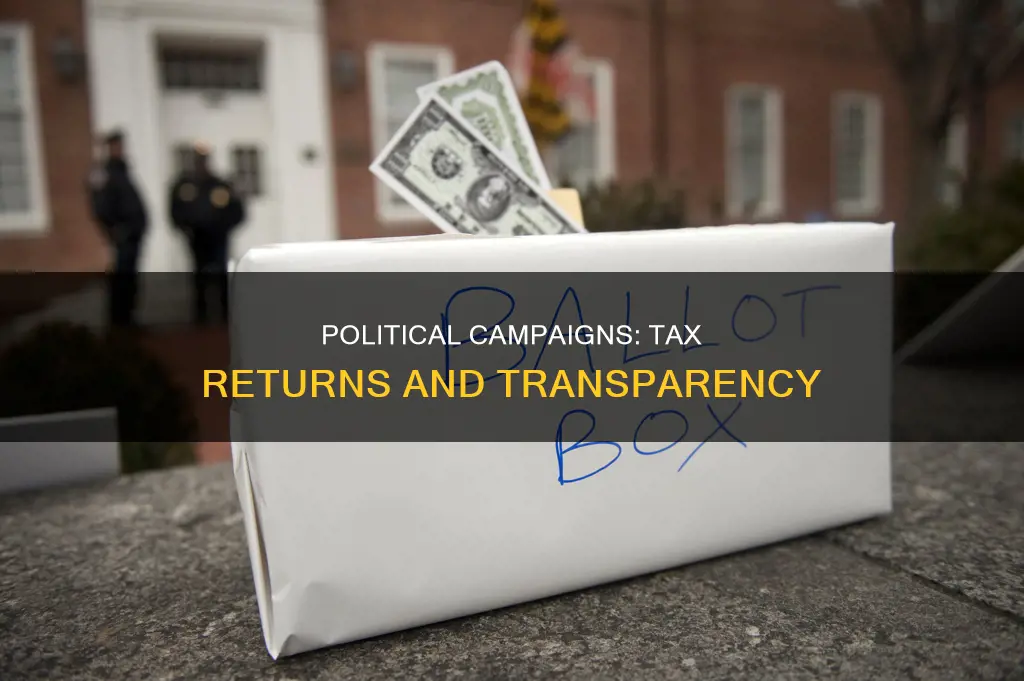

Political campaigns are subject to tax under IRC section 527 and may have filing requirements. This includes campaign committees for candidates for federal, state, or local office, as well as political parties and political action committees. These organizations are required to file periodic reports, such as Form 8872, with the IRS. The taxable income of a political organization includes exempt function income, such as contributions, membership dues, and proceeds from political fundraising events. While political contributions from individuals are not tax-deductible, taxpayers can choose to contribute a small amount, such as $3, to the Presidential Election Campaign Fund through their tax forms. This fund provides public funding for eligible presidential candidates' campaigns.

| Characteristics | Values |

|---|---|

| Are political campaigns subject to tax? | Yes, under IRC Section 527 |

| Are political contributions tax-deductible? | No |

| Do political campaigns file tax returns? | Yes, using Form 1120-POL, U.S. Income Tax Return for Certain Political Organizations |

| What is the tax calculated on? | Political organization taxable income, i.e. gross income excluding exempt function income |

| What is the tax calculated with? | Graduated rates specified in §11(b) |

| What is the tax paid with? | Form 1120-POL, U.S. Income Tax Return for Certain Political Organizations |

| What is the tax filing process? | Political organizations must file Form 8872, Political Organization Report of Contributions & Expenditures, electronically |

| Do citizens contribute to political campaigns through taxes? | Yes, through the Presidential Election Campaign Fund check box on federal tax forms |

Explore related products

What You'll Learn

![]()

Political donations are not tax-deductible

The same rule applies to businesses, which cannot deduct political contributions on their tax returns. This rule is very strict and even prevents political candidates from deducting their own out-of-pocket expenses incurred while running for office.

It is worth noting that while political donations are not tax-deductible, charitable donations generally are. However, it is important to distinguish between "nonprofit" and "charity" as they are treated differently by the tax code. While all charities are nonprofit organizations, not all nonprofits are charities. For example, nonprofit advocacy groups like the American Civil Liberties Union have a 501(c)(4) designation and cannot receive tax-deductible donations because they may engage in political activity.

If you are unsure whether an organization qualifies as a charity or a nonprofit, you can use the IRS's Tax-Exempt Organization Search Tool. To be considered tax-deductible, charitable donations must be made to organizations that are tax-exempt under §501(c)(3) of the Internal Revenue Code. These organizations are specifically barred from attempting to influence legislation or participating in any political campaigns.

Rack Cards: Effective Political Campaign Tool?

You may want to see also

Explore related products

![]()

Political organizations are taxed under IRC section 527

Political organizations, including political parties, campaign committees for candidates for federal, state, or local office, and political action committees, are subject to tax under IRC section 527. This means that they are required to file periodic reports with the IRS and may have additional filing requirements.

To comply with IRC section 527, political organizations must obtain an employer identification number (EIN) by filing Form SS-4, even if they do not have any employees. This number is necessary for filing tax returns. Additionally, many political organizations must electronically file their periodic reports using Form 8872, which details contributions and expenditures. To do so, they need the username and password issued by the IRS after filing their initial notice (Form 8871).

It is important to note that IRC section 527 also includes specific provisions for exemption from taxation. These requirements for exemption are outlined on the IRS website, along with information on solicitation notice requirements under IRC section 6113 and employment taxes for tax-exempt organizations.

Furthermore, IRC section 527(j) was amended to mandate the electronic filing of Form 8872 for periods starting on or after January 1, 2020. This form must be submitted by most tax-exempt political organizations to maintain their tax-exempt status. The form can be filed electronically through the "Political Organization Filing and Disclosure" link provided by the IRS.

In summary, political organizations are taxed under IRC section 527, which entails specific filing requirements and the need for an EIN. By adhering to these regulations, political organizations can ensure compliance with tax laws and maintain their tax-exempt status, if applicable.

Campaign Managers: Political and Marketing Strategists?

You may want to see also

Explore related products

![]()

Taxable income of political organizations

Political parties, campaign committees for candidates for federal, state, or local office, and political action committees are all considered political organizations under IRC § 527 and are subject to tax. These political organizations are generally required to file periodic reports and may have additional filing requirements with the Internal Revenue Service (IRS).

The taxable income of a political organization includes its gross income, excluding exempt function income, and any deductions allowed by the Code that are directly connected with producing that gross income. Specifically, exempt function income refers to income set aside for use by the political organization, which is received through the following means:

- Contributions of money or other property

- Membership dues, fees, or assessments from members

- Proceeds from political fundraising events, entertainment events, or the sale of political campaign materials outside the ordinary course of any trade or business

- Proceeds from conducting bingo games as defined in § 513(f)(2)

On the other hand, investment income or income from a trade or business, such as renting excess office space to an unrelated organization, is not considered exempt function income and is therefore subject to tax. It's important to note that if a political organization does not file a Form 8871 as required, its exempt function income becomes taxable for any period of time.

The tax on the taxable income of a political organization is calculated by multiplying the taxable income by the highest rate of tax specified in §11(b). However, if the organization is the principal campaign committee of a candidate for U.S. Congress, the tax is calculated using the graduated rates specified in §11(b). The tax is then paid using Form 1120-POL, U.S. Income Tax Return for Certain Political Organizations.

Social Media: Political Campaign's Best Friend

You may want to see also

Explore related products

$13.99 $35

![]()

Presidential Election Campaign Fund

Political parties, campaign committees for candidates for federal, state, or local office, and political action committees are all considered political organizations subject to tax under IRC section 527. These organizations are generally required to file Form 8872, Political Organization Report of Contributions & Expenditures, and may have additional filing requirements.

Now, when it comes to the Presidential Election Campaign Fund (PECF), this fund provides public financing for eligible presidential candidates to help cover qualified expenses for both the primary and general elections. The PECF is designed to reduce a candidate's dependence on large contributions from individuals and special interest groups. It is administered by the Federal Election Commission (FEC) and funded by voluntary contributions from taxpayers who can choose to direct a portion of their tax payments to the fund.

To be eligible for funding under the PECF, candidates must meet certain requirements, including agreeing to overall and state-specific spending limits, using funds only for legitimate campaign-related expenses, maintaining financial records, and permitting campaign audits. The FEC matches up to $250 of an individual's total contributions to an eligible candidate.

The PECF has evolved over the years, and the amount of funding available has changed. In recent years, there has been a decline in the number of taxpayers choosing to contribute to the fund, which has impacted the total amount available for presidential candidates.

Kamala's Fashion Choices: What Will She Wear Tonight?

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Political Organization Report of Contributions and Expenditures

Political organizations are subject to tax under IRC Section 527 and are required to file periodic reports. One such report is Form 8872, the Political Organization Report of Contributions and Expenditures. This form is used by tax-exempt Section 527 political organizations to report certain contributions received and expenditures made, unless an exception applies.

The following entities are considered political organizations under IRC Section 527 and may need to file Form 8872:

- Political parties

- Campaign committees for candidates for federal, state, or local office

- Political action committees

To file Form 8872 electronically, an organization must have the username and password it received from the IRS after filing its initial notice (Form 8871). The form can be filed using the “Political Organization Filing and Disclosure” link on the IRS website.

In addition to reporting contributions and expenditures on Form 8872, political organizations may also need to comply with other reporting requirements. For example, specific-purpose committees that accept political contributions or make expenditures on behalf of a candidate or officeholder must provide written notice to the affected candidate or officeholder by the end of the reporting period. This notice must include the full name and address of the committee and its campaign treasurer, and indicate that it is a specific-purpose committee.

Furthermore, there are specific reporting requirements for contributions and expenditures made using credit cards. Candidates or officeholders who accept political contributions made by credit card must report the full amount, including any processing fees deducted by the credit card issuer, as a political contribution. The deducted amount must then be reported as a political expenditure.

Campaign Strategies: Candidate's Critical Component

You may want to see also

Frequently asked questions

Yes, political parties, campaign committees for candidates for federal, state or local office, and political action committees are all political organizations subject to tax under IRC section 527 and may have filing requirements.

The tax is calculated by multiplying the political organization's taxable income by the highest rate of tax specified in §11(b). If the organization is the principal campaign committee of a candidate for U.S. Congress, the tax is calculated using the graduated rates specified in §11(b).

A political organization must have its own employer identification number (EIN), even if it does not have any employees. To get an EIN, an organization must file Form SS-4, Application for Employer Identification Number. Many political organizations must electronically file their periodic reports.

No, unlike charitable contributions, political contributions—whether to candidates, parties, or PACs—are not usually tax-deductible. This includes monetary donations, in-kind contributions, and volunteer expenses.

Yes, when filing federal taxes, individuals can choose to contribute $3 as a single filer or $6 if filing jointly to the Presidential Election Campaign Fund. Eligible presidential candidates can use this fund to pay for their political campaigns.

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)