The question of which political party borrowed from Social Security has been a contentious issue in American politics, with significant implications for the program's sustainability and public trust. Historically, the Social Security Trust Fund has been utilized to balance the federal budget, with both Democratic and Republican administrations engaging in practices that effectively borrowed from the fund to finance other government expenditures. While the funds were legally transferred with the promise of repayment through Treasury bonds, critics argue that this practice undermines the financial stability of Social Security, particularly as the program faces long-term solvency challenges due to demographic shifts and economic pressures. This issue highlights the complex interplay between fiscal policy, political priorities, and the future of one of the nation's most vital safety net programs.

Explore related products

What You'll Learn

![]()

Democratic Party's Social Security Expansion

The Democratic Party has long advocated for expanding Social Security, positioning it as a cornerstone of their commitment to economic security and equity. Unlike the narrative often associated with borrowing from Social Security, Democrats frame their proposals as investments in the program’s sustainability and reach. Their expansion plans typically focus on increasing benefits, adjusting cost-of-living calculations, and raising revenue through progressive taxation rather than diverting funds. This approach contrasts with criticisms that other parties have "borrowed" from the trust fund to finance unrelated initiatives.

One key Democratic proposal involves boosting benefits for vulnerable populations, such as low-income seniors and survivors. For instance, the Social Security 2100 Act, championed by Democrats, would increase the special minimum benefit to ensure retirees above a certain age receive at least 125% of the federal poverty line. Additionally, it would adopt a Consumer Price Index for the Elderly (CPI-E) to more accurately reflect seniors’ spending on healthcare and housing, addressing the inadequacy of the current CPI-W. These adjustments aim to strengthen the program’s safety net without compromising its long-term solvency.

To fund these expansions, Democrats propose raising or eliminating the payroll tax cap, currently set at $168,600 (as of 2023). This would require higher earners to contribute a larger share, ensuring the program remains solvent for decades. For example, earnings above $400,000 could be subject to payroll taxes, generating an estimated $1.3 trillion over 10 years. This progressive approach aligns with the party’s broader tax policy, emphasizing fairness and shared responsibility. Critics argue this could burden businesses, but proponents counter that it’s a modest trade-off for securing millions of retirees’ financial stability.

A comparative analysis reveals that Democratic expansion plans differ fundamentally from past instances of "borrowing" from Social Security. In the 1980s, bipartisan reforms led to temporary surpluses in the trust fund, which were then used to offset federal deficits—a practice often criticized as raiding the program. Democrats’ current proposals, however, aim to reinvest in Social Security, ensuring it remains a robust pillar of the social safety net. By focusing on benefit increases and equitable funding, they seek to address both immediate needs and long-term sustainability.

Practical implementation of these expansions requires careful legislative strategy. Democrats must navigate partisan divides and public misconceptions about Social Security’s finances. Educating voters on the difference between strengthening the program and "borrowing" from it is crucial. For individuals, understanding these proposals means recognizing how they could directly impact retirement income, especially for those aged 62 and older. Advocates suggest contacting representatives, participating in town halls, and leveraging social media to amplify support for these reforms. The takeaway is clear: Democratic expansion plans are not about borrowing but about building a more secure future for all Americans.

ASPCA's Political Affiliations: Uncovering Their Party Support and Advocacy

You may want to see also

Explore related products

![]()

Republican Cuts to Social Security Funding

The Republican Party has historically advocated for reducing federal spending, often targeting entitlement programs like Social Security. While they haven’t directly "borrowed" from Social Security in the sense of transferring funds to other programs, their proposals to cut benefits or raise the retirement age effectively reduce the program’s funding by limiting its outflow. This approach, framed as fiscal responsibility, has sparked intense debate over the sustainability of Social Security and the role of government in ensuring economic security for retirees.

Consider the 2016 Republican Party platform, which called for "saving" Social Security by gradually increasing the retirement age and introducing means-testing for benefits. These measures would reduce the program’s long-term costs but would also lower benefits for millions of Americans, particularly those in lower-income brackets who rely heavily on Social Security for retirement income. For example, raising the retirement age to 70 would mean a 20% cut in monthly benefits for someone claiming at that age, according to the Social Security Administration’s actuarial tables.

A comparative analysis reveals that Republican proposals often contrast with Democratic approaches, which typically focus on expanding Social Security by increasing payroll taxes on higher earners or lifting the taxable wage cap. While Democrats argue this ensures solvency without cutting benefits, Republicans counter that such tax increases would stifle economic growth. However, the Congressional Budget Office has noted that cutting benefits disproportionately affects vulnerable populations, while tax increases could be structured to minimize economic impact by targeting those least likely to spend additional income.

To understand the practical implications, imagine a 65-year-old retiree earning the average Social Security benefit of $1,657 per month. Under a Republican plan to raise the retirement age, this individual might need to wait until 67 or 70 to claim full benefits, forcing them to either delay retirement or accept reduced payments. For someone with limited savings or health issues, this delay could be financially devastating. Advocates for cuts often overlook these real-world consequences, focusing instead on abstract budgetary targets.

In conclusion, while Republicans have not "borrowed" from Social Security in the traditional sense, their proposals to cut benefits or raise the retirement age effectively reduce the program’s funding by limiting payouts. These measures, though aimed at addressing long-term solvency, place a disproportionate burden on lower-income retirees. Policymakers must balance fiscal responsibility with the program’s core mission: providing economic security for America’s elderly. Practical alternatives, such as progressive tax adjustments, could achieve sustainability without undermining the safety net millions depend on.

Strengthening Democracy: The Vital Role of Political Parties in Governance

You may want to see also

Explore related products

![]()

Libertarian Views on Privatizing Social Security

Libertarians advocate for privatizing Social Security as a core tenet of their philosophy, emphasizing individual choice and market efficiency over government-managed programs. They argue that the current pay-as-you-go system, where current workers fund current retirees, is unsustainable due to demographic shifts and economic inefficiencies. Instead, they propose allowing individuals to invest a portion of their payroll taxes in private accounts, such as 401(k)-style plans, to harness the power of compound interest and stock market growth. This approach, they claim, would yield higher returns than the modest 1-2% annual increase in Social Security benefits, potentially doubling or tripling retirement savings over a 40-year career.

However, privatization is not without risks. Market volatility could expose individuals to significant losses, as seen during the 2008 financial crisis when retirement accounts plummeted. Libertarians counter this by suggesting diversified portfolios and safeguards, such as mandatory financial education for participants and government-backed insurance for catastrophic losses. They also propose a phased transition, starting with younger workers (e.g., those under 40) who have more time to recover from market downturns, while maintaining the current system for older workers nearing retirement.

Critics argue that privatization would undermine Social Security’s role as a safety net, leaving vulnerable populations at risk. Libertarians respond by advocating for a minimal guaranteed benefit funded by general revenues, ensuring a basic floor for all retirees while allowing those who opt for private accounts to pursue higher returns. They also highlight the success of similar models in countries like Chile and Sweden, where privatization has increased retirement savings and reduced dependency on government pensions.

A key libertarian argument is that privatization would reduce the government’s role in managing retirement funds, aligning with their broader goal of limiting state intervention in personal finances. They contend that individuals are better stewards of their own money than bureaucrats, pointing to the inefficiencies and unfunded liabilities of the current Social Security system, which the Social Security Administration projects will deplete its reserves by 2034. By shifting to private accounts, libertarians believe the system would become self-sustaining, freeing taxpayers from future bailouts.

In practice, implementing privatization would require careful planning. Libertarians suggest a multi-step process: first, allowing voluntary opt-ins for private accounts; second, gradually increasing the percentage of payroll taxes diverted to these accounts; and third, establishing a regulatory framework to protect investors. They also stress the importance of transparency, ensuring participants understand the risks and rewards of their investment choices. While privatization remains a contentious issue, libertarians see it as a necessary step toward empowering individuals and securing long-term retirement stability.

The Origins of Political Polling: A Historical Perspective

You may want to see also

Explore related products

![]()

Green Party's Social Security Reform Plans

The Green Party's approach to Social Security reform is rooted in sustainability, equity, and strengthening the program for future generations. Unlike parties that have historically borrowed from Social Security to fund other initiatives, the Green Party advocates for expanding benefits while ensuring long-term solvency through progressive revenue measures. Their plan challenges the notion that Social Security must be pared back, instead proposing a robust framework that addresses both current inadequacies and future fiscal challenges.

At the heart of the Green Party’s reform plan is the elimination of the payroll tax cap. Currently, wages above $160,200 are exempt from Social Security taxes, creating a regressive system where lower-income earners pay a higher proportion of their income. The Green Party proposes taxing all earned income, ensuring that high earners contribute proportionally. This change alone could extend Social Security’s solvency for decades, according to the Social Security Administration’s actuarial estimates. For example, a worker earning $500,000 annually would pay taxes on the full amount, significantly increasing revenue without burdening middle- or low-income households.

Another key component is the expansion of benefits to address poverty among seniors. The Green Party suggests increasing the minimum benefit to ensure no retiree lives below the federal poverty line. This would particularly benefit women, people of color, and low-wage workers, who are disproportionately affected by inadequate benefits. Additionally, the party proposes adjusting the cost-of-living allowance (COLA) to better reflect the spending patterns of seniors, such as healthcare costs, which rise faster than general inflation. For instance, a retiree relying on Social Security could see their annual benefit increase by an additional 1-2% under a more accurate COLA formula.

To further strengthen the program, the Green Party advocates for diversifying its revenue sources. One proposal is to introduce a financial transactions tax on Wall Street trades, which could generate billions annually without impacting everyday Americans. This approach aligns with the party’s broader commitment to economic justice, shifting the tax burden from working-class families to those who benefit most from the financial system. Critics argue this could reduce market liquidity, but proponents counter that a modest tax (e.g., 0.1% on stock trades) would have minimal impact on long-term investment while providing a stable funding stream for Social Security.

Finally, the Green Party emphasizes the importance of integrating Social Security reform with broader climate and economic policies. By investing in green jobs and infrastructure, the party aims to create a more resilient economy that supports both current workers and retirees. This holistic approach contrasts sharply with piecemeal reforms that focus solely on fiscal sustainability. For individuals, this means not only a more secure retirement but also a healthier planet for future generations. The Green Party’s vision is clear: Social Security should be a cornerstone of a just and sustainable society, not a program to be borrowed from or diminished.

Political Bias: How Parties Divide Citizens and Government

You may want to see also

Explore related products

![]()

Socialist Party's Universal Basic Income Proposals

The Socialist Party's Universal Basic Income (UBI) proposals stand out as a bold reimagining of social security, aiming to address systemic inequalities by providing a guaranteed income floor to all citizens. Unlike traditional welfare programs that target specific demographics or conditions, UBI is unconditional, offering a fixed amount—often proposed at $1,000 to $2,000 monthly—to every individual, regardless of employment status or income level. This approach borrows from the foundational principles of social security but expands its scope to ensure universal coverage, eliminating the bureaucratic inefficiencies and stigmatization often associated with means-tested programs.

Analytically, the Socialist Party’s UBI proposal is rooted in the belief that social security should evolve to meet the demands of a rapidly changing economy. Automation, gig work, and precarious employment have eroded traditional job stability, leaving millions vulnerable to poverty. By providing a baseline income, UBI aims to decouple survival from employment, fostering economic resilience and enabling individuals to pursue education, entrepreneurship, or caregiving without fear of destitution. Critics argue this could disincentivize work, but evidence from pilot programs in places like Finland and Stockton, California, suggests recipients often use funds to enhance productivity, not replace it.

Instructively, implementing UBI requires careful consideration of funding mechanisms. The Socialist Party typically advocates for progressive taxation, wealth taxes, and reallocation of military spending to finance the program. For instance, a 5% wealth tax on the top 1% could generate trillions annually, sufficient to fund a modest UBI. Practical tips for policymakers include phasing in UBI gradually, starting with vulnerable populations like the elderly or disabled, and pairing it with investments in healthcare and education to maximize societal benefits.

Persuasively, UBI aligns with the Socialist Party’s vision of a more equitable society by reducing income inequality and poverty rates. Studies estimate a $1,000 monthly UBI could cut poverty by 30-50%, particularly benefiting marginalized communities. Unlike social security, which often excludes gig workers or those with inconsistent employment histories, UBI ensures no one falls through the cracks. This universality also fosters solidarity, as all citizens share in the program’s benefits, reducing the political divisiveness often seen in targeted welfare debates.

Comparatively, while social security has been a cornerstone of American safety nets since the 1930s, its design reflects an outdated economic model. UBI, by contrast, is forward-looking, addressing 21st-century challenges like automation and climate displacement. For example, a coal worker laid off due to green energy transitions could use UBI to retrain for a new career without facing immediate financial ruin. This adaptability makes UBI a more sustainable and inclusive alternative to piecemeal social security reforms.

In conclusion, the Socialist Party’s UBI proposals represent a transformative expansion of social security principles, offering a universal, unconditional income to address modern economic challenges. By borrowing the core idea of collective support from social security but modernizing its structure, UBI promises to reduce inequality, enhance economic stability, and empower individuals in an increasingly uncertain world. While implementation requires careful planning, the potential benefits make it a compelling policy for the future.

Exploring Idaho's Political Landscape: Does an Independent Party Exist?

You may want to see also

Frequently asked questions

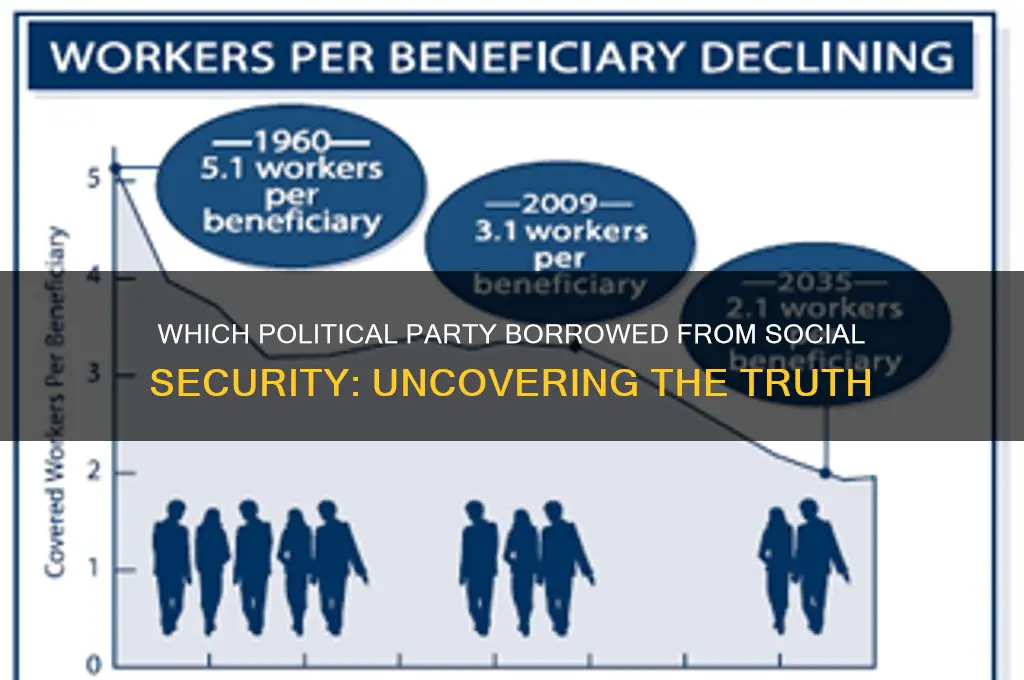

Both the Democratic and Republican parties have, at various times, utilized Social Security trust funds for general budget purposes, though the specifics and contexts differ.

As of recent estimates, the U.S. government owes the Social Security trust funds over $2.9 trillion, accumulated through decades of borrowing to fund other government programs.

Borrowing from Social Security can strain the system's long-term solvency, potentially leading to benefit cuts or tax increases if the funds are not repaid with interest, as required by law.