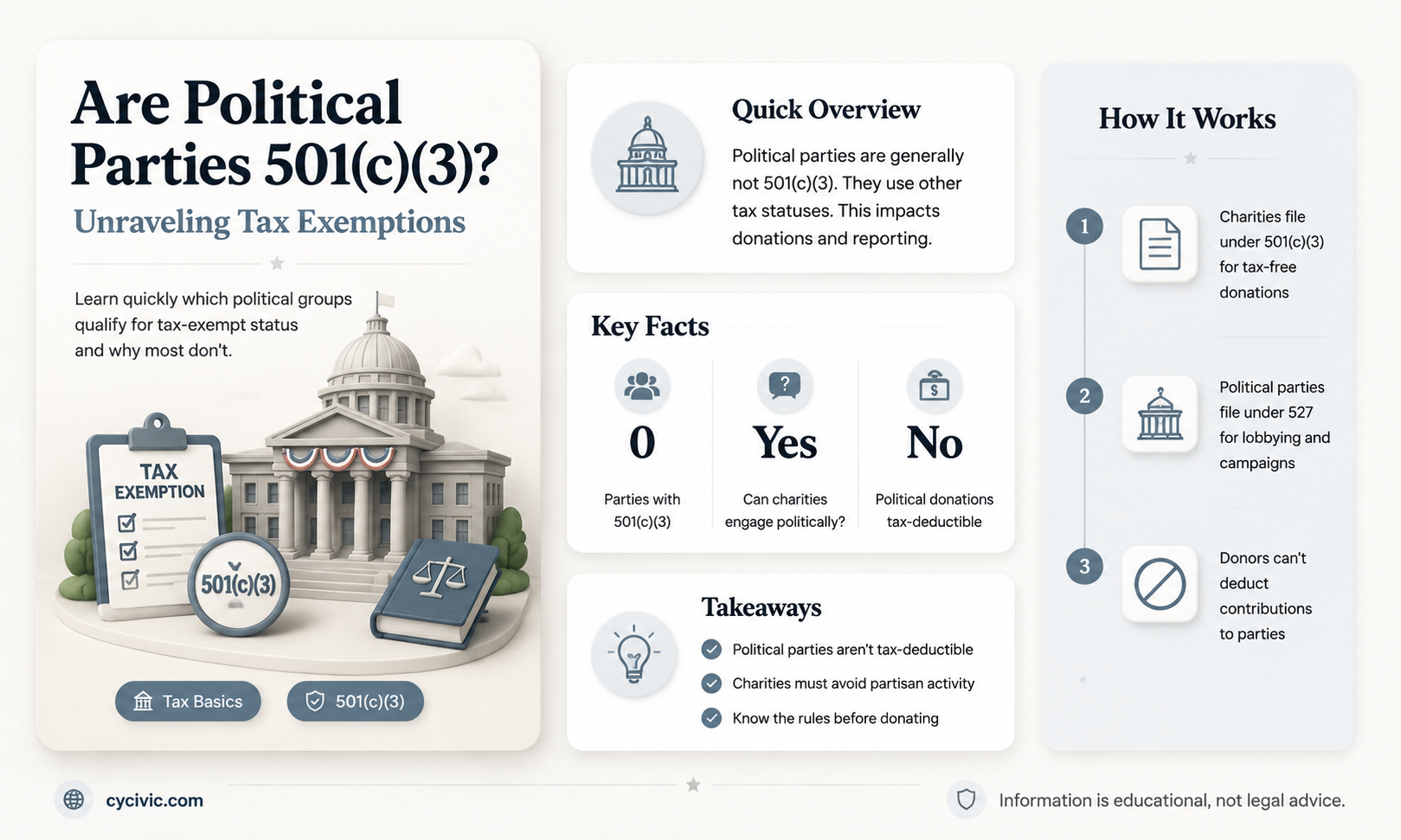

The question of whether political parties qualify as 501(c)(3) organizations under the U.S. Internal Revenue Code is a common point of confusion. A 501(c)(3) designation is reserved for charitable, religious, educational, or scientific organizations that operate exclusively for public benefit, and it prohibits substantial involvement in political campaigns or lobbying. Political parties, on the other hand, are primarily focused on influencing elections and government policies, which directly conflicts with the non-partisan requirements of a 501(c)(3). Instead, political parties typically fall under different tax classifications, such as 527 organizations, which are taxed on political activities but do not offer donors the same tax deductions as charitable contributions. Understanding these distinctions is crucial for both organizations and donors to ensure compliance with tax laws and avoid potential legal pitfalls.

| Characteristics | Values |

|---|---|

| Tax Exemption Status | Political parties are not eligible for 501(c)(3) status. |

| Primary Purpose | 501(c)(3) organizations must be primarily for religious, charitable, scientific, or educational purposes. Political parties focus on influencing elections and government. |

| Political Activity | 501(c)(3) organizations are strictly prohibited from engaging in political campaigns or endorsing candidates. Political parties are inherently political. |

| Donation Deductibility | Donations to 501(c)(3) organizations are tax-deductible. Donations to political parties are not tax-deductible. |

| Lobbying Restrictions | 501(c)(3) organizations can engage in limited lobbying, but not as their primary activity. Political parties are primarily focused on lobbying and advocacy. |

| IRS Classification | Political parties are typically classified under 527 organizations (political organizations) or other non-501(c)(3) categories. |

| Funding Sources | 501(c)(3) organizations rely on donations, grants, and fundraising. Political parties rely on campaign contributions, PACs, and party fundraising. |

| Transparency Requirements | Both 501(c)(3) organizations and political parties must file disclosures, but political parties face stricter FEC regulations. |

| Eligibility for Grants | 501(c)(3) organizations are eligible for government and private grants. Political parties are not eligible for such grants. |

| Public Perception | 501(c)(3) organizations are seen as non-partisan and charitable. Political parties are seen as partisan and politically driven. |

Explore related products

What You'll Learn

- Tax-Exempt Status: Are political parties eligible for 501(c)(3) tax-exempt status under IRS rules

- Political Activities: Limits on political campaigning and lobbying for 501(c)(3) organizations

- Donation Rules: Restrictions on tax-deductible donations to political parties under 501(c)(3)

- PAC vs. 501(c)(3): Differences between political action committees and 501(c)(3) organizations

- Legal Precedents: Court cases defining political parties’ relationship with 501(c)(3) status

![]()

Tax-Exempt Status: Are political parties eligible for 501(c)(3) tax-exempt status under IRS rules?

Under the Internal Revenue Code (IRC), section 501(c)(3) provides tax-exempt status to organizations operated exclusively for religious, charitable, scientific, literary, or educational purposes, among others. However, political parties do not qualify for this status due to the inherent nature of their activities. The IRS explicitly states that organizations primarily engaged in political campaign activities are ineligible for 501(c)(3) status. Political parties are formed to support or oppose candidates for public office, which directly conflicts with the requirement that 501(c)(3) organizations must not participate in any political campaign on behalf of (or in opposition to) any candidate for public office.

The IRS distinguishes between 501(c)(3) organizations and other tax-exempt entities, such as those under section 527 of the IRC, which specifically covers political organizations. Section 527 organizations, including political parties, are taxed differently and are required to disclose their donors and expenditures to the IRS. While they enjoy some tax benefits, they are not granted the same broad tax-exempt status as 501(c)(3) organizations. This classification ensures that political parties are subject to different regulations and limitations, particularly regarding their involvement in electoral activities.

For an organization to qualify for 501(c)(3) status, it must meet strict operational and organizational tests. One of the key requirements is the "exclusivity test," which mandates that the organization's primary activities must further its exempt purpose. Since political parties are fundamentally focused on influencing elections and supporting candidates, they fail to meet this test. Additionally, 501(c)(3) organizations are prohibited from engaging in substantial lobbying activities, another area where political parties typically exceed permissible limits.

It is important for political parties to understand that attempting to obtain 501(c)(3) status could lead to denial by the IRS and potential penalties. Instead, they should explore other tax classifications, such as section 527, which is specifically designed for political organizations. This ensures compliance with IRS rules and avoids jeopardizing their tax-exempt status or facing legal consequences.

In summary, political parties are not eligible for 501(c)(3) tax-exempt status under IRS rules due to their primary focus on political campaign activities. The IRS reserves 501(c)(3) status for organizations with exclusively charitable, educational, or similar purposes, which are distinct from the goals and operations of political parties. Understanding these distinctions is crucial for political organizations to navigate tax laws effectively and maintain compliance with federal regulations.

Are Major Parties Still Dominant in UK Politics?

You may want to see also

Explore related products

$15.97 $21.95

![]()

Political Activities: Limits on political campaigning and lobbying for 501(c)(3) organizations

C)(3) organizations, which include many charities, religious groups, and educational institutions, are granted tax-exempt status by the IRS under the condition that they operate exclusively for charitable, religious, educational, or other specified purposes. One of the most critical restrictions imposed on these organizations is the limitation on political activities, particularly political campaigning and lobbying. The IRS strictly prohibits 501(c)(3) organizations from engaging in any activity that constitutes political campaigning on behalf of or in opposition to any candidate for public office. This means that these organizations cannot endorse candidates, make donations to their campaigns, or use their resources to promote or oppose specific candidates. Violating this rule can result in the loss of tax-exempt status and potential penalties.

While 501(c)(3) organizations are barred from political campaigning, they are allowed to engage in some forms of lobbying, but only within strict limits. The IRS distinguishes between two types of lobbying activities: grassroots lobbying and direct lobbying. Grassroots lobbying involves attempts to influence legislation by encouraging the general public to contact legislators, while direct lobbying involves direct communication with legislators or their staff to influence legislation. To remain compliant, 501(c)(3) organizations must ensure that lobbying activities are not a substantial part of their overall activities. The IRS uses a facts-and-circumstances test or the "substantial part" test to determine whether an organization’s lobbying efforts exceed permissible limits. Exceeding these limits can jeopardize the organization’s tax-exempt status.

It is important to note that political parties are not eligible for 501(c)(3) status because their primary purpose is to influence elections and support candidates, which directly conflicts with the restrictions on political campaigning for 501(c)(3) organizations. Instead, political parties and other organizations primarily engaged in political activities may qualify for tax exemption under different sections of the tax code, such as 527 organizations, which are taxed differently and face fewer restrictions on political activities. This distinction highlights the IRS’s intent to separate charitable and educational activities from partisan political efforts.

For 501(c)(3) organizations, navigating the boundaries of permissible political activities requires careful planning and adherence to IRS guidelines. Organizations can engage in non-partisan voter education, such as registering voters or providing unbiased information about candidates’ positions, as long as these activities do not favor or oppose any candidate. Additionally, they can participate in issue advocacy, which involves promoting or opposing specific legislation without referencing candidates. However, even in these cases, organizations must ensure that their activities are not perceived as supporting or opposing a particular candidate. Clear documentation and transparency are essential to demonstrate compliance with IRS rules.

In summary, 501(c)(3) organizations must strictly avoid political campaigning while carefully managing any lobbying activities to stay within IRS limits. Political parties, due to their inherent focus on electoral politics, cannot qualify for 501(c)(3) status and are subject to different tax and regulatory frameworks. For 501(c)(3) organizations, maintaining tax-exempt status requires a clear understanding of these restrictions and a commitment to operating within the bounds of charitable, educational, or religious purposes. Organizations that fail to comply risk severe consequences, including loss of tax exemption and financial penalties, underscoring the importance of adhering to these rules.

Judicial Independence: Are Judges Legally Bound to Shun Political Parties?

You may want to see also

Explore related products

![]()

Donation Rules: Restrictions on tax-deductible donations to political parties under 501(c)(3)

In the United States, the tax code imposes strict restrictions on tax-deductible donations to political parties, particularly under the 501(c)(3) designation. Organizations classified as 501(c)(3) are primarily charitable, religious, educational, or scientific in nature and are prohibited from engaging in partisan political activities. This means that donations made to 501(c)(3) organizations are generally tax-deductible for the donor, but these organizations cannot directly support or oppose political candidates or parties. As a result, political parties themselves cannot qualify as 501(c)(3) entities because their primary purpose is to influence elections and support specific candidates, which is inherently partisan.

Donors must understand that contributions to political parties are not tax-deductible under any circumstances. The Internal Revenue Service (IRS) clearly distinguishes between donations to 501(c)(3) organizations and those to political parties or candidates. While donations to 501(c)(3) organizations may qualify for tax deductions, contributions to political parties, campaigns, or political action committees (PACs) are considered personal expenses and do not provide any tax benefits. This rule ensures that taxpayers do not receive deductions for activities aimed at influencing elections, which could otherwise be seen as subsidizing political participation with public funds.

Even when 501(c)(3) organizations engage in activities that might seem politically related, such as voter education or advocacy on public policy issues, they must adhere to strict guidelines to maintain their tax-exempt status. For example, a 501(c)(3) organization can educate the public on issues like healthcare or climate change, but it cannot endorse or oppose specific candidates or parties. If a donor contributes to such an organization with the intent to support its non-partisan activities, the donation may be tax-deductible. However, if the donation is earmarked for partisan activities or directed toward political campaigns, it loses its tax-deductible status.

Another important restriction involves the use of donor funds by 501(c)(3) organizations. These organizations cannot allocate donations to support political parties or candidates, even if the donor expresses a preference for such use. Doing so would violate the organization’s tax-exempt status and could result in penalties, including loss of 501(c)(3) designation. Donors must therefore be cautious and ensure their contributions are used for non-partisan purposes if they seek a tax deduction. Transparency in how donations are utilized is critical for both the organization and the donor to remain compliant with IRS regulations.

In summary, political parties are not eligible for 501(c)(3) status, and donations to them are never tax-deductible. While 501(c)(3) organizations can engage in certain politically related activities, they must do so in a non-partisan manner to maintain their tax-exempt status. Donors should carefully consider the purpose of their contributions to ensure compliance with IRS rules and avoid mistakenly claiming deductions for non-qualifying donations. Understanding these restrictions is essential for both organizations and individuals to navigate the complexities of tax-deductible giving in the political landscape.

Why Many Voters Are Rejecting Political Party Affiliations Today

You may want to see also

Explore related products

![]()

PAC vs. 501(c)(3): Differences between political action committees and 501(c)(3) organizations

Political Action Committees (PACs) and 501(c)(3) organizations are both entities involved in advocacy, but they serve distinct purposes and operate under different legal frameworks. A PAC is primarily formed to raise and spend money to elect or defeat political candidates. These committees are highly regulated by the Federal Election Commission (FEC) and must disclose their donors and expenditures regularly. PACs can contribute directly to political campaigns, run ads supporting or opposing candidates, and engage in other partisan activities. Their focus is explicitly political, and they are not tax-exempt under the Internal Revenue Code (IRC).

In contrast, 501(c)(3) organizations are nonprofit entities recognized by the IRS as tax-exempt under the IRC. These organizations are typically charitable, religious, educational, or scientific in nature and are prohibited from engaging in partisan political activities. While 501(c)(3)s can advocate for issues and engage in lobbying within certain limits, they cannot endorse or oppose political candidates. Violating these rules can result in the loss of their tax-exempt status. The primary purpose of a 501(c)(3) is to serve the public good, not to influence elections.

One of the key differences between PACs and 501(c)(3)s is their funding and disclosure requirements. PACs must disclose their donors and expenditures to the FEC, ensuring transparency in political spending. Donors to PACs can contribute directly to political causes but cannot claim tax deductions for their contributions. On the other hand, donations to 501(c)(3) organizations are tax-deductible for the donor, incentivizing charitable giving. However, 501(c)(3)s are not required to disclose their donors publicly, which can lead to less transparency compared to PACs.

Another critical distinction lies in their activities and limitations. PACs have broad latitude to engage in political campaigns, including direct contributions to candidates and partisan advertising. They are designed to be political tools for individuals, corporations, or unions. Conversely, 501(c)(3)s must remain nonpartisan and focus on their mission-driven work. While they can engage in advocacy, it must be issue-based and cannot support or oppose specific candidates. This restriction ensures that tax-exempt resources are not used to influence elections.

In summary, PACs and 501(c)(3) organizations differ fundamentally in their purpose, activities, and legal treatment. PACs are political entities focused on electing candidates, with strict disclosure requirements but no tax benefits for donors. In contrast, 501(c)(3)s are tax-exempt nonprofits dedicated to public service, prohibited from partisan politics, and offering tax deductions for donations. Understanding these differences is essential for individuals and organizations navigating the complex landscape of political and charitable engagement.

Shifting Allegiances: Are Voters Abandoning Party Loyalty in Modern Politics?

You may want to see also

Explore related products

![]()

Legal Precedents: Court cases defining political parties’ relationship with 501(c)(3) status

The relationship between political parties and 501(c)(3) status has been shaped by several key court cases that clarify the boundaries of what organizations with this tax-exempt designation can and cannot do in the political arena. One of the foundational cases is Branch Ministries v. Rossotti (2001), where the U.S. Court of Appeals for the District of Columbia Circuit upheld the IRS's revocation of a 501(c)(3) organization's status due to its substantial involvement in political campaigning. The court emphasized that 501(c)(3) organizations are prohibited from engaging in any amount of political campaign activity, reinforcing the strict separation between charitable and political activities.

Another critical case is Americans United for Separation of Church and State v. IRS (2000), which addressed the issue of churches and religious organizations holding 501(c)(3) status while potentially engaging in political activities. The court ruled that the IRS's failure to enforce restrictions on political campaigning by churches violated the Establishment Clause of the First Amendment. This case underscored the importance of maintaining the non-partisan nature of 501(c)(3) organizations, even for religious entities, to ensure they do not become vehicles for political parties.

In FEC v. Wisconsin Right to Life, Inc. (2007), the U.S. Supreme Court further delineated the limits of political activity for 501(c)(3) organizations. While the case primarily focused on campaign finance laws, it reinforced the principle that organizations with 501(c)(3) status must avoid any activity that could be construed as endorsing or opposing political candidates. The court’s decision highlighted the need for clear distinctions between issue advocacy, which may be permissible, and direct political campaigning, which is strictly prohibited for 501(c)(3) entities.

A more recent case, Tea Party Groups v. IRS (2018), brought attention to the IRS's scrutiny of political organizations applying for 501(c)(3) or 501(c)(4) status. While not directly involving political parties, the case illustrated the challenges organizations face when their activities blur the lines between social welfare and political advocacy. The settlement emphasized the importance of transparency and adherence to IRS guidelines for maintaining tax-exempt status, further clarifying that political parties are not eligible for 501(c)(3) status due to their inherently partisan nature.

These legal precedents collectively establish that political parties cannot qualify for 501(c)(3) status because their primary purpose is to influence elections and support candidates, activities that are explicitly prohibited under this tax designation. Instead, political parties typically fall under 527 organizations, which are taxed differently and allow for political campaigning. The court cases reinforce the IRS's position that 501(c)(3) status is reserved for organizations dedicated to charitable, educational, or religious purposes, with no involvement in partisan political activities.

Interest Groups and Political Parties: Allies or Independent Forces?

You may want to see also

Frequently asked questions

No, political parties cannot be classified as 501(c)(3) organizations. 501(c)(3) status is reserved for charitable, religious, educational, or other specified nonprofit purposes, and it prohibits substantial involvement in political campaigns or lobbying.

Political parties are typically classified as 527 organizations under the Internal Revenue Code. These organizations are taxed on their political activities but can raise unlimited funds for political purposes, unlike 501(c)(3) organizations.

No, 501(c)(3) organizations are strictly prohibited from supporting or endorsing political parties or candidates. Doing so risks losing their tax-exempt status.

No, donations to political parties are not tax-deductible. Only donations to qualified 501(c)(3) organizations are eligible for tax deductions.