Flood insurance is a separate policy from homeowners' insurance that covers losses caused by flooding. The National Flood Insurance Program (NFIP), established in 1968 and managed by the Federal Emergency Management Agency (FEMA), offers flood insurance to property owners, renters, and businesses in participating communities. This insurance covers buildings, contents, or both, with separate deductibles for each. The cause of flooding matters when determining coverage, and certain expenses are not covered by NFIP policies. Private flood insurance companies are also available for those who do not have access to NFIP insurance or want to compare rates. Purchasing flood insurance typically involves a waiting period before coverage takes effect, and rates are determined by factors such as the location and construction of the property. Understanding flood risk and taking steps to mitigate damage can help reduce the cost of flood insurance.

| Characteristics | Values |

|---|---|

| Who is it for? | Property owners, renters and businesses in participating communities |

| Who provides it? | The National Flood Insurance Program (NFIP), managed by FEMA, and delivered through a network of 47 insurance companies and the NFIP Direct |

| What does it cover? | Buildings, contents in a building, or both |

| What is the coverage limit? | Building coverage up to $250,000 and contents coverage up to $100,000 for homeowners. Commercial flood insurance covers up to $500,000 in flood damage. |

| What is not covered? | Currency, precious metals, stock certificates, vehicles, property outside the insured building, temporary housing expenses, etc. |

| How much does it cost? | The rate depends on the location, construction, and replacement cost of the property. |

| How long does it last? | The policy is typically valid for one year. |

| Is there a waiting period? | There is usually a 30-day waiting period for NFIP policies, but it may vary depending on specific circumstances. |

Explore related products

What You'll Learn

![]()

Flood insurance is a separate policy from homeowners insurance

The NFIP is delivered to the public by a network of more than 47 insurance companies and the NFIP Direct. There are also private flood insurance companies that offer coverage. When purchasing flood insurance, it is important to consider the waiting period before the policy goes into effect. For NFIP policies, there is typically a 30-day waiting period, while other policies may have shorter periods of 10 to 14 days.

The cost of flood insurance is determined by factors such as the location and construction of the property, as well as the cost of replacing it. There are ways to reduce the cost of flood insurance, such as by elevating the water heater or electrical panel, or by obtaining an elevation certificate. This certificate documents the building's elevation and can help to lower the premium.

It is worth noting that flood insurance does not cover all types of flood damage. For example, it typically does not cover damage from a sewer backup caused by clogged pipes. Additionally, there are certain items that are not covered by flood insurance policies, regardless of the cause of flooding. These items include currency, precious metals, stock certificates, cars, and property outside of the insured building, such as landscaping and fences.

Equality in the Original Constitution: Myth or Reality?

You may want to see also

Explore related products

![]()

The National Flood Insurance Program (NFIP) is managed by FEMA

The National Flood Insurance Program (NFIP) is managed by the Federal Emergency Management Agency (FEMA). The NFIP was established by Congress on August 1, 1968, with the passage of the National Flood Insurance Act (NFIA) of 1968, which has been modified over the years.

FEMA retains responsibility for underwriting flood insurance coverage sold under the program and by the NFIP Direct. The NFIP is a partnership between the federal government, the property and casualty insurance industry, states, local officials, lending institutions, and property owners. It is delivered to the public by a network of more than 47 insurance companies and the NFIP Direct.

The NFIP provides flood insurance to property owners, renters, and businesses, helping them recover faster when floodwaters recede. It offers two types of coverage: building coverage and contents coverage. Building policies cover up to $250,000 of flood damage, while content policies cover up to $100,000. Renters' flood insurance policies protect items inside the home, such as furniture, clothes, electronics, and artwork. Commercial flood insurance covers businesses' buildings and equipment, with each type of coverage protecting up to $500,000 in flood damage.

The NFIP works with communities required to adopt and enforce floodplain management regulations, helping to mitigate flooding effects. These regulations are based on FEMA's definition of a floodplain as the area that would be flooded by a base flood, which has a 1% chance of occurring in any given year. This is also known as a 100-year flood.

The Mitigation Division within FEMA manages the NFIP and oversees the floodplain management and mapping components of the program, aiming to reduce future flood damage and provide financial protection for property owners against potential losses.

Key Components of an Electronic Health Record

You may want to see also

Explore related products

$92.65 $162

![]()

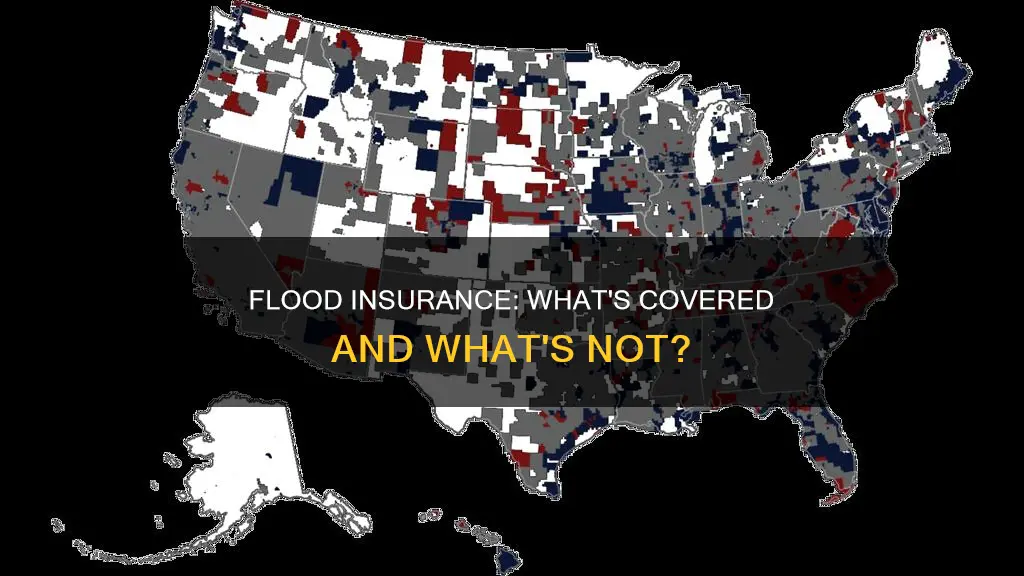

NFIP insurance isn't available in all areas

The National Flood Insurance Program (NFIP) is a federal program managed by the Federal Emergency Management Agency (FEMA) that offers flood insurance to households and businesses across the United States. The NFIP is delivered to the public by a network of more than 47 insurance companies and the NFIP Direct. It is a voluntary program in which participating communities adopt and enforce minimum floodplain management regulations that limit development in the FEMA-defined 1% annual chance floodplain.

However, NFIP insurance is not available in all areas. If it isn't available in your area, you can look for private flood insurance companies. Even if NFIP insurance is available, you may be able to get a lower rate from a private insurer. A local independent agent can help you find the best option.

NFIP insurance is available to anyone living in one of the 22,600 participating communities. These communities are spread across the United States, making flood insurance available to the vast majority of the nation's population. The program currently has over 5 million policies in force, providing nearly $1.3 trillion in coverage against floods.

It's important to note that there is typically a waiting period between purchasing flood insurance and when the coverage takes effect. For NFIP policies, the waiting period is usually 30 days, while other policies may have shorter periods of 10 to 14 days. There are some exceptions to the waiting period, such as when coverage is mandated by a government-backed lender or when there is a community flood map change.

Additionally, the cost of flood insurance varies depending on several factors, including the location and characteristics of the property, such as its elevation and number of floors. The NFIP provides resources and tools to help policyholders, agents, and servicers navigate the flood insurance process before, during, and after a disaster.

The Preamble's Length: A Concise Introduction to the Constitution

You may want to see also

Explore related products

![]()

Building and contents coverage are typically purchased separately

When it comes to flood insurance, building and contents coverage are typically purchased separately. This is because the two types of coverage serve different purposes and have distinct parameters.

Building coverage, as the name suggests, pertains to the physical structure of a home or commercial property. This includes damage to electrical and plumbing systems, water heaters, foundation walls, built-in appliances, cabinets, permanently installed carpets, detached garages, fuel and well water tanks, solar energy equipment, staircases, and window blinds. Building coverage is similar to dwelling coverage in a homeowners policy, and it is designed to protect the structural integrity of the property. The National Flood Insurance Program (NFIP) offers building coverage of up to $250,000, although private insurers like Neptune offer higher limits of up to $4 million.

On the other hand, contents coverage pertains to the items and belongings within the insured property. This includes electronics, valuable items such as original artwork or furs (typically up to a specified limit), washers, dryers, microwaves, portable air conditioners, and carpets installed over wood floors. Contents coverage is akin to personal property coverage in a homeowners or renters policy. The NFIP provides contents coverage of up to $100,000, while private insurers like Chubb can offer up to $500,000.

It is important to note that the NFIP has certain exclusions and limitations. For instance, it does not cover damage to swimming pools, hot tubs, landscaping, fences, wells, septic systems, or valuable papers. Additionally, coverage for basements is typically minimal. As such, homeowners may need to purchase additional coverage or opt for private flood insurance to ensure adequate protection.

When purchasing flood insurance, it is crucial to understand the specific needs of your property. Conducting a thorough inventory of your belongings and assigning values to them can help you determine the appropriate level of coverage required. By purchasing building and contents coverage separately, you can tailor your insurance plan to your unique circumstances, ensuring that your most valuable assets are protected in the event of a flood.

Work Email: Personal Data or Not?

You may want to see also

Explore related products

![]()

Flood insurance helps you recover faster

Floods can happen anywhere, and they can be incredibly costly. In fact, flooding is the most common natural disaster in the US, with 90% of all presidentially declared natural disasters involving flooding. The damage caused by just one inch of floodwater can cost thousands of dollars to fix.

Most homeowners and renters insurance policies do not cover flood damage. Only flood insurance covers the cost of rebuilding after a flood. Flood insurance is a separate policy that can cover buildings, the contents of a building, or both. The National Flood Insurance Program (NFIP) offers two types of flood insurance: building and contents, each with a separate deductible. Building coverage pays for flood damage to electrical and plumbing systems, water heaters, foundation walls, built-in appliances, detached garages, and more. Contents coverage protects belongings such as furniture, clothes, electronics, and artwork.

The NFIP is managed by the Federal Emergency Management Agency (FEMA) and delivered to the public by a network of more than 47 insurance companies. The NFIP works with communities to adopt and enforce floodplain management regulations that help mitigate flooding effects. The program provides insurance to help reduce the socioeconomic impact of floods, and it is the nation's largest single-line insurance program, providing nearly $1.3 trillion in coverage against floods.

The cost of flood insurance is based on factors such as the property's location, age, elevation, and the number of floors. Properties located in high-risk flood zones will have higher insurance rates. However, it's important to remember that flooding can happen anywhere, and nearly one-third of NFIP flood insurance claims come from outside high-risk flood areas.

By having flood insurance, you can recover faster when floodwaters recede. You don't have to go through the difficult process of rebuilding alone, and you can protect your most important assets—your home, your business, and your possessions.

Congressional Powers: What the Constitution Doesn't Allow

You may want to see also

Frequently asked questions

The NFIP is a federal program that enables property owners in participating communities to purchase insurance as a protection against flood losses. It is managed by FEMA and delivered to the public by a network of more than 47 insurance companies and the NFIP Direct.

Flood insurance covers losses directly caused by flooding. It offers two types of coverage: building coverage and contents coverage. Building policies cover up to $250,000 of flood damage, while content policies cover up to $100,000 of flood damage.

Your flood insurance rate is determined by three factors: where your property is built, how it's built, and what it would cost to replace it. Your premium is unique to your home, so if you live in a community with low flood risk, you'll pay less than someone in a high-risk area.

The first step is to get a quote using the NFIP Quote Tool. Once you have a quote, you can share it with an agent or call your insurance company. There is typically a 30-day waiting period for an NFIP policy to go into effect.