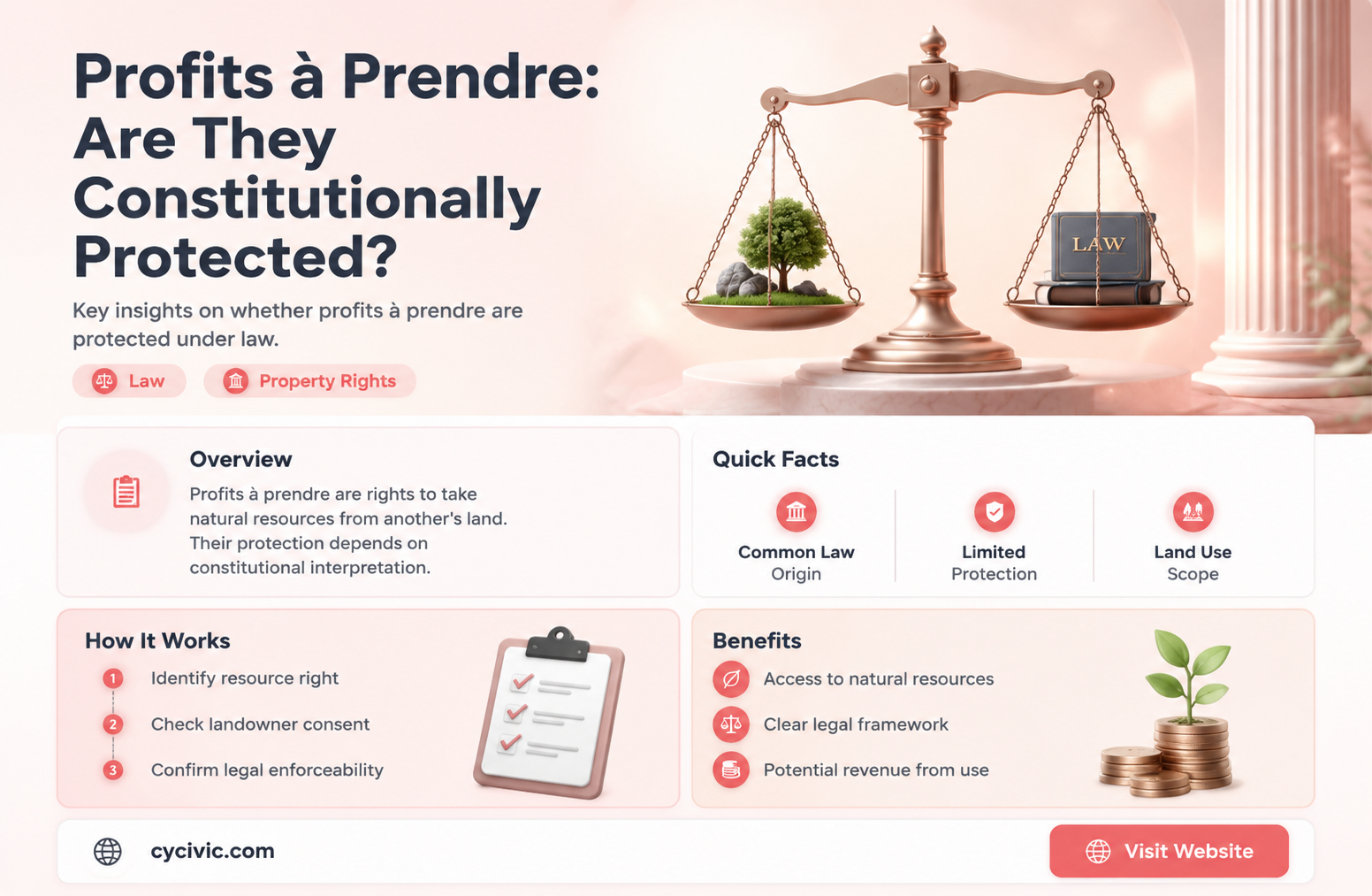

Profits à prendre are rights to take something from another's land, such as minerals or crops. They can be created by express grant, statute, or prescription at common law. In this article, we will explore whether these profits are protected under the constitution.

| Characteristics | Values |

|---|---|

| Registration | Profits a prendre in gross cannot be registered under the Land Registration Act 2002, but may be the subject of notice in the register of the affected land |

| Creation | Profits a prendre in gross may be created by express grant, statute, or prescription at common law or under the doctrine of lost modern grant |

| Rights of common | Rights of common capable of registration under the Commons Registration Act 1965 cannot be registered under the Land Registration Act 2002 |

| Right to graze | At common law, the courts do not recognise a right in common for members of the public generally, or for a significant class of the public |

| Extent of rights | The exercise of the rights cannot be so extensive that they displace the rights of the landowner |

| Commercial purposes | An appurtenant right cannot exist for commercial purposes |

| Rights of support | The holder of the right must not disregard the rights of support of land for adjoining owners |

| Mines and minerals | Mines of gold and silver belong to the State. By statute, the exclusive right to work minerals is vested in the State |

Explore related products

What You'll Learn

- Profits a prendre in gross may be the subject of notice in the register of the affected land

- Profits a prendre in gross may be created by express grant, statute or prescription

- Profits a prendre in gross are not recognised as a right in common for members of the public

- Profits a prendre in gross cannot be acquired under the provisions of the Prescription Act 1832

- Profits a prendre in gross may be granted over the same land to take different things

![]()

Profits a prendre in gross may be the subject of notice in the register of the affected land

Profits à prendre in gross are rights not attached to the ownership of any particular piece of land. The owner of the profit may not own any land at all and may dispose of the profit independently from any land they do own.

A profit à prendre in gross may be substantively registered with its own title. However, it may also be the subject of notice in the register of the affected land, without being registered with its own title. If the affected land is not registered, it may be the subject of a caution against first registration.

If the profit à prendre in gross is for a term of seven years or less, it cannot be registered with its own title. To meet the registration requirements, the 'noting a profit' transaction must be included in the application, along with form AN1 or form AP1. A notice will then be entered in the charges register of the title to the affected land.

A profit à prendre appurtenant, on the other hand, is a right of benefit attached to a particular piece of land and cannot be registered with its own title.

The First Amendment and Neo-Nazis: Protected or Prohibited?

You may want to see also

Explore related products

$42.39 $52.99

![]()

Profits a prendre in gross may be created by express grant, statute or prescription

Profits à prendre in gross may be created by express grant, statute or prescription. In English law, there are five ways to create a profit à prendre: express grant, reservation, implied grant, prescription and by statute. The owner of an estate in land may expressly grant a profit à prendre over their estate. Where the owner of an estate in land sells part of their estate, but retains the other part, a profit-à-prendre may be created by reservation. This is actually a re-grant made by the purchaser of the newly created estate in land from which the owner of the original estate in land may benefit.

A profit à prendre in gross may be created by express grant (or reservation), by statute, or by prescription at common law or under the doctrine of lost modern grant. It cannot be acquired under the provisions of the Prescription Act 1832 (section 5 of which requires the right to have been enjoyed for the benefit of the claimant’s land).

Some profits à prendre in gross are 'rights of common' for the purposes of the Commons Registration Act 1965 (and the Commons Act 2006, which when fully in force will repeal the Commons Registration Act 1965). Rights of common capable of registration under the Commons Registration Act 1965 cannot be registered under the Land Registration Act 2002 (section 1(1) of the Commons Registration Act 1965). Nor can the burden of such rights be noted in the register of the land affected (section 33(d) of the Land Registration Act 2002). It is therefore necessary to establish whether a profit à prendre in gross is a right of common capable of registration under the Commons Registration Act 1965. Such a right may be created today (by express grant, statute or prescription) although most are of older origin.

The Heroes Protecting America's Natural Resources

You may want to see also

Explore related products

![]()

Profits a prendre in gross are not recognised as a right in common for members of the public

Profits a prendre in gross are rights of common for the purposes of the Commons Registration Act 1965 and the Commons Act 2006. However, these rights cannot be registered under the Land Registration Act 2002. Instead, a profit a prendre in gross may be the subject of notice in the register of the affected land, without being registered with its own title.

Profits a prendre in gross may be created by express grant (or reservation), by statute, or by prescription at common law or under the doctrine of lost modern grant. They cannot be acquired under the provisions of the Prescription Act 1832, as this requires the right to have been enjoyed for the benefit of the claimant's land.

It is important to note that the exercise of the rights of profits a prendre cannot be so extensive that they displace the rights of the landowner. An appurtenant right cannot exist for commercial purposes, and the holder of the right must respect the rights of support of land for adjoining owners.

News Propaganda: Free Speech or Constitution Conundrum?

You may want to see also

Explore related products

![]()

Profits a prendre in gross cannot be acquired under the provisions of the Prescription Act 1832

Profits à prendre in gross cannot be acquired under the provisions of the Prescription Act 1832. This is because section 5 of the Act requires the right to have been enjoyed for the benefit of the claimant's land.

Profits à prendre are rights to take something from another's land. They are a type of easement, which is a right that benefits another piece of land. The exercise of the rights cannot be so extensive that they displace the rights of the landowner. Profits à prendre in gross may be created by express grant (or reservation), by statute, or by prescription at common law or under the doctrine of lost modern grant.

The Prescription Act 1832 has been repealed and replaced by the 2009 Act. Any application lodged after 30 November 2021 cannot be grounded upon the Prescription Act 1832, as user will not be in the period immediately before making the application.

Some profits à prendre in gross are 'rights of common' for the purposes of the Commons Registration Act 1965 (and the Commons Act 2006, which when fully in force will repeal the Commons Registration Act 1965). Rights of common capable of registration under the Commons Registration Act 1965 cannot be registered under the Land Registration Act 2002.

Patent Rights: Constitutional Protection or Legislative Loophole?

You may want to see also

Explore related products

![]()

Profits a prendre in gross may be granted over the same land to take different things

Profits à prendre are not mentioned in the UK constitution. However, they are mentioned in the Commons Registration Act 1965 and the Commons Act 2006, which will repeal the Commons Registration Act 1965 when it comes into force.

Profits à prendre in gross may be granted over the same land to take different things, or to take the same thing at different times. This means that there may be more than one profit à prendre in gross affecting the same land. For example, a profit à prendre in gross may be created by express grant, statute, or prescription at common law.

Profits à prendre in gross are not always registered at the Land Registry and may not be visible on a site inspection if they are not being used on the day of the inspection. They can be difficult to identify, so it is important to establish whether a profit à prendre in gross is a right of common capable of registration under the Commons Registration Act 1965.

Profits à prendre in gross can be created today, although most are of older origin. They cannot be acquired under the provisions of the Prescription Act 1832, as this requires the right to have been enjoyed for the benefit of the claimant's land.

Felons' Voting Rights: Constitutional Protection or State Decision?

You may want to see also

Frequently asked questions

A profit a prendre in gross is a right of common capable of registration under the Commons Registration Act 1965. It may be created by express grant, statute or prescription.

A right to graze is an example of a profit a prendre in gross.

Yes, the exercise of the rights cannot be so extensive that they displace the rights of the landowner.

No, an appurtenant right cannot exist for commercial purposes.