechanisms must be in place to identify and react to these changing conditions.

Effective communication is essential to a robust control environment. Information must be identified, captured, and communicated effectively and honestly throughout the organization, enabling stakeholders to carry out their daily internal control activities. This includes disseminating information to relevant departments and individuals so they can understand their responsibilities and take appropriate action.

The control environment also includes the establishment of objectives, which are linked at different levels and are internally consistent. These objectives provide the basis for risk management and the implementation of necessary control activities, such as approvals, authorizations, verifications, reconciliations, and reviews of operating performance. Control activities ensure that management directives are carried out and that risks to the achievement of objectives are addressed.

Get Your Hands on a Constitution Copy

You may want to see also

Explore related products

$33.26 $45

$64.95 $100

![]()

Risk assessment

The first step in risk assessment is establishing objectives that are linked at different levels and internally consistent. These objectives provide a foundation for identifying and analysing relevant risks. For instance, operational objectives relate to the effectiveness and efficiency of operations, encompassing performance, financial goals, and safeguarding resources.

Once risks are identified, they must be evaluated to determine how they should be managed. This includes implementing control activities, which are the policies and procedures that ensure management directives are executed. Control activities can include approvals, authorisations, verifications, reconciliations, reviews of operating performance, security of assets, and segregation of duties.

To effectively manage risks, it is crucial to have a comprehensive understanding of the organisation's objectives and the potential risks associated with achieving those objectives. This understanding enables the identification and implementation of appropriate controls. For example, hard controls, such as organisational structure, policies, and procedures, provide formal and tangible risk mitigation. On the other hand, soft controls, like ethical climate integrity and trust, are informal and intangible but still contribute to risk reduction.

Additionally, monitoring activities are essential for assessing the quality of the internal control system's performance over time. This includes regular management and supervisory activities, as well as ongoing monitoring in the ordinary course of operations. The scope and frequency of separate evaluations are influenced by the assessment of risks and the effectiveness of existing monitoring procedures.

In conclusion, risk assessment in the context of internal controls involves a continuous process of identifying, analysing, and managing risks through the implementation of control activities, understanding objectives, employing various types of controls, and conducting ongoing monitoring activities. By effectively managing risks, organisations can increase their operational effectiveness and efficiency while safeguarding against potential threats.

William Paterson's Influence on the US Constitution

You may want to see also

Explore related products

![]()

Control activities

The policies and procedures implemented as control activities are designed to ensure the integrity of financial and accounting information, promote accountability, and prevent fraud. They help to ensure compliance with laws and regulations, including accurate and timely financial reporting and data collection. Control activities also promote operational efficiency by identifying problems and implementing corrections before external audits.

Effective communication is vital for successful control activities. Information must be identified, captured, and communicated effectively and efficiently throughout the organisation. This includes downward, horizontal, and upward communication to ensure everyone understands their role in the internal control system and how their work relates to others.

The Mexican Constitution's Impact on Multiparty Politics

You may want to see also

Explore related products

![]()

Information and communication

Clear communication of objectives is a precondition to risk assessment. Risks must be identified and analysed at all levels, and necessary actions must be taken to manage them. Risks can be internal or external, and they can change over time. Therefore, mechanisms are needed to identify and react to changing conditions. Once risks are identified, they must be evaluated. This evaluation forms the basis for determining how the risks should be managed.

Furthermore, information systems produce reports containing operational, financial, and compliance-related information that is essential for running and controlling the organisation. Solid information and consistent communication are important for setting the stage with a clear purpose and defined roles. They also facilitate the understanding and commitment of employees to the steps they need to take to do their jobs most effectively.

Citing the Constitution: Chicago Turabian Style

You may want to see also

Explore related products

$60.05 $129.99

![]()

Monitoring

The scope and frequency of separate evaluations depend on the nature of the risks and the efficacy of ongoing monitoring procedures. For instance, if an audit reveals a significant cybersecurity flaw, the findings should be communicated to the relevant departments, such as IT and legal, who can then take appropriate action. This two-way communication ensures that all stakeholders are aware of their responsibilities in addressing the identified issues and that internal controls are functioning as intended.

An important aspect of monitoring is the identification and analysis of risks, which is an ongoing process. Risks can be internal or external, and they must be evaluated and managed effectively. This includes understanding the objectives and the associated risks, which then informs the implementation of the correct control measures. For example, hard controls, such as organizational structure and policies, and soft controls, such as ethical climate and trust, must work together to reduce risks to an acceptable level.

Additionally, monitoring should also include an evaluation of the internal control structure, which is influenced by how management runs the organization. This structure is integrated with the management process and may vary depending on the size of the department or organization. It is essential to recognize that internal control is effected by people, and their judgment and actions can impact the effectiveness of the controls. Therefore, ongoing monitoring is necessary to identify any changes or deficiencies in the internal control system, which should be promptly addressed to ensure the system's overall effectiveness.

Free Inhabitants: A Constitutional Right or an Omission?

You may want to see also

Frequently asked questions

Internal controls are the mechanisms, rules, and procedures implemented by a company to ensure the integrity of financial and accounting information, promote accountability, and prevent fraud.

An effective internal control system consists of five interconnected key elements: control environment, risk assessment, control activities, information and communication, and monitoring.

Leadership plays a crucial role in an effective internal control system. They provide direction, demonstrate commitment to internal controls and risk management, and promote a culture of transparency, honesty, and accountability.

Internal controls help prevent fraud and irregularities by establishing policies and procedures that ensure management directives are carried out. Control activities include approvals, authorizations, verifications, reconciliations, and segregation of duties.

Internal control systems should be monitored regularly to assess their performance and effectiveness over time. This includes ongoing monitoring through management activities, supervisory actions, and personnel duties. Any deficiencies or serious matters should be reported immediately to top administration.