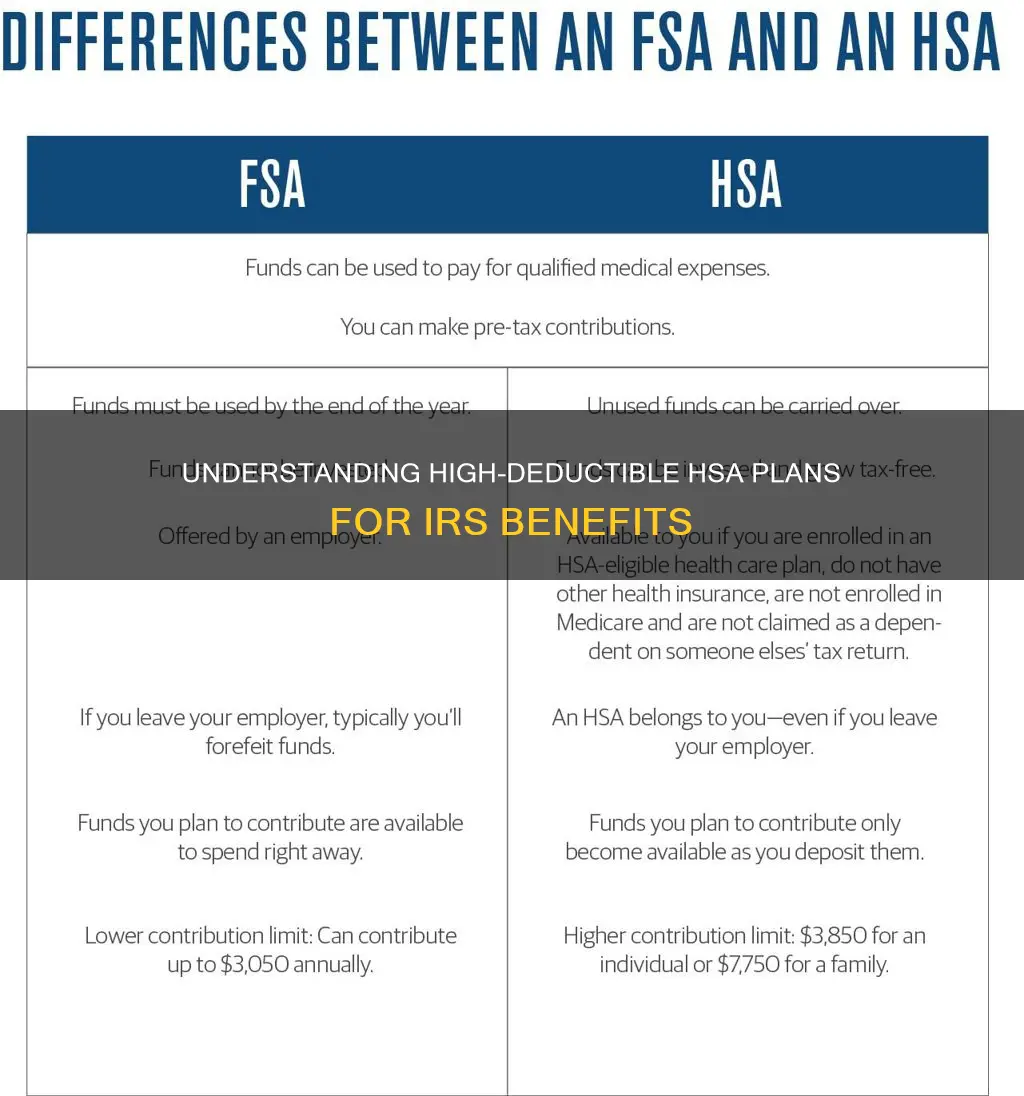

High-deductible health plans (HDHPs) are a type of savings account that allows individuals to set aside money on a pre-tax basis to pay for qualified medical expenses. These expenses include deductibles, copayments, coinsurance, and other out-of-pocket costs. HSA-eligible plans, also known as HDHPs, offer lower monthly premiums but typically require higher deductibles, which can be as high as the maximum out-of-pocket costs. Individuals can contribute to an HSA only if they have an HSA-eligible plan, and these contributions are either tax-deductible or pre-tax. The IRS defines qualified medical expenses, and HSA funds generally cannot be used to pay premiums. HSA balances roll over each year, allowing individuals to build up reserves for future healthcare needs.

| Characteristics | Values |

|---|---|

| Type of Account | Health Savings Account (HSA) |

| Type of Plan | High Deductible Health Plan (HDHP) |

| Eligibility | Employees eligible for FSAFEDS and enrolled in a Federal Employees Health Benefits (FEHB) Program |

| Tax Benefits | Pre-tax contributions, tax-deductible contributions, tax-free withdrawals for qualified medical expenses, tax-free savings, tax-free rollover |

| Qualified Medical Expenses | Dental, drug, vision, and some insurance premiums |

| Deductible | Minimum and maximum out-of-pocket costs set by the plan, can be as high as the maximum out-of-pocket costs |

| Contribution Limits | Catch-up contributions allowed up to $1,000 over the IRS maximum contribution limit |

| Reporting | Contributions reported on Form W-2, box 12, code W |

Explore related products

What You'll Learn

![]()

HSA-eligible plan deductibles

A Health Savings Account (HSA) is a type of savings account that allows you to set aside money on a pre-tax basis to pay for qualified medical expenses. HSA-eligible plans, also known as High Deductible Health Plans (HDHPs), have certain requirements and benefits that are important to understand.

Firstly, HSA-eligible plan deductibles tend to be significantly higher than the minimums set by the Internal Revenue Service (IRS). These deductibles can be as high as the maximum out-of-pocket costs allowed by the IRS. The minimum deductible is the amount you must pay for healthcare items and services per year before your insurance plan starts to pay. On the other hand, the maximum out-of-pocket costs represent the upper limit on what you would have to pay per year for healthcare.

By enrolling in an HSA-eligible plan, you may benefit from lower monthly premiums. The money deposited into your HSA can be used to pay for deductibles, copayments, coinsurance, and other qualified medical expenses, such as dental, drug, and vision care. It's important to note that HSA funds generally cannot be used to pay insurance premiums. Additionally, any unspent HSA funds will roll over from year to year, allowing you to build up reserves for future healthcare needs.

To contribute to an HSA, you must have an HSA-eligible plan. These contributions are either tax-deductible or pre-tax if made through payroll deductions. HSA contributions can reduce your overall taxable income, and the interest earned on HSA funds is not taxable. It's important to review the eligibility considerations for an HSA, including your financial position and ability to pay the annual net deductible amount.

For specific details on HSA-eligible plan deductibles, it is recommended to refer to IRS publications, such as IRS Publication 502, which provides a list of qualified medical expenses, and IRS Publication 969, which covers Health Savings Accounts and other tax-favored health plans. These publications offer valuable information on eligibility, contributions, and qualified expenses for HSAs.

Term Limits for Supreme Court Justices: What the Constitution Says

You may want to see also

Explore related products

![]()

Qualified medical expenses

A Health Savings Account (HSA) is a tax-exempt trust or custodial account that you set up with a qualified HSA trustee to pay or reimburse certain medical expenses you incur. You must be an eligible individual to contribute to an HSA. An HSA may receive contributions from an eligible individual or any other person, including an employer or a family member, on behalf of an eligible individual.

Contributions, other than employer contributions, are deductible on the eligible individual's return whether or not the individual itemizes deductions. Employer contributions are not included in income. Distributions from an HSA that are used to pay qualified medical expenses are not taxed.

The US Constitution: Self-Reference and Significance

You may want to see also

Explore related products

$15.99 $26.99

![]()

Tax-deductible contributions

A Health Savings Account (HSA) is a type of savings account that allows you to set aside money on a pre-tax basis to pay for qualified medical expenses. HSA-eligible plans, also known as High Deductible Health Plans (HDHPs), often have significantly higher deductibles than the minimum required. By enrolling in an HSA-eligible plan, you may benefit from a lower monthly premium. However, this also means that you will need to pay a higher amount out-of-pocket before your insurance plan starts to pay.

Your contributions to an HSA are either tax-deductible or pre-tax if made through payroll deduction. The money deposited in your HSA can be used to pay for deductibles, copayments, coinsurance, and other qualified medical expenses, such as dental, drug, and vision care. It's important to note that HSA funds generally cannot be used to pay insurance premiums.

The Internal Revenue Service (IRS) defines qualified medical expenses, and you can refer to IRS Publication 502 for a detailed list of these expenses. Additionally, IRS Publication 969 provides information on Health Savings Accounts and other tax-favored health plans. It is important to stay updated with the latest IRS publications, as they outline any amendments or changes to eligible expenses. For example, Public Law 117-169 amended Section 223 to include selected insulin products as having a $0 deductible for plan years beginning after 2022.

If you are considering an HSA, it is important to review your financial situation and determine if you can contribute enough to meet the annual net deductible amount. Additionally, if you are between the ages of 55 and 65, you may be able to make "catch-up contributions" of up to $1,000 over the IRS maximum contribution limit. By effectively utilizing an HSA, you can lower your overall healthcare costs and take advantage of tax savings.

Business Law: The Constitution's Impact

You may want to see also

Explore related products

![]()

Out-of-pocket expenses

A high-deductible health plan (HDHP) is a health insurance plan with a sizable deductible for medical expenses. An HDHP usually has a larger annual deductible than a typical health plan but charges lower monthly premiums. The minimum deductible varies from year to year.

The Internal Revenue Service (IRS) defines an HDHP as one with a deductible of at least $1,600 for individuals and $3,200 for families in 2024, or $1,650 and $3,300, respectively, in 2025.

A deductible is the portion of an insurance claim that the insured must pay out of pocket before the policy coverage is activated. Once an individual pays that portion of a claim, the insurance company covers the remaining portion, as specified in the contract.

HDHPs are believed to lower overall health care costs by making people more aware of the cost of medical expenses. The higher deductible also means lower insurance premiums, leading to more affordable monthly costs.

An HSA plan may save you money through lower premiums, tax savings, and money deposited in your account, which can be used to pay your deductible and other out-of-pocket medical expenses in the current year or in the future. HSA funds generally may not be used to pay premiums.

Under the tax law, HSA-eligible plans must set a minimum deductible and a limit, or maximum, on out-of-pocket costs for both individuals and families. The minimum deductible is the amount you pay for health care items and services per year before your plan starts to pay. The maximum out-of-pocket costs are the most you’d have to pay per year if you need more health care items and services.

Offer Letters: Employment Contracts or Not?

You may want to see also

Explore related products

![]()

Reimbursement and FSAFEDS

A Health Savings Account (HSA) is a type of savings account that lets you set aside money on a pre-tax basis to pay for qualified medical expenses. HSA funds can be used to pay for deductibles, copayments, coinsurance, and some other expenses. HSA-eligible plans must set a minimum deductible and a limit, or maximum, on out-of-pocket costs for individuals and families. The minimum deductible is the amount you pay for health care items and services per year before your plan starts to pay. The maximum out-of-pocket costs are the most you’d have to pay per year if you needed more health care items and services.

FSAFEDS is a program that offers reimbursement and payment options for eligible medical, pharmacy, dental, and vision expenses. To be eligible for reimbursement under FSAFEDS, you must be enrolled in a Federal Employees Health Benefits (FEHB) Program high-deductible health plan (HDHP) with an HSA. Eligible expenses under FSAFEDS include out-of-pocket costs for dental and vision care services/products that meet the IRS definition of medical care.

FSAFEDS offers several reimbursement and payment options, including:

- Paperless reimbursement: Claims are submitted electronically, and reimbursement is deposited directly into your bank account or sent to your health care provider.

- Pick and Process: You can choose which expenses you want to be processed for reimbursement and when.

- Direct reimbursement to health care providers: FSAFEDS can send payments directly to your health care or dependent care provider.

It's important to note that paperless reimbursement does not change your relationship or obligations to your healthcare provider, and it may not speed up the time it takes for your provider to submit or process a claim. Additionally, you are expected to make payments for your out-of-pocket expenses as requested by your provider.

George Mason's Post-Constitution: A Legacy of Rights

You may want to see also

Frequently asked questions

HSA-eligible plans, also known as High Deductible Health Plans (HDHP), are plans with deductibles that are often significantly higher than the minimums. These plans allow you to open a Health Savings Account (HSA) to pay for qualified out-of-pocket medical expenses using pre-tax dollars.

Qualified medical expenses include certain dental, drug, and vision expenses, as well as some preventive care benefits. The IRS defines and publishes a list of qualified medical expenses, which can be found on IRS.gov.

HSA-eligible plans offer the potential for lower monthly premiums and tax savings. HSA funds can be used to pay for deductibles, copayments, and other eligible expenses. Additionally, HSA balances roll over each year, allowing you to build up reserves for future medical needs.