Tax expenditures are defined by law as revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability. These provisions are meant to support favoured activities or assist specific groups of taxpayers. They are often viewed as alternatives to direct spending programs or regulations to achieve the same goals. The special nature of these provisions is what distinguishes them from the normal tax code, and they can take the form of exclusions, deductions, deferrals, credits, and tax rates.

| Characteristics | Values |

|---|---|

| Definition | Revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability. |

| Examples | Exclusion of employer contributions for medical insurance premiums and medical care, Exclusion of net imputed rental income, Defined contribution employer plans, Capital gains, Child tax credits, Reduced rates of tax on dividends, and long-term capital gains |

| Agencies that do not count as tax expenditures | OMB and JCT do not count deductions for measuring income accurately, such as employers' deductions for employee compensation or interest expenses. |

| Agencies that publish lists of tax expenditures and estimates | Office of Management and Budget (OMB) and the Congressional Joint Committee on Taxation (JCT) |

| Tax expenditure estimates | Account only for changes in income taxes. |

| Tax expenditure programs | Considered "off-budget" spending by most economists and budget experts. |

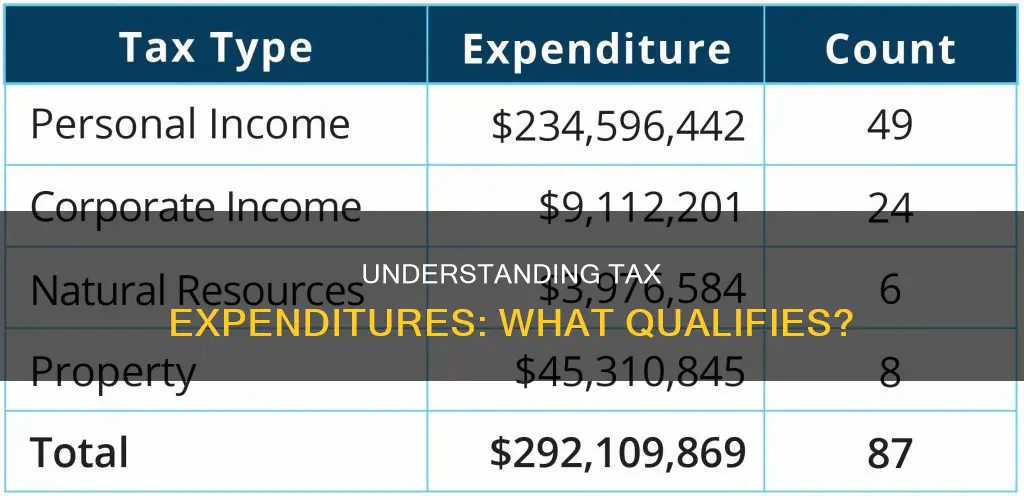

| Largest tax expenditures (FY2024 estimates) | Exclusion of employer contributions for medical insurance premiums and medical care ($231 billion), Exclusion of net imputed rental income ($152 billion), Defined contribution employer plans ($136 billion) |

| Largest tax expenditures (FY2019 estimates) | Exclusions from income: Employment-based health insurance (1.5% GDP) and pension contributions (1.2% GDP), Deductions from income: State and local taxes (0.6% GDP) and mortgage interest |

Explore related products

What You'll Learn

![]()

Tax expenditures are 'special'

Tax expenditures are indeed special. They are provisions of the tax code that reduce how much a taxpayer owes and, therefore, federal revenue. They are a departure from the "normal" tax code, providing a special exclusion, exemption, or deduction from gross income.

The Congressional Budget and Impoundment Control Act of 1974 defines tax expenditures as "revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability." The key word here is "special". Not all exemptions and deductions are counted as tax expenditures. For instance, the tax law permits deductions to measure income accurately, such as employers' deductions for employee compensation, and these are not considered tax expenditures.

Tax expenditures are often viewed as alternatives to other policy instruments, such as direct spending or regulatory programs. They can be used to influence or reward certain economic or social behaviour. For example, federal tax expenditures aid the development of renewable utility-scale electricity generation projects. They can also be used to reform the existing tax code, making it more efficient or in line with other countries.

Tax expenditures are considered "off-budget" spending by most economists and budget experts. They are easier to pass through Congress than increases in appropriations spending and, once in the tax code, they do not come up for annual review.

Dolley Madison's Influence on the US Constitution

You may want to see also

Explore related products

![]()

They are revenue losses

Tax expenditures are defined by law as "revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability". These exceptions are often viewed as alternatives to other policy instruments, such as spending or regulatory programs. They are a departure from the "normal" tax code, providing a subsidy for certain activities and influencing both axes of equity of the basic tax system.

The Congressional Budget and Impoundment Control Act of 1974 defines tax expenditures as "revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability". This definition highlights that tax expenditures are special provisions that result in revenue losses for the government.

These special provisions can include exclusions, deductions, deferrals, credits, and preferential tax rates. For example, the exclusion of employer contributions for medical insurance premiums and medical care is considered a tax expenditure, as it results in a revenue loss for the government. Similarly, the exclusion of net imputed rental income and defined contribution employer plans are also considered tax expenditures.

Tax expenditures are often used to influence or reward certain economic or social behaviour. For instance, tax credits for research and development are provided to encourage business investment in innovation. Additionally, tax expenditures can be used to promote certain social policies, such as providing tax breaks for homeowners, individuals with children, or those with employer-provided healthcare and pension insurance.

It is important to note that not all exemptions and deductions are considered tax expenditures. For example, deductions that are permitted by tax law to accurately measure income, such as employers' deductions for employee compensation or interest expenses, are not typically counted as tax expenditures. The determination of whether a provision is a tax expenditure depends on its relation to the "normal" tax code and the specific provisions included in the baseline tax code.

Military Oath: Defending the Constitution, a Sacred Duty

You may want to see also

Explore related products

![]()

They are provisions of the tax code

Tax expenditures are special provisions of the tax code that benefit specific activities or groups of taxpayers. They are determined based on their relation to the "normal" tax code. The U.S. Treasury defines them as "revenue losses attributable to provisions of the federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability." These exceptions are often viewed as alternatives to other policy instruments, such as spending or regulatory programs.

The Congressional Budget and Impoundment Control Act of 1974 defines tax expenditures as "revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability." This definition highlights that tax expenditures are special provisions that deviate from the standard tax code and provide benefits to certain individuals or activities.

Examples of tax expenditures include exclusions, deductions, and deferrals of income recognition. In fiscal year 2024, these three categories are expected to account for 61% of individual income tax expenditures. Other examples include special tax credits, such as the tax credit for qualified research expenses, which provides subsidies to encourage business investment in research and innovation. Renewable energy tax expenditures are another example, where the federal government aids the development of utility-scale renewable electricity generation projects through tax credits or other incentives.

It is important to note that not all exemptions and deductions are considered tax expenditures. For instance, deductions permitted by tax laws to measure income accurately, such as employers' deductions for employee compensation, are not typically counted as tax expenditures. The determination of whether a provision qualifies as a tax expenditure requires a clear definition of a normative or baseline system against which exceptions can be identified.

Tax expenditures can be viewed as subsidies for certain activities or groups, providing preferential treatment and influencing the equity of the basic tax system. They can also be used to influence or reward certain economic or social behaviors, such as encouraging investment in renewable energy projects or providing benefits to homeowners, individuals with children, or those with employer-provided healthcare.

Citing the Constitution: SBL Style Guide

You may want to see also

Explore related products

![]()

They can be exclusions, exemptions, or deductions

Tax expenditures are provisions of the tax code that can reduce how much a taxpayer owes and, therefore, federal revenue. They can be exclusions, exemptions, or deductions from gross income.

Exclusions refer to specific types of income that are not taxed. For example, employer contributions for medical insurance premiums and medical care, or net imputed rental income. Exemptions refer to a reduction in the amount of tax owed based on factors such as income level or family composition. For instance, the trend of tax exemptions on tips, overtime, and bonuses. Deductions lower the amount of tax owed by reducing the taxable income. An example of this is the mortgage interest deduction.

The Congressional Budget and Impoundment Control Act of 1974 defines tax expenditures as "revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income". The US Treasury defines them similarly, referring to "revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability".

It is important to note that not all exemptions and deductions are considered tax expenditures. For example, the tax law permits deductions to measure income accurately, such as employers' deductions for employee compensation, and these are not considered tax expenditures.

Artificial Heart: An Ongoing Treatment Option?

You may want to see also

Explore related products

![]()

They are alternatives to other policy instruments

Tax expenditures are special provisions of the tax code that benefit specific activities or groups of taxpayers. They are defined by law as "revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability". These exceptions are alternatives to other policy instruments, such as spending or regulatory programs.

Tax expenditures are often seen as alternatives to direct spending programs or regulations to achieve the same goals. They are considered "off-budget" spending by most economists and budget experts. They are viewed as free benefits, while government grants are seen as giveaways. Tax expenditures are also easier to pass through Congress than increases in appropriations spending. They only need to pass through two committees, the House Ways and Means and Senate Finance, whereas direct spending must go through the annual appropriations process.

Tax expenditures can be used to influence or reward certain economic activities or social behaviours. For example, federal tax expenditures have aided the development of utility-scale electricity generation projects, particularly renewable ones. They can also be used to encourage business investment in research to foster innovation and promote long-term economic growth.

Tax expenditures can also be used to provide social benefits and services, such as employee-provided healthcare, which was the largest tax expenditure in FY2024 with an estimated cost of $231 billion. Other social benefits include the exclusion of net imputed rental income ($152 billion) and defined contribution employer plans ($136 billion).

Overall, tax expenditures are a powerful tool that can be used as an alternative to other policy instruments to achieve various economic and social goals. They can be used to influence behaviour, encourage investment, and provide social benefits. However, they should be carefully considered and evaluated to ensure they are effective and fair.

Framers' Intent: Political Parties in Constitution Vision

You may want to see also

Frequently asked questions

Tax expenditures are defined by law as "revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability."

The key word in the definition is "special". Not all exemptions and deductions are considered tax expenditures. For example, the tax law permits deductions to measure income accurately, such as employers' deductions for employee compensation, and these are not considered tax expenditures.

Examples of tax expenditures include the exclusion of employer contributions for medical insurance premiums and medical care, the exclusion of net imputed rental income, and defined contribution employer plans.

Tax expenditures function as subsidies for certain activities, giving preferential treatment to those activities. For instance, two people with the same income can have different effective tax rates if one qualifies for tax expenditures by owning a home, having children, or receiving employer-provided health care and pension insurance.