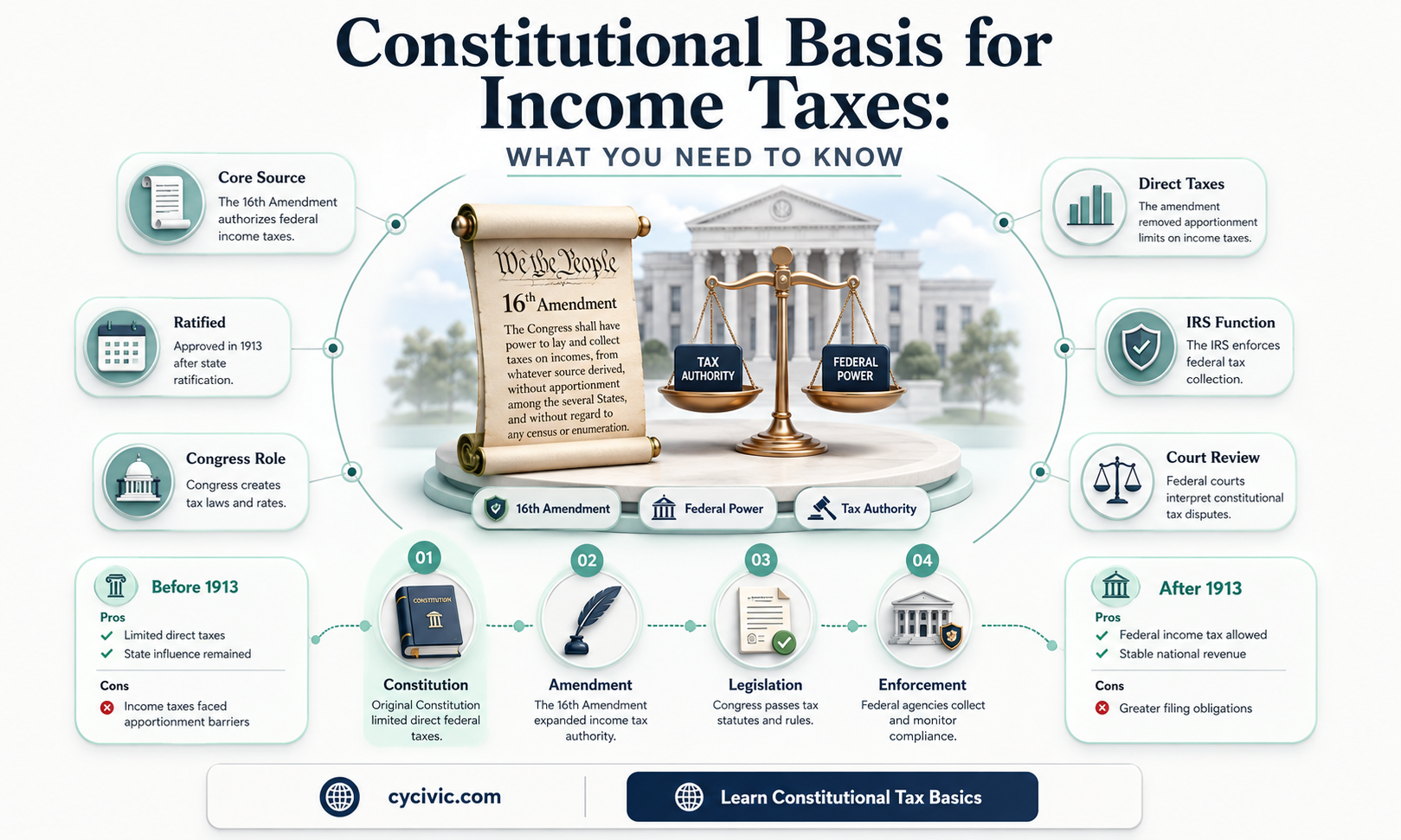

The 16th Amendment to the US Constitution, ratified on February 3, 1913, grants Congress the authority to collect income tax without apportioning it among the states based on population. This amendment was passed in response to the 1895 Supreme Court case of Pollock v. Farmers' Loan & Trust Co., which ruled that income tax was a form of direct taxation on property owners. The 16th Amendment effectively overruled this decision and allowed for the formal collection of income taxes in the United States, with the Revenue Act of 1913 being enacted soon after.

Explore related products

What You'll Learn

![]()

The 16th Amendment

The passage of the 16th Amendment had far-reaching social and economic impacts. It settled the constitutional question of how to tax income and dramatically changed the American way of life. It also shifted the primary source of federal revenue from tariffs and excise taxes to income taxes, which today account for the largest source of federal government revenue.

Understanding Differences in Excerpts Through Comparative Analysis

You may want to see also

Explore related products

![]()

Federal income tax laws

The power to collect income tax is also outlined in Article 1, Section 8, Clause 1 of the U.S. Constitution, also known as the Taxing and Spending Clause. This clause provides Congress with the general authority to "lay and collect Taxes, Duties, Imposts and Excises" to fund the operations of the federal government.

The 16th Amendment came about in response to the 1895 Supreme Court case of Pollock v. Farmers' Loan & Trust Co., where the Court ruled that a 2% income tax on incomes over $4,000 was unconstitutional as it was a "direct" tax on property owners that was not apportioned among the states. This ruling sparked concern among members of Congress about the accumulation of economic power by the wealthiest Americans.

The passage of the 16th Amendment effectively overruled the decision in Pollock, allowing for the reinstatement of the federal income tax through the Revenue Act of 1913. Today, the Internal Revenue Code, embodied as Title 26 of the United States Code, outlines the specific laws and regulations governing federal income tax in the U.S.

It is important to note that while all residents and citizens of the U.S. are subject to federal income tax, there are no provisions in the Internal Revenue Code that allow for tax credits or deductions based on race or ethnicity, such as the so-called "Black Tax Credit" or Native American reparations. Additionally, the First Amendment does not provide a right to refuse to pay income taxes based on religious or moral beliefs, despite claims made by some individuals and groups.

John Jay's Constitutional Beliefs: Federalism and Centralized Power

You may want to see also

Explore related products

![]()

Native Americans and tax

Native Americans are subject to federal income tax, just like every other American. However, there are some notable exceptions to this rule. Native Americans do not pay taxes on income derived from trust lands held for them by the U.S. or on income from federal Indian reservations. They are also exempt from state sales taxes on transactions made on these reservations.

The Internal Revenue Service (IRS) notes that Native Americans are generally expected to pay federal taxes. However, tribal governments are exempt from federal and state taxes. This is because federally recognized tribes are considered sovereign and are therefore immune from tax obligations.

The tax situation for Native Americans is complex and convoluted, with many conflicting court decisions and unclear laws. This is partly due to the history of Native American tribes being put on reservations, where they had little autonomy and were expected to assimilate or disappear. Today, Native American tribes continue to have a degree of self-government and can define the conditions of membership, regulate domestic relations, and levy taxes through their tribal governments.

The United States Constitution recognizes tribal sovereignty in several places. Article 1, Section 2 states that "Indians not taxed," indicating that the Founding Fathers viewed Native Americans as subjects of a separate sovereign and did not believe in taxation without representation. The commerce clause and the treaty clause also acknowledge tribal sovereignty.

Impeachment Power: Where in the Constitution?

You may want to see also

Explore related products

![]()

The Revenue Act of 1913

> "The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration."

The Oval Office: White House's Iconic Nerve Center

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

McCulloch v. Maryland (1819)

The Supreme Court, led by Chief Justice John Marshall, ruled in favour of McCulloch, concluding that the "'Necessary and Proper' Clause" of the U.S. Constitution grants Congress certain implied powers necessary and proper for the exercise of the powers explicitly enumerated in the Constitution. The Court determined that the federal government is supreme over the states, and therefore, the states' ability to interfere with the federal government is restricted. This decision established that Congress has the authority to establish a national bank and that states do not have the power to tax or impede the operations of a federal institution.

In his opinion, Chief Justice Marshall noted the difference between the Constitution and the Articles of Confederation, highlighting that the Tenth Amendment did not include the word "expressly." He redefined the meaning of "necessary" as something "appropriate and legitimate," covering all methods for furthering the objectives of the enumerated powers. Marshall's decision reaffirmed the principle that the federal government derives its sovereignty from the people, not the states, and this view has been widely accepted.

The McCulloch v. Maryland case set a significant precedent regarding the division of powers between the state and federal governments and addressed the issue of federal power and commerce. It clarified that Congress has the implied power to charter a bank and that states cannot use taxation to impede or control the operations of constitutional laws enacted by Congress. The case also influenced legal systems in other countries, such as Australia, where it was cited in the High Court case of D'Emden v Pedder (1904).

Research Engagement: Activities That Define Involvement

You may want to see also

Frequently asked questions

The 16th Amendment to the United States Constitution, passed in 1909 and ratified in 1913, grants Congress the authority to collect income tax without having to determine it based on population.

The 16th Amendment was significant as it effectively overruled a previous Supreme Court ruling in Pollock v. Farmers' Loan & Trust Co. (1895) and allowed for the formal collection of income taxes in the United States.

Progressive groups argued that it was fairer for wealthy individuals to pay income taxes rather than the middle class and poor, who had been burdened by tariffs and taxes.

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)