The topic of self-employment income on Schedule K-1 is a complex one, with many factors determining how to report self-employment earnings and losses. Schedule K-1 (Form 1065) is used by partners in a partnership to report their share of the partnership's income, deductions, credits, etc. Self-employment earnings are reported on Box 14 of Schedule K-1, and these earnings are generally subject to self-employment tax, which is an additional tax on top of regular income tax. The self-employment tax rate is typically 15.3%, but it was 13.3% in 2011. The IRS provides detailed instructions for Schedule K-1, including codes for various types of income, deductions, and credits. Understanding these codes is crucial for accurate reporting. Additionally, there are specific rules for partners in publicly traded partnerships (PTPs) and considerations for single-member LLCs within multi-member LLCs.

| Characteristics | Values |

|---|---|

| Self-Employment Earnings/Loss | Box 14 of Schedule K-1 (Form 1065) |

| General Partner's Income | Subject to self-employment tax |

| Limited Partner's Income | Not subject to self-employment tax (except for "guaranteed payments") |

| LLC Member Subject to Self-Employment Tax | Personal liability for LLC debts/claims, authority to contract on LLC behalf, participation in LLC business for >500 hours/year, LLC services in specific fields |

| Multi-Member LLC Income Reporting | Only Schedule K-1 information is entered for the investment |

| Single-Member LLC Income Reporting | Income and expenses reported on personal tax return (Schedule C), Schedule K-1 reported in K-1 section of personal return |

| Unreimbursed Expenses | Entered at the end of the Schedule K-1 process in TurboTax |

Explore related products

$15.97 $19.95

![]()

Self-employment earnings/loss

Self-employment earnings or losses are reported on Schedule K-1 (Form 1065). This form is used by partners in a partnership to report their share of the partnership's income, deductions, and credits. The self-employment earnings or losses are reported in Box 14 of Schedule K-1, under Code A.

If you have net income, losses, deductions, or credits from any activity to which special rules apply, the partnership will identify the activity and all related amounts on Schedule K-1 or on an attached statement. For example, if you have net income subject to recharacterization under certain tax regulations, you must report these amounts according to the instructions for Form 8582 or Form 8810.

If you are a general partner, the amount in Box 14, Code A may be reduced by certain unreimbursed employee expenses that were not reimbursed by the partnership. If the amount in Box 14, Code A is reduced for any reason, an explanation should be attached to the tax return.

It is important to note that self-employment earnings are generally subject to self-employment tax, which is imposed in addition to regular income tax. The self-employment tax rate is typically 15.3%, but it can vary from year to year. For example, in 2011, the rate was reduced to 13.3%.

Additionally, the treatment of self-employment income can vary depending on the structure of your business. For example, if you operate a single-member LLC that is a disregarded entity for tax purposes, the income and expenses of the LLC are reported on your personal tax return, typically on Schedule C. However, if your single-member LLC is a member of a multi-member LLC taxed as a partnership, you may need to report the Schedule K-1 income on Schedule E of your personal tax return.

Electoral Timetables: Constitutional Requirements for Elections

You may want to see also

Explore related products

![]()

Self-employment tax

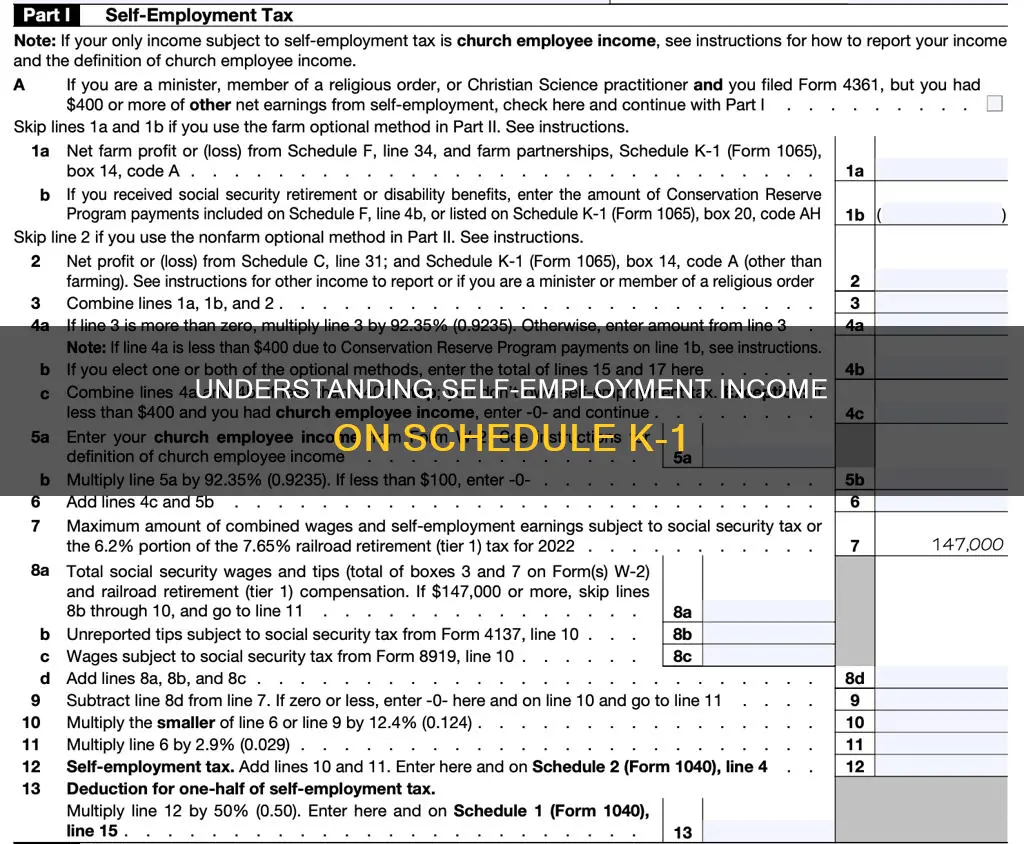

To calculate self-employment tax, use Schedule SE (Form 1040 or Form 1040-SR). You must pay self-employment tax and file Schedule SE if your net earnings from self-employment (excluding church employee income) were $400 or more, or if you had church employee income of $108.28 or more. When calculating your self-employment income, you can subtract half of your self-employment tax from your income before applying the tax rate. The self-employment tax rate consists of 12.4% for social security and 2.9% for Medicare. For 2024, the first $168,600 of your combined wages, tips, and net earnings are subject to the social security part of self-employment tax. If your total wages and tips are subject to social security tax and total at least $168,600, you do not need to pay the 12.4% social security part of the SE tax on any of your net earnings. However, all of your wages and tips are subject to the 2.9% Medicare part of the SE tax on all your net earnings.

If you use a tax year other than the calendar year, you must use the tax rate and maximum earnings limit in effect at the beginning of your tax year. Even if the tax rate or maximum earnings limit changes during your tax year, continue to use the same rate and limit throughout your tax year. You can deduct the employer-equivalent portion of your self-employment tax when calculating your adjusted gross income. This deduction only affects your income tax and does not affect your net earnings from self-employment or your self-employment tax.

In addition to self-employment tax, self-employed individuals must also pay income tax. To file your annual income tax return, you will need to use Schedule C (Form 1040) to report any income or loss from your business. If you have net income (loss), deductions, or credits from any activity to which special rules apply, the partnership will identify the activity and all amounts relating to it on Schedule K-1 or on an attached statement. Self-employment earnings from Schedule K-1 (Form 1065) are entered on Box 14 of the form.

Liveness and Live Migration: Defining Virtual Machine Uptime

You may want to see also

Explore related products

![]()

Net income

Self-employment earnings are specifically reported on Schedule K-1, and they constitute a significant component of net income for self-employed individuals. These earnings are subject to self-employment tax, which is levied in addition to regular income tax. The self-employment tax rate is generally 15.3%, although it may vary from year to year, such as in 2011 when it was reduced to 13.3%.

Schedule K-1 also accounts for deductions and credits that impact net income. For instance, if a partner has unreimbursed employee expenses, they can reduce their gross income amount in Box 14, Code A. Additionally, certain qualified expenditures can be deducted over a specified period under Section 59(e). Other credits and deductions, such as the low-income housing credit, qualified rehabilitation expenditures, and credits for increasing research activities, can also influence a partner's net income.

It's important to note that net income calculations on Schedule K-1 can be quite complex, especially when partners have multiple sources of income or expenses. Proper reporting of net income is essential for tax compliance, and partners should carefully review the instructions provided by the IRS to ensure accurate tax filings.

By carefully considering all sources of income, deductions, and credits, partners can determine their net income or loss using Schedule K-1. This information is crucial for tax reporting and ensures that partners are taxed appropriately on their share of partnership earnings.

The Election of 1800: Constitution's Testing Times

You may want to see also

Explore related products

![]()

Deductions

Self-employment income refers to the income earned by an individual working for themselves, rather than as an employee of a company. For individuals who are self-employed and working as part of a partnership, it is important to correctly account for self-employment taxes on Schedule K-1. This helps to determine the amount of self-employment tax owed.

Schedule K-1 can be used to report deductions for self-employed individuals who are part of a partnership. The deductions available depend on the individual's participation and status within the partnership. For general partners and active owners, the income may be considered earned income, and they may owe self-employment tax on it. Limited partners, on the other hand, do not pay self-employment tax on their distributive share of partnership income but do pay tax on guaranteed payments.

Other Deductions

In addition to self-employment deductions, Schedule K-1 can also be used for other types of deductions. For example, if a partnership records a loss over the tax year, partners can carry forward that loss to future years and deduct it from their taxable income. This can result in a tax deduction for the partner, reducing their overall tax liability for the year.

Furthermore, certain expenses that were not reimbursed by the partnership can also be deducted. If an amount is entered on Line 12 of the K-1 as a Section 179 Deduction, it will automatically pull to the menu. Additionally, deductions can be made for post-1986 depreciation adjustments, depletion (excluding oil and gas), and other alternative minimum tax (AMT) items.

Founding Fathers' Ages: Constitution Writers' Untold Story

You may want to see also

Explore related products

![]()

Credits

Firstly, self-employment earnings or losses are typically reported on Box 14 of Schedule K-1 (Form 1065). This includes net earnings or losses from self-employment, gross income from farming or fishing (Code B), and gross nonfarm income (Code C). These amounts are essential for calculating self-employment taxes accurately.

Secondly, various credits are available to self-employed individuals and partnerships. These credits can be found in Box 15 of Schedule K-1 and include a range of options, such as:

- Zero-emission nuclear power production credit (Code A)

- Credit for production from advanced nuclear power facilities (Code B)

- Low-income housing credit (Codes C and D)

- Qualified rehabilitation expenditures for rental real estate (Code E)

- Other rental real estate credits (Code F)

- Undistributed capital gains credit (Code H)

- Biofuel producer credit (Code I)

- Work opportunity credit (Code J)

- Disabled access credit (Code K)

- Empowerment zone employment credit (Code L)

- Credit for increasing research activities (Code M)

- Credit for employer social security and Medicare taxes (Code N)

Additionally, self-employed individuals may be able to claim certain deductions and expenses related to their business activities. For example, unreimbursed employee expenses that were not covered by the partnership can be deducted from Box 14, Code A. These deductions can impact the overall self-employment tax liability.

It's important to note that the specific credits and deductions available can vary depending on individual circumstances and the tax year in question. Therefore, it's always advisable to refer to the latest instructions provided by the Internal Revenue Service (IRS) and seek professional tax advice when preparing tax returns.

Framers' Vision: Guarding Against Tyranny in the Constitution

You may want to see also

Frequently asked questions

Schedule K-1 is a form that is used to report a partner's share of a partnership's income, losses, deductions, and credits. It is used to report self-employment income and losses.

Schedule K-1 is used by partners in a partnership to report their share of the partnership's income and losses. It is also used by members of a multi-member LLC to report their share of the LLC's earnings.

Self-employment income on Schedule K-1 includes net earnings from self-employment activities, gross income from farming or fishing, and gross nonfarm income. It also includes income from rental properties, trading personal property, and working interests in oil and gas wells.

Self-employment income is generally taxed at a rate of 15.3%. This tax is imposed in addition to regular income tax. Self-employment taxes are paid by partners in a partnership and members of an LLC who are considered self-employed.