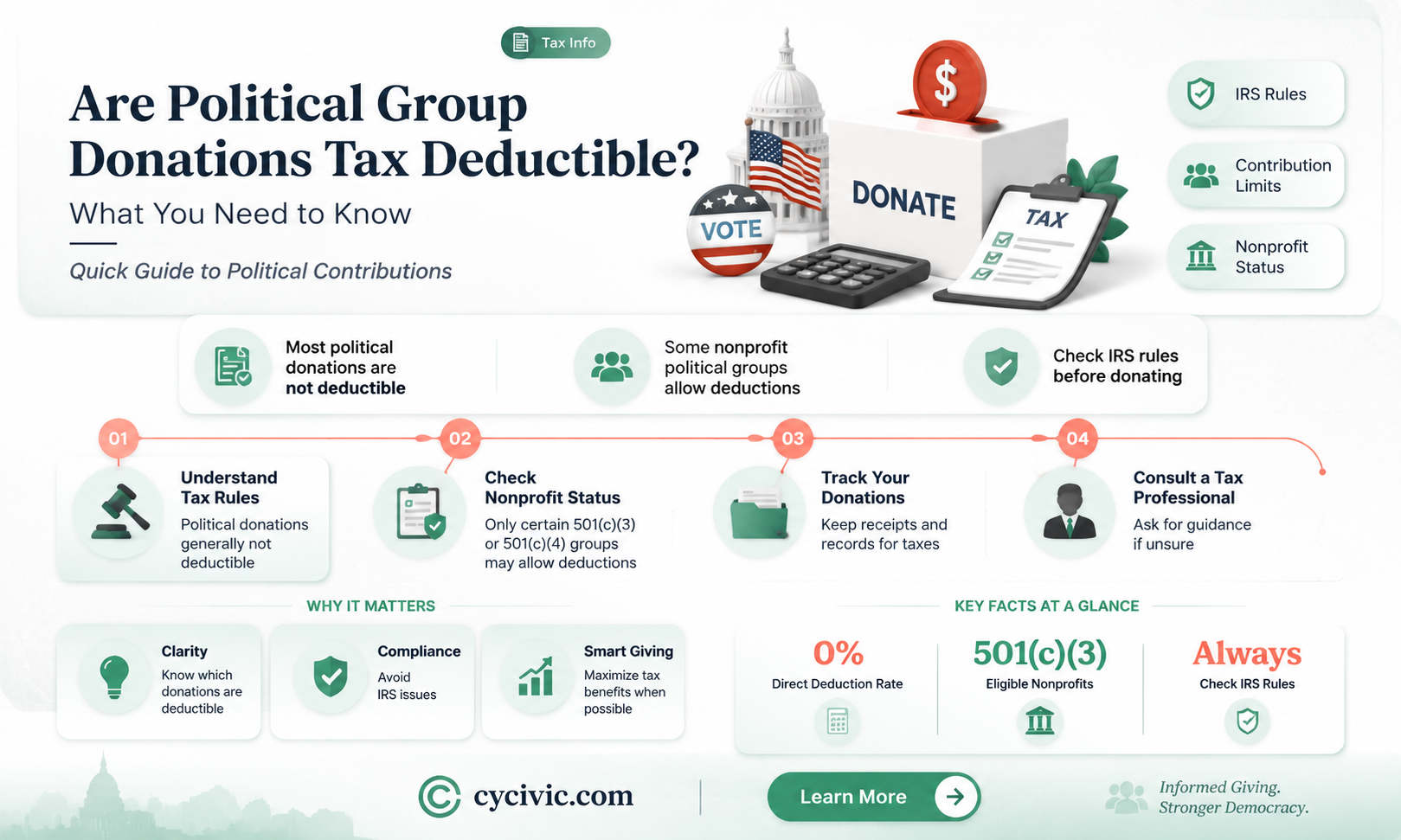

The question of whether political groups are tax-deductible is a complex and often debated issue, as it intersects with tax laws, political regulations, and the principles of free speech and civic engagement. In many countries, including the United States, donations to certain political organizations, such as political parties or candidate campaigns, are generally not tax-deductible because they are considered personal expenses rather than charitable contributions. However, donations to some non-partisan political advocacy groups, educational organizations, or think tanks may qualify for tax deductions if they meet specific criteria, such as being classified as 501(c)(3) organizations under U.S. tax law. Understanding these distinctions is crucial for donors who wish to support political causes while maximizing their tax benefits, as well as for policymakers seeking to balance transparency, fairness, and the role of money in politics.

| Characteristics | Values |

|---|---|

| Tax Deductibility for Political Groups | Generally, donations to political groups are not tax-deductible in most countries, including the U.S. and Canada. |

| U.S. Specifics (IRS Rules) | Donations to political parties, candidates, or PACs are not deductible. Only donations to certain 501(c)(3) organizations (e.g., non-partisan voter education groups) may qualify. |

| 501(c)(4) Organizations | These are social welfare organizations that can engage in political activity, but donations to them are not tax-deductible. |

| 501(c)(3) Organizations | Donations to these organizations (e.g., charities, educational groups) are tax-deductible, but they face strict limits on political activity. |

| Canada (CRA Rules) | Political contributions to registered parties or candidates are not deductible. Only donations to registered charities may qualify. |

| UK (HMRC Rules) | Donations to political parties are not tax-deductible. Gift Aid can only be claimed for charitable donations. |

| Exceptions | Some countries allow deductions for donations to specific political education programs or non-partisan activities, but these are rare. |

| Lobbying vs. Political Activity | Lobbying expenses may be partially deductible in some cases, but direct political campaign expenses are not deductible. |

| Transparency Requirements | Political groups often face stricter reporting requirements for donations, even if they are not tax-deductible. |

| Global Trend | Most countries separate charitable and political donations, with political donations excluded from tax benefits. |

Explore related products

$13.9 $25

$14.87 $15.95

What You'll Learn

- Eligibility Criteria: Rules defining which political groups qualify for tax-deductible status under current laws

- IRS Regulations: Specific IRS guidelines governing tax deductions for contributions to political organizations

- (c)(4) Status: Tax-exempt status for social welfare groups, including certain political activities

- Donation Limits: Maximum deductible amounts for contributions to political groups or related entities

- Prohibited Activities: Actions that disqualify political groups from being eligible for tax deductions

![]()

Eligibility Criteria: Rules defining which political groups qualify for tax-deductible status under current laws

In the United States, not all political groups are created equal in the eyes of the IRS when it comes to tax-deductible status. The eligibility criteria are stringent, designed to differentiate between organizations that serve the public good and those that primarily advance private interests. To qualify, a political group must first be structured as a 501(c)(3) organization, which is reserved for charitable, religious, educational, or scientific entities. This classification explicitly prohibits substantial lobbying or political campaign intervention, meaning groups cannot endorse candidates or engage in partisan activities. For instance, a non-profit focused on voter education might qualify, while a political action committee (PAC) would not.

The IRS scrutinizes the purpose and activities of political groups to ensure alignment with tax-exempt goals. Organizations must demonstrate that their primary mission is charitable, such as promoting social welfare or educating the public on policy issues, rather than advocating for specific political outcomes. For example, a group that provides non-partisan research on climate change policies could qualify, whereas one lobbying for a particular candidate’s environmental plan would not. The key distinction lies in whether the group’s activities benefit the broader public or serve narrow, partisan interests.

Another critical factor is the source and use of funds. Tax-deductible donations to eligible political groups must be used exclusively for charitable purposes, not for political campaigns or lobbying efforts. Donors should ensure the organization provides clear documentation of its tax-exempt status, typically an IRS determination letter. For instance, contributions to a 501(c)(3) focused on civic engagement are deductible, but donations to a 501(c)(4) social welfare organization, which can engage in political activities, are not. Understanding these nuances is essential for both organizations and donors to remain compliant.

Practical tips for political groups seeking tax-deductible status include maintaining detailed records of activities and expenditures, avoiding partisan language in communications, and consulting legal or tax professionals to navigate IRS regulations. For donors, verifying an organization’s 501(c)(3) status through the IRS’s Tax Exempt Organization Search tool is a crucial step before claiming a deduction. While the rules may seem complex, they serve to uphold the integrity of tax-exempt status and ensure that deductible contributions genuinely support public welfare rather than political agendas.

Are All Political PACs 527 Organizations? Unraveling the Truth

You may want to see also

Explore related products

![]()

IRS Regulations: Specific IRS guidelines governing tax deductions for contributions to political organizations

Contributions to political organizations often spark confusion among taxpayers regarding their tax-deductible status. The Internal Revenue Service (IRS) provides clear guidelines to navigate this complexity. Under current regulations, donations to political parties, campaigns, or candidates are not tax- deductible. This rule applies regardless of whether the contribution is made to a local, state, or federal political entity. The rationale is straightforward: political contributions are considered personal expenses rather than charitable donations, which are the primary focus of tax deductions.

However, not all politically affiliated activities are excluded from tax benefits. Certain organizations, such as 501(c)(3) charities, may engage in limited political activity while retaining their tax-exempt status. For instance, a charity can advocate for policy changes or lobby for legislation, provided these activities do not constitute a substantial part of their operations. Taxpayers can deduct donations to such organizations, but only if the contribution is used for charitable purposes, not political campaigns. This distinction is critical for donors seeking to maximize their tax benefits while supporting causes aligned with their values.

The IRS also outlines specific rules for political action committees (PACs) and 527 organizations. Contributions to these groups are generally not deductible, as they are primarily focused on influencing elections or advocating for specific candidates. However, some 527 organizations may qualify as tax-exempt under other sections of the tax code, such as 501(c)(4) social welfare organizations. Donors must carefully review the organization’s tax status before assuming any deduction eligibility. Missteps in this area can lead to audits or penalties, underscoring the importance of due diligence.

Practical tips for taxpayers include maintaining detailed records of contributions and verifying an organization’s tax-exempt status using the IRS Tax Exempt Organization Search tool. For those seeking to support political causes while optimizing tax benefits, consider redirecting funds to charitable arms of advocacy groups, which often operate as separate 501(c)(3) entities. For example, donating to the educational foundation of a political organization may qualify for a deduction, whereas a direct contribution to its PAC would not. This strategic approach allows donors to align their financial support with their beliefs while adhering to IRS regulations.

In summary, while political contributions themselves are not tax-deductible, understanding the nuances of IRS guidelines can unlock opportunities for savvy donors. By distinguishing between political and charitable activities and leveraging tools like the IRS database, taxpayers can navigate this complex landscape with confidence. Always consult a tax professional for personalized advice, especially when dealing with organizations that straddle the line between political and charitable work.

Mastering Polite Disagreement: Effective Phrases for Respectful Arguments

You may want to see also

Explore related products

![]()

501(c)(4) Status: Tax-exempt status for social welfare groups, including certain political activities

In the United States, organizations seeking tax exemption for political activities often turn to 501(c)(4) status, a designation that allows social welfare groups to engage in limited political campaigning while maintaining their tax-exempt standing. This status is distinct from 501(c)(3) organizations, which are strictly prohibited from substantial political involvement. To qualify for 501(c)(4) status, an organization must primarily operate to promote social welfare, a broad category that includes activities benefiting the community at large. Political activities, such as lobbying or supporting candidates, are permitted but must not become the organization’s primary function. For instance, a group advocating for environmental policies can endorse candidates who align with their mission, provided their main focus remains on community-wide initiatives like clean water campaigns or public education programs.

One of the key advantages of 501(c)(4) status is the ability to shield donor identities, a feature that has sparked both interest and controversy. Unlike 501(c)(3) organizations, which must disclose significant donors to the IRS, 501(c)(4)s are not required to reveal their contributors publicly. This anonymity has made 501(c)(4)s a popular vehicle for political spending, particularly among groups seeking to influence elections without exposing their financial backers. However, this lack of transparency has also raised concerns about the potential for undisclosed "dark money" to distort political processes. For organizations considering this route, it’s crucial to balance the benefits of donor privacy with the ethical implications of undisclosed funding.

Navigating the rules for 501(c)(4) organizations requires careful attention to the IRS’s guidelines on political activity. While these groups can engage in lobbying and campaign-related efforts, they must ensure that such activities do not eclipse their social welfare mission. A practical tip for compliance is to maintain detailed records of expenditures, clearly distinguishing between social welfare programs and political initiatives. For example, if an organization spends 40% of its budget on a voter education campaign and 60% on community health programs, it can demonstrate that its primary focus remains on social welfare. Regular audits and legal consultations can further safeguard against inadvertently crossing IRS thresholds.

Despite its flexibility, 501(c)(4) status is not a free pass for unfettered political engagement. The IRS scrutinizes these organizations to ensure they meet the "primarily operated" test for social welfare. Groups that fail this test risk losing their tax-exempt status and facing penalties. A notable example is the 2013 IRS controversy, where some organizations were accused of misusing 501(c)(4) status for predominantly political purposes. To avoid such pitfalls, organizations should adopt a proactive approach, such as creating a clear mission statement, establishing a board of directors to oversee activities, and regularly reviewing their operations to ensure alignment with IRS requirements.

In conclusion, 501(c)(4) status offers a unique opportunity for social welfare groups to engage in political activities while enjoying tax exemption. However, this privilege comes with stringent conditions and ethical considerations. By prioritizing transparency, maintaining a clear focus on social welfare, and adhering to IRS guidelines, organizations can effectively leverage this status to advance their missions without compromising their standing. For those navigating this complex landscape, the key lies in striking a balance between political engagement and community benefit, ensuring that their work remains both impactful and compliant.

Mastering Citations: A Guide to Citing Political Speeches Effectively

You may want to see also

Explore related products

![The Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS Penalties](https://m.media-amazon.com/images/I/617DYgupSxL._AC_UL320_.jpg)

![]()

Donation Limits: Maximum deductible amounts for contributions to political groups or related entities

In the United States, donations to political groups, such as political parties, candidates, or Political Action Committees (PACs), are generally not tax-deductible. The Internal Revenue Service (IRS) classifies these contributions as gifts for political purposes, which do not qualify for charitable deductions. However, the rules shift when considering donations to certain related entities, like 501(c)(3) organizations engaged in non-partisan activities or educational initiatives. Understanding the donation limits and deductible amounts for these related entities is crucial for maximizing tax benefits while staying compliant.

For 501(c)(3) organizations, which are tax-exempt and eligible to receive tax-deductible donations, the IRS imposes no specific dollar limit on deductible contributions. Instead, individuals can deduct up to 60% of their adjusted gross income (AGI) for cash donations, with any excess carried over for up to five subsequent years. For corporations, the limit is 10% of taxable income. However, these rules apply only if the organization does not engage in substantial lobbying or political campaign activities. For example, donating $10,000 to a non-partisan voter education group with 501(c)(3) status could be fully deductible if it falls within the AGI percentage limits.

When navigating donations to political groups or their affiliates, it’s essential to distinguish between deductible and non-deductible contributions. For instance, donating to a 501(c)(4) social welfare organization, which can engage in political activities, is generally not tax-deductible. Similarly, contributions to Super PACs or directly to candidates are non-deductible. A practical tip is to verify an organization’s tax status using the IRS Tax Exempt Organization Search tool before donating. This ensures clarity on whether your contribution qualifies for a deduction.

One common misconception is that all politically related donations are non-deductible. While this is true for direct political contributions, certain exceptions exist. For example, donations to 501(c)(3) organizations that focus on policy research or public education may be deductible, even if their work indirectly influences political discourse. However, donors must ensure the organization’s primary activities align with IRS guidelines for charitable purposes. For instance, a think tank analyzing healthcare policy could qualify, whereas a group explicitly advocating for a candidate would not.

In conclusion, while direct donations to political groups are not tax-deductible, contributions to related entities like 501(c)(3) organizations may offer deductible benefits within specific limits. Understanding these distinctions and adhering to IRS guidelines can help donors optimize their tax strategy while supporting causes aligned with their values. Always consult a tax professional to ensure compliance and maximize deductions.

Understanding NYC Politics: A Comprehensive Guide to the City's Political Landscape

You may want to see also

Explore related products

![]()

Prohibited Activities: Actions that disqualify political groups from being eligible for tax deductions

Political groups seeking tax-deductible status must navigate a minefield of prohibited activities that can jeopardize their eligibility. The IRS strictly enforces rules to maintain the separation between charitable and political endeavors. Engaging in lobbying, campaign intervention, or partisan activities beyond permitted limits automatically disqualifies an organization from tax-exempt status under Section 501(c)(3). Even seemingly minor infractions, like endorsing a candidate or using organizational resources for political ads, can trigger audits, fines, or revocation of tax benefits. Understanding these boundaries is critical for compliance.

Consider the case of lobbying, a common pitfall. While 501(c)(3) organizations can engage in some lobbying, it must not constitute a "substantial part" of their activities. The IRS uses a facts-and-circumstances test to determine if lobbying efforts are excessive. For instance, spending over 20% of annual expenditures on lobbying often raises red flags. Practical tips include tracking lobbying expenses meticulously, avoiding direct calls to action in communications, and consulting legal counsel when in doubt. Nonprofits must prioritize their charitable mission over political advocacy to remain within IRS guidelines.

Another disqualifying activity is campaign intervention, which includes endorsing or opposing candidates, donating to political campaigns, or engaging in voter education that favors one party. For example, distributing voter guides that implicitly support a candidate or using organizational social media accounts to promote political events can violate IRS rules. To avoid this, nonprofits should adopt clear policies separating their activities from political campaigns, train staff and volunteers on compliance, and refrain from coordinating with political groups. Transparency and strict adherence to nonpartisanship are essential.

Comparatively, 501(c)(4) social welfare organizations enjoy more flexibility in political activities but are not eligible for tax-deductible donations. This distinction highlights the trade-off between political engagement and tax benefits. Groups must decide whether their primary goal is to influence policy through advocacy or to rely on tax-deductible donations for charitable work. For those choosing 501(c)(3) status, the takeaway is clear: political activities must remain secondary and within strict limits to preserve tax-exempt eligibility.

In conclusion, prohibited activities for tax-deductible political groups are not merely technicalities but fundamental boundaries that define their purpose and operations. By avoiding lobbying excesses, campaign intervention, and partisan actions, organizations can maintain compliance while pursuing their missions. Regular audits, clear policies, and ongoing education are practical steps to ensure adherence. The IRS’s rules are designed to protect the integrity of charitable work, and organizations that respect these limits can thrive without risking their tax-exempt status.

Corsica's Political Engagement: Activism, Autonomy, and National Identity Explored

You may want to see also

Frequently asked questions

Generally, donations to political groups, such as political parties, candidates, or PACs (Political Action Committees), are not tax-deductible. These contributions are considered personal expenses and do not qualify for deductions on federal tax returns.

Donations to 501(c)(3) nonprofit organizations are tax-deductible, but only if the organization’s primary purpose is charitable, educational, or religious, and not political. If a nonprofit engages in substantial political campaigning, donations may not be deductible.

No, donations to 501(c)(4) organizations, which can engage in political activities, are not tax-deductible. These groups are classified as social welfare organizations and do not qualify for charitable deductions.