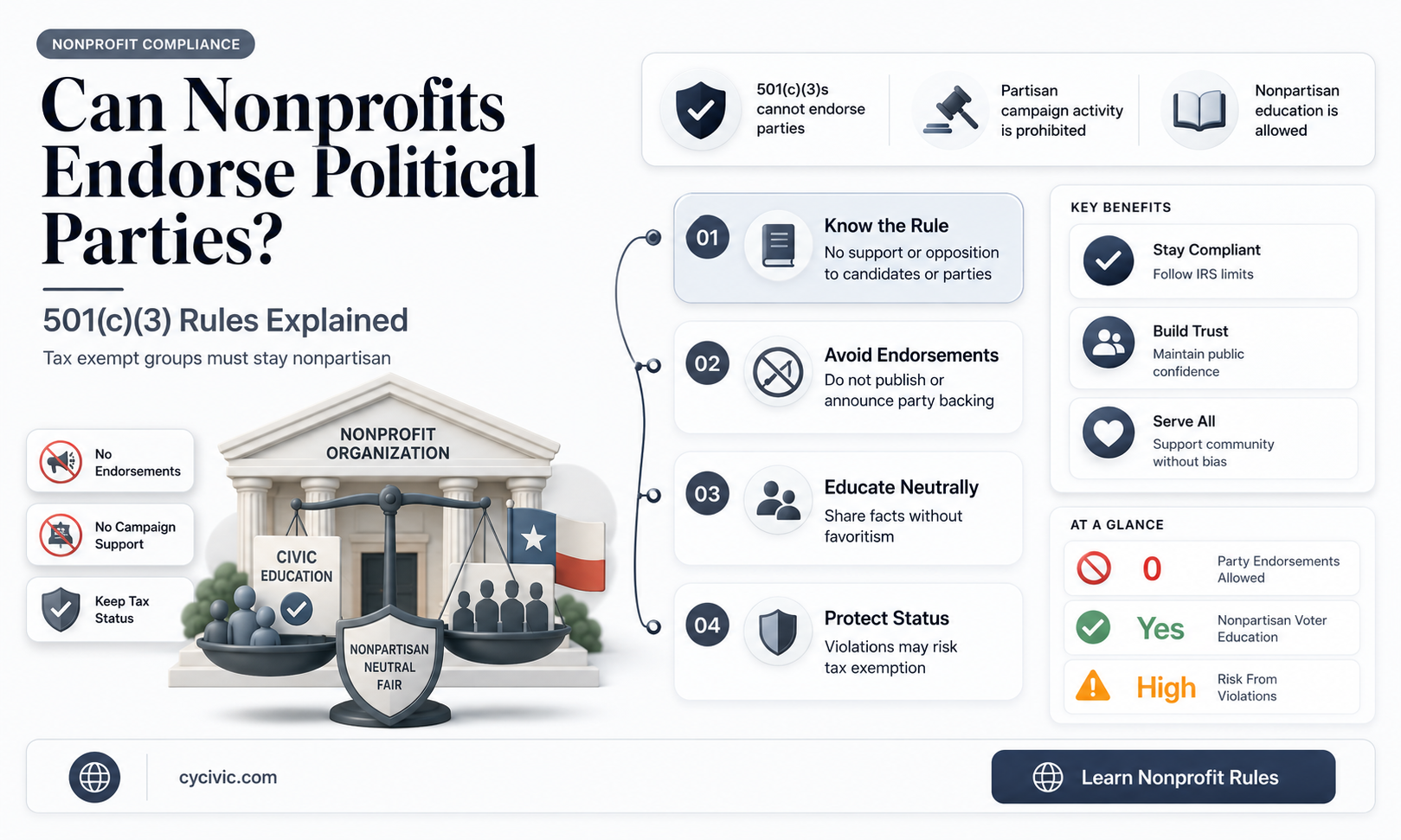

The question of whether a 501(c)(3) organization can promote a political party is a critical one, as it intersects with tax law, nonprofit regulations, and the principles of political neutrality. Under the Internal Revenue Code, 501(c)(3) organizations, which include charities, religious groups, and educational institutions, are granted tax-exempt status in exchange for a strict prohibition on engaging in partisan political activities. This means they cannot endorse or oppose political candidates, contribute to campaigns, or engage in any actions that could be construed as promoting a specific political party. Violating these rules can result in the loss of tax-exempt status and potential penalties. While 501(c)(3) organizations can address policy issues and advocate for social causes, they must do so in a nonpartisan manner, ensuring their activities remain focused on their charitable mission rather than advancing a political agenda.

| Characteristics | Values |

|---|---|

| Political Campaign Activity | Prohibited. 501(c)(3) organizations cannot participate in or intervene in political campaigns on behalf of or in opposition to any candidate for public office. |

| Voter Education | Allowed, but must be nonpartisan. Activities like voter registration drives, candidate forums, and issue advocacy are permissible if conducted in a neutral manner. |

| Lobbying | Limited. 501(c)(3) organizations can engage in some lobbying, but it must not constitute a substantial part of their activities. Excessive lobbying can result in loss of tax-exempt status. |

| Issue Advocacy | Permitted, as long as it is not tied to a specific candidate or political party. Advocacy must focus on issues, not electoral outcomes. |

| Endorsing Candidates | Prohibited. Endorsing, supporting, or opposing candidates for public office is strictly forbidden. |

| Political Contributions | Prohibited. 501(c)(3) organizations cannot make contributions to political parties, candidates, or PACs. |

| Nonpartisanship | Required. All activities must be nonpartisan and not favor or oppose any political party or candidate. |

| Consequences of Violation | Violating these rules can result in penalties, including fines, loss of tax-exempt status, or legal action. |

| IRS Oversight | The IRS enforces these rules and may audit organizations suspected of political activity violations. |

| Public Perception | Engaging in political activities can harm an organization's reputation and donor trust, even if not explicitly prohibited. |

Explore related products

What You'll Learn

- Legal Boundaries: IRS rules prohibit 501(c)(3) organizations from supporting or opposing political candidates

- Voter Education: Nonprofits can conduct nonpartisan voter education and registration activities

- Lobbying Limits: Limited lobbying is allowed, but excessive advocacy risks tax-exempt status

- Candidate Appearances: Hosting candidates is permitted if all parties are invited equally

- Issue Advocacy: Promoting issues is allowed, but not if tied to a specific party

![]()

Legal Boundaries: IRS rules prohibit 501(c)(3) organizations from supporting or opposing political candidates

The Internal Revenue Service (IRS) has established clear legal boundaries for 501(c)(3) organizations, which are primarily charitable, religious, educational, or scientific in nature. One of the most critical restrictions is the prohibition on supporting or opposing political candidates. This rule is rooted in the tax code and is designed to maintain the nonpartisan nature of these organizations while preserving their tax-exempt status. Specifically, the IRS prohibits 501(c)(3) entities from engaging in any activity that constitutes intervention in a political campaign on behalf of (or in opposition to) any candidate for public office. This includes endorsements, financial contributions, and even public statements that could be construed as favoring one candidate over another.

The rationale behind this restriction is to ensure that tax-exempt organizations remain focused on their charitable missions rather than becoming vehicles for political influence. When a 501(c)(3) organization endorses or opposes a candidate, it risks diverting resources and attention away from its core purpose. Additionally, allowing such activities could undermine public trust in these organizations, as donors and supporters may perceive them as politically biased rather than neutral actors working for the public good. Violating this rule can result in severe consequences, including the loss of tax-exempt status, fines, and other penalties.

While 501(c)(3) organizations cannot support or oppose political candidates, they are permitted to engage in certain nonpartisan political activities. For example, they can conduct voter education campaigns, host candidate forums, and advocate for specific policy issues, provided these activities are carried out in a fair and unbiased manner. The key distinction is that the organization must not favor or disfavor any particular candidate. Even subtle actions, such as inviting only certain candidates to speak or using language that implies endorsement, can cross the line into prohibited territory. Therefore, organizations must exercise caution and ensure all political activities are strictly nonpartisan.

It is also important to note that the IRS rules apply not only to the organization itself but also to its leaders and employees. Board members, officers, and staff of 501(c)(3) organizations must be mindful of their actions and statements, both in their official capacities and as private individuals, to avoid inadvertently violating the rules. For instance, while an individual is free to support a political candidate personally, they must clearly separate their personal views from their role within the organization to prevent any confusion or implication of organizational endorsement.

To navigate these legal boundaries effectively, 501(c)(3) organizations should establish clear policies and guidelines regarding political activities. This may include training staff and volunteers on permissible and prohibited actions, consulting legal counsel when in doubt, and maintaining detailed records of all activities to demonstrate compliance with IRS rules. By adhering to these guidelines, organizations can continue to pursue their missions without jeopardizing their tax-exempt status or public trust. In summary, while 501(c)(3) organizations have some latitude to engage in nonpartisan political activities, they must strictly avoid any actions that could be interpreted as supporting or opposing political candidates to remain within the legal boundaries set by the IRS.

Are Political Parties 501(c)(3) Organizations? Unraveling Tax Exemptions

You may want to see also

Explore related products

![]()

Voter Education: Nonprofits can conduct nonpartisan voter education and registration activities

Nonprofits holding a 501(c)(3) status play a crucial role in fostering civic engagement through nonpartisan voter education and registration activities. These organizations are uniquely positioned to empower individuals by providing them with the knowledge and tools necessary to participate in the democratic process. While 501(c)(3) nonprofits are strictly prohibited from endorsing or opposing political candidates or parties, they can—and should—engage in activities that promote informed and active citizenship. Voter education initiatives can include distributing nonpartisan guides that explain voting procedures, such as registration deadlines, polling locations, and the mechanics of casting a ballot. By focusing on the "how" of voting rather than the "who" or "what," nonprofits ensure compliance with IRS regulations while still making a meaningful impact.

One effective way nonprofits can conduct voter education is by organizing workshops, webinars, or community events that demystify the voting process. These activities can target underserved populations, such as first-time voters, young adults, or communities with historically low voter turnout. For example, a nonprofit might host a workshop that explains the structure of a ballot, including local and state races, ballot measures, and the importance of down-ballot positions. By providing clear, unbiased information, these organizations help voters feel more confident and prepared to participate in elections. Additionally, nonprofits can partner with schools, libraries, or community centers to reach a broader audience and amplify their educational efforts.

Voter registration drives are another critical component of nonpartisan voter education. Nonprofits can set up booths at public events, distribute registration forms, and assist individuals in completing them accurately. It’s essential for these activities to remain strictly nonpartisan, avoiding any language or materials that could be perceived as favoring a particular candidate or party. For instance, volunteers should be trained to answer questions about the registration process without steering individuals toward specific political affiliations. By focusing on accessibility and inclusivity, nonprofits can help ensure that all eligible citizens have the opportunity to register and vote.

Technology can also be leveraged to enhance voter education efforts. Nonprofits can create user-friendly websites or apps that provide step-by-step guides to voter registration, offer personalized voting plans, and include FAQs about the voting process. Social media campaigns can be used to disseminate information about upcoming elections, registration deadlines, and the importance of voting. These digital tools can reach a wide audience, particularly younger voters who are often more engaged with online platforms. However, it’s crucial to maintain a nonpartisan tone in all digital content, avoiding any endorsements or criticisms of candidates or parties.

Finally, nonprofits can collaborate with other nonpartisan organizations to maximize the impact of their voter education initiatives. Coalitions can pool resources, share best practices, and coordinate efforts to reach diverse communities. For example, a local nonprofit might partner with a national organization to access voter education materials or training programs. By working together, these groups can create a more informed and engaged electorate, strengthening the democratic process as a whole. In doing so, 501(c)(3) nonprofits fulfill their mission of serving the public good while adhering to the legal boundaries of their tax-exempt status.

Is the Alternative for Germany a Neo-Nazi Political Party?

You may want to see also

Explore related products

![]()

Lobbying Limits: Limited lobbying is allowed, but excessive advocacy risks tax-exempt status

C)(3) organizations, which are primarily charitable, religious, educational, or scientific in nature, enjoy tax-exempt status under U.S. law. However, this status comes with strict limitations on political activities, including promoting political parties or candidates. The IRS prohibits these organizations from engaging in *any* political campaign activity, such as endorsing or opposing candidates. While outright promotion of a political party is off-limits, the rules around lobbying are more nuanced. Limited lobbying is permitted, but only if it aligns with the organization’s mission and does not become a substantial part of its activities. This distinction is critical because excessive advocacy or lobbying can jeopardize the organization’s tax-exempt status.

The IRS defines lobbying as attempting to influence legislation, and it allows 501(c)(3) organizations to engage in two types of lobbying: direct and grassroots. Direct lobbying involves communicating with legislators or their staff to influence specific legislation, while grassroots lobbying aims to influence legislation by encouraging the public to contact legislators. However, these activities must remain within strict limits. The "substantial part test" is the traditional rule, which states that lobbying cannot be a substantial part of the organization’s overall activities. Alternatively, organizations can elect to follow the "501(h) expenditure test," which provides clear spending limits for lobbying based on the organization’s budget. Exceeding these limits can trigger penalties or even revocation of tax-exempt status.

It is crucial for 501(c)(3) organizations to distinguish between permissible lobbying and prohibited political activity. For example, advocating for policy changes related to their mission (e.g., a health organization lobbying for healthcare legislation) is allowed, but endorsing a political party or candidate that supports those policies is not. The line can be thin, and organizations must exercise caution to ensure their activities remain within legal boundaries. Transparency and documentation are key; organizations should maintain records of their lobbying efforts to demonstrate compliance with IRS rules if audited.

Excessive advocacy, particularly when it veers into promoting a political party, poses a significant risk. The IRS scrutinizes activities that appear to favor one party over another, even if indirectly. For instance, hosting events or publishing materials that disproportionately highlight one party’s stance on issues can be problematic. Organizations must focus on the issues themselves rather than aligning with a party’s agenda. Board members and staff should receive training on these distinctions to avoid unintentional violations.

To navigate these restrictions, 501(c)(3) organizations should adopt clear policies and procedures for lobbying and political activities. Consulting legal counsel or tax experts can provide additional guidance tailored to the organization’s specific circumstances. By staying informed and vigilant, organizations can advocate effectively within the bounds of the law while safeguarding their tax-exempt status. Ultimately, the goal is to balance mission-driven advocacy with compliance, ensuring that political neutrality remains a cornerstone of their operations.

Are Political Parties Unconstitutional? Exploring Legal and Historical Perspectives

You may want to see also

Explore related products

![]()

Candidate Appearances: Hosting candidates is permitted if all parties are invited equally

When considering whether a 501(c)(3) organization can host candidate appearances, it is crucial to understand the IRS guidelines regarding political activities. A 501(c)(3) is primarily a tax-exempt organization dedicated to charitable, educational, or religious purposes, and it is strictly prohibited from engaging in partisan political activities. However, hosting candidate appearances is permissible under certain conditions, the most critical being that all parties must be invited equally. This ensures the event remains non-partisan and aligns with the organization’s tax-exempt status. The IRS emphasizes that such events must not show bias toward any candidate or political party, and the organization must maintain strict neutrality.

To comply with IRS rules, 501(c)(3) organizations must design candidate appearances as educational opportunities for the public, not as platforms for promoting specific candidates. For example, hosting a forum where all candidates for a particular office are invited to discuss their positions on relevant issues is acceptable. The organization must provide equal speaking time and opportunities to all participating candidates, regardless of their party affiliation. Failure to invite all candidates equally or showing favoritism can jeopardize the organization’s tax-exempt status. Additionally, the event should be structured to encourage informed civic engagement rather than endorsing or opposing any candidate.

Practical steps for hosting such events include sending invitations to all qualified candidates well in advance and documenting the invitation process to demonstrate fairness. If a candidate declines the invitation, the organization should retain proof of the invitation and the candidate’s response. During the event, moderators must ensure questions are neutral and relevant to the issues, avoiding topics that could be seen as favoring one candidate over another. The organization should also avoid any activities that could be construed as campaigning, such as distributing campaign materials or allowing candidates to solicit donations or support.

It is also important for 501(c)(3) organizations to be mindful of the timing and context of candidate appearances. Hosting such events too close to an election or in a manner that appears to influence the outcome could raise red flags with the IRS. Organizations should consult legal or tax advisors to ensure compliance with all regulations. By adhering to these guidelines, 501(c)(3)s can host candidate appearances that foster public education and engagement without violating their tax-exempt status.

In summary, while 501(c)(3) organizations cannot promote political parties or candidates, they can host candidate appearances if all parties are invited equally and the event is conducted in a fair, non-partisan manner. This approach allows organizations to fulfill their educational mission while staying within the boundaries of IRS regulations. Careful planning, documentation, and adherence to neutrality are essential to ensure compliance and maintain the organization’s tax-exempt status.

Are Political Parties Essential for Zambia's Democracy and Governance?

You may want to see also

Explore related products

![]()

Issue Advocacy: Promoting issues is allowed, but not if tied to a specific party

C)(3) organizations, which are primarily charitable, religious, educational, or scientific in nature, are granted tax-exempt status by the IRS. One of the key restrictions for these organizations is the prohibition on engaging in political campaign activities. This means they cannot support or oppose any candidate for public office. However, 501(c)(3)s are allowed to engage in issue advocacy, which involves promoting or opposing specific issues or causes. The critical distinction is that issue advocacy must remain neutral regarding political parties or candidates. For example, a 501(c)(3) can advocate for environmental protection, healthcare reform, or education funding, but it cannot tie these issues to a specific political party or candidate. This ensures the organization remains focused on its mission without crossing into partisan politics.

When engaging in issue advocacy, 501(c)(3)s must be cautious to avoid any language or actions that could be construed as supporting or opposing a political party. For instance, an organization advocating for climate change legislation can lobby for specific policies but cannot endorse a party that supports those policies. Similarly, it can educate the public about the importance of an issue but must avoid framing the issue in a way that aligns with a particular party’s platform. The IRS evaluates advocacy activities based on the "facts and circumstances" of each case, so organizations should ensure their messaging is issue-focused and non-partisan. Clear, objective communication is essential to staying compliant with IRS regulations.

Another important consideration is the timing and context of advocacy efforts. During election seasons, 501(c)(3)s must be especially vigilant to avoid even the appearance of partisanship. For example, releasing a report on a critical issue just before an election could be misinterpreted as an attempt to influence the outcome if the issue aligns closely with a party’s stance. To mitigate this risk, organizations should maintain consistent advocacy efforts throughout the year, rather than concentrating them around election periods. Additionally, they should avoid coordinating their activities with political campaigns or parties, as this could jeopardize their tax-exempt status.

Transparency is also crucial for 501(c)(3)s engaged in issue advocacy. Organizations should clearly communicate their positions on issues and ensure their materials are educational rather than persuasive in a partisan sense. This includes providing balanced information and avoiding attacks on political parties or candidates. For example, a nonprofit advocating for criminal justice reform can highlight the need for policy changes but should refrain from criticizing a party that opposes those changes. By maintaining a neutral tone and focusing on the merits of the issue, organizations can effectively advocate without running afoul of IRS rules.

Finally, 501(c)(3)s should establish internal policies and guidelines to ensure compliance with IRS regulations regarding issue advocacy. This includes training staff and volunteers on the differences between permissible issue advocacy and prohibited political activity. Organizations may also seek legal counsel to review their advocacy materials and strategies, especially if they are navigating complex or high-profile issues. By taking proactive steps to remain compliant, nonprofits can continue to promote important causes while preserving their tax-exempt status and public trust. In summary, while 501(c)(3)s cannot promote political parties, they can and should engage in issue advocacy—as long as it remains focused on the issue itself and not on partisan politics.

Exploring Colombia's Political Landscape: Parties, Ideologies, and Influence

You may want to see also

Frequently asked questions

No, a 501(c)(3) organization cannot endorse or oppose political parties or candidates. Doing so risks losing its tax-exempt status.

Yes, but only in a limited and non-partisan manner. Activities like voter education, registration, and advocacy on issues are allowed, as long as they do not favor a specific party or candidate.

No, a 501(c)(3) cannot contribute funds, resources, or services to support a political party, candidate, or campaign.

Yes, employees can engage in political activities on their own time, but they must make it clear they are not representing the organization.

The organization may face penalties, including fines, loss of tax-exempt status, and legal action by the IRS for violating its non-partisan requirements.