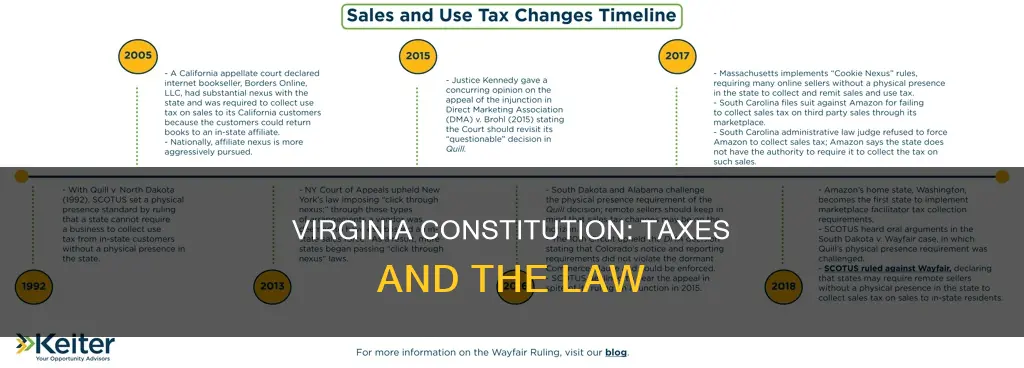

The Constitution of Virginia outlines taxation and finance in Article X, with provisions for property tax exemptions, revenue collection, and debt management. It grants the General Assembly the authority to impose franchise taxes on corporations and outlines rules for property tax exemptions for religious organisations and government-owned properties. The Constitution also mandates that all taxes, licenses, and revenues be collected by proper officers and deposited into the State treasury. Additionally, it addresses limitations on incurring expenses and outlines the process for authorising debt for capital projects. Virginia's tax system includes property, sales, and income taxes, with varying rates across the state.

| Characteristics | Values |

|---|---|

| Tax collection | All taxes, licenses, and other revenues of the Commonwealth shall be collected by its proper officers and paid into the State treasury. |

| Tax appropriation | No money shall be paid out of the State treasury except in pursuance of appropriations made by law. |

| Debt expenses | The Governor shall ensure that no expenses of the Commonwealth exceed total revenues on hand and anticipated during a period not to exceed two years and six months. |

| Franchise tax | The General Assembly may impose a franchise tax on corporations in lieu of taxes on other property. |

| Property tax exemption | Property owned by the Commonwealth or used for religious worship is exempt from taxation. |

| Educational funding | Counties, cities, or towns that accept distributions from the Fund must provide their portion of the cost of maintaining an educational program without using distributions from the Fund. |

| Tax rate limitation | No other or greater amount of tax or revenues shall be levied than is required for the necessary expenses of the government or to pay the indebtedness of the Commonwealth. |

| Debt authorization | The General Assembly may authorize the creation of debt for capital projects upon an affirmative vote of a majority of the members elected to each house. |

| Real estate tax | Based on the assessed value of a home and administered by local authorities, with average bills ranging from $378 to over $10,000. |

| Sales tax | The average combined state and local sales tax is 5.77%, with the state sales tax at 5.3% and some counties adding a local tax. |

| Income tax | Virginia uses a graduated income tax with four tax brackets, ranging from 2% to 5.75% for the highest earners. |

Explore related products

![]()

Property tax

Article X of the Virginia Constitution, titled "Taxation and Finance", outlines the provisions related to property tax in the state. According to this article, all property shall be taxed except as otherwise provided. This includes both real estate and personal property.

The Virginia Constitution grants authority to cities, counties, and towns to administer local taxes on personal property and real estate. The tax rates vary depending on the locality. Real estate is assessed annually at fair market value, and the Board of Supervisors sets the general tax rate for all real property within the county.

The Virginia Constitution also provides exemptions from property taxation for certain classes of property. These include property owned by the Commonwealth or any political subdivision, as well as real estate and personal property owned and used exclusively by churches or religious bodies for religious worship or residences. Additionally, the Code of Virginia may exempt certain properties from taxation, such as those owned by non-profit charities.

Amendments to Article X have been made over the years to include additional exemptions and provisions related to property tax. For example, an amendment effective January 1, 2019, added a subsection exempting one motor vehicle owned and used by a veteran from taxation. Furthermore, the General Assembly has the discretion to impose franchise taxes on corporations in lieu of taxes on other property.

It is important to note that while the Virginia Constitution provides the framework for property taxation, specific tax rates, due dates, payment information, and exemptions may vary depending on the locality within the state.

The Evolution of Constitution: Section 98's Addition

You may want to see also

Explore related products

![]()

Sales tax

One section of Article X, Section 6 (a)(6), grants the authority to exempt certain classes of property from taxation. This includes property owned by the Commonwealth or its political subdivisions, as well as real estate and personal property owned and used exclusively by churches or religious bodies for religious worship or residences.

The Virginia sales tax is levied on the sale, lease, or rental of tangible personal property within the state, as well as certain services. The state sales tax rate is currently 4.3%, but local municipalities can have a total tax rate of up to 7%. The sales tax rate can vary depending on the locality and the type of item sold, leased, or rented. For example, food for home consumption, like grocery items, is taxed at a reduced rate of 2.5%. Additionally, certain essential personal hygiene items are also taxed at a reduced rate starting in 2020.

Dealers or retailers are generally responsible for collecting sales tax from their customers and remitting it to the Virginia Tax department when filing their sales tax returns. There are different categories of dealers, including in-state and out-of-state dealers, with specific registration requirements for each. Direct Payment Permits are also available for eligible companies, allowing them to purchase goods without paying sales tax upfront, provided they agree to pay the tax directly to Virginia Tax.

The US Constitution: How It Was Drafted

You may want to see also

Explore related products

![]()

Real estate tax

Article X of the Virginia Constitution, titled "Taxation and Finance", covers taxes. Real estate tax is a local tax, administered by cities, counties, and towns in Virginia. The Virginia Constitution states that real estate must be assessed in a uniform manner and at fair market value. The Board of Supervisors sets the general tax rate that applies to all real property in the county.

The Code of Virginia exempts some property from taxation, including property owned by the Commonwealth or any political subdivision, and real property and personal property owned by churches or religious bodies. This includes property used for religious worship, the residence of ministers, and adjacent land necessary for the convenient use of any such property.

The Constitution also allows for the exemption of property from taxation by classification. For example, energy-efficient buildings and improvements to real property designed for renewable energy production are considered separate classes of property and are taxed separately from other real property.

The General Assembly has the authority to impose franchise taxes on corporations and may make these taxes in lieu of taxes on other corporate property. Additionally, the Constitution outlines debt provisions related to taxation, stating that the General Assembly may authorize the creation of debt for capital projects upon an affirmative vote of a majority of the members of each house.

Verizon's New Line of Service: What You Need to Know

You may want to see also

Explore related products

![]()

Franchise tax

The Virginia Constitution mentions taxes in Article X, which is dedicated to "Taxation and Finance". This article outlines the role of the General Assembly in imposing taxes and managing the state's finances.

In Virginia, franchise taxes are imposed on the net capital of banks and trust companies. The state imposes a tax of $1 for every $100 of taxable value on January 1 each year, except for new banks. The franchise tax for new banks is prorated based on when they first transact business. For example, if a new bank first transacts business between April 1 and June 30, the tax is 75 cents for every $100 of net capital.

The constitution also mentions that the General Assembly may define and classify real estate for taxation purposes. This includes real estate devoted to agricultural, horticultural, forest, or open space uses. The General Assembly can authorize local governments to provide relief from taxes on such real estate if it is deemed to be in the public interest for the preservation of those lands.

In addition, the Virginia Constitution outlines that all taxes, licenses, and other revenues must be collected by the proper officers and paid into the State Treasury. No money can be paid out of this treasury except as authorized by law, and the state must ensure that expenses do not exceed total revenues.

The Constitution Empowers Courts: How and Why?

You may want to see also

Explore related products

![]()

State and local taxes

The Constitution of Virginia outlines the state's taxation and finance policies in Article X. This article includes provisions for state and local taxes, including property and franchise taxes.

Regarding state and local taxes, the Virginia Constitution stipulates that:

- All taxes, licenses, and other revenues of the Commonwealth shall be collected by the proper officers and deposited into the State treasury.

- No money shall be withdrawn from the State treasury unless authorized by law, and no appropriation shall be made for a period exceeding two years and six months after the end of the General Assembly session that enacted the authorizing law.

- The Governor shall ensure that expenses of the Commonwealth do not exceed total revenues on hand and anticipated within a specified period.

- The General Assembly may authorize the creation of debt for capital projects, provided that such projects are specified in the law and approved by a majority vote.

- No other or greater amount of tax or revenue shall be levied than is necessary for the government's expenses or to pay the Commonwealth's indebtedness.

In addition to these provisions, the Virginia Constitution also addresses property taxes and exemptions. It states that certain property, such as that owned by the Commonwealth or churches, is exempt from taxation. Furthermore, it grants the General Assembly the discretion to impose franchise taxes on corporations in lieu of taxes on other property.

Virginia has a progressive income tax system with four tax brackets, ranging from 2% for lower incomes to 5.75% for the highest earners. The state also collects sales tax at a rate of 5.3%, while some counties levy additional local sales taxes, resulting in combined sales tax rates of up to 7%.

Virginia also imposes a real estate tax, which is administered by local cities, towns, and counties. This tax is based on the assessed value of homes, with average tax bills varying across the state. Additionally, Virginia levies a personal property tax on vehicles, boats, tools, and business furniture, which is also administered at the local level.

Children of US Citizens: Are They Automatically Citizens?

You may want to see also

Frequently asked questions

Article X of the Virginia Constitution is about taxation and finance.

Article X of the Virginia Constitution mentions that all taxes, licenses, and other revenues of the Commonwealth shall be collected by its proper officers and paid into the State treasury. It also mentions that no money shall be paid out of the State treasury except in pursuance of appropriations made by law.

According to Article X, real estate, coal and other mineral lands, and tangible personal property (except the rolling stock of public service corporations) are subject to local taxation only.

Article X mentions that the General Assembly may authorize the creation of debt for capital projects, provided that the law specifies the capital projects and is approved by a majority of voters. It also states that the Governor should ensure that expenses do not exceed total revenues, including anticipated revenues over a period not exceeding two years and six months.