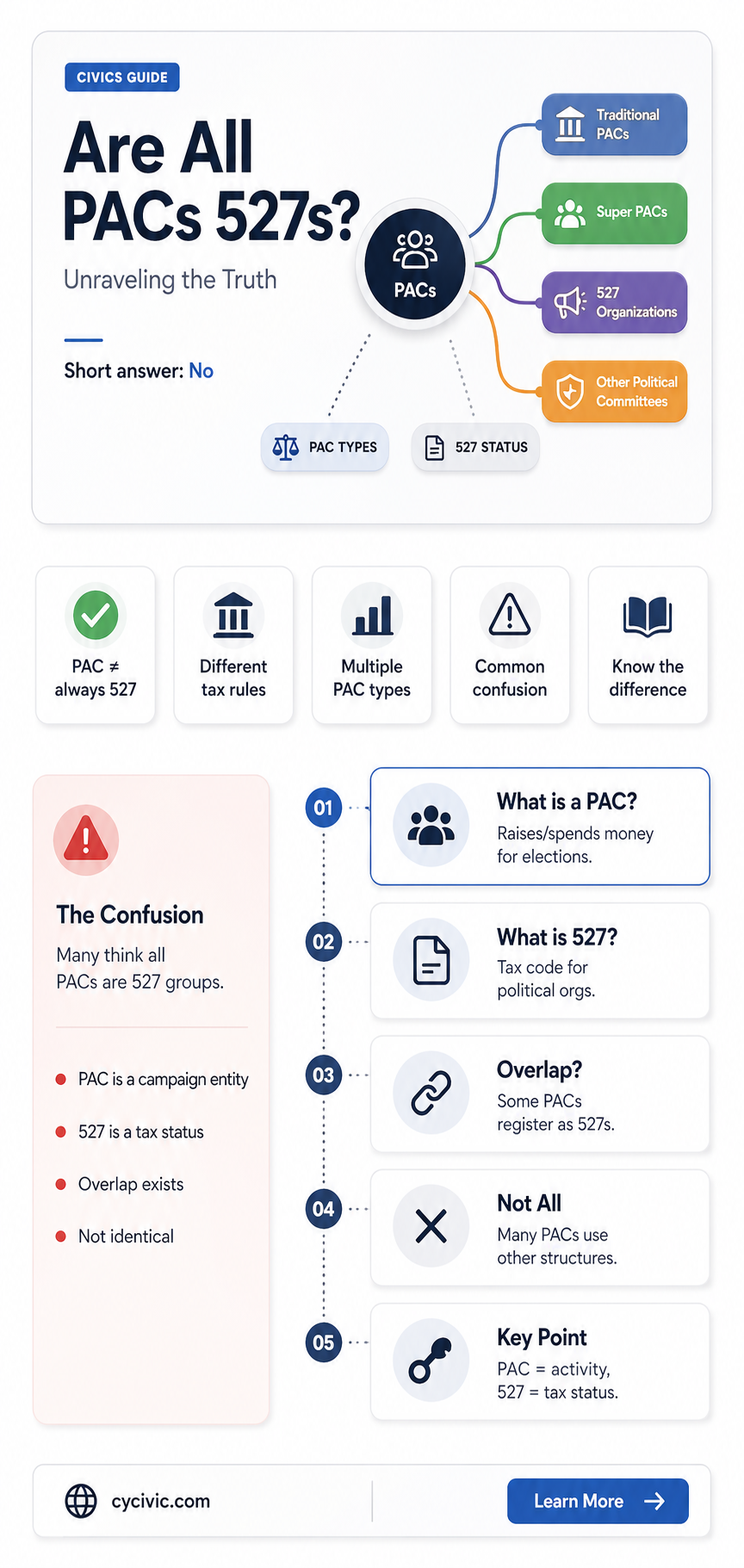

Political Action Committees (PACs) and 527 organizations are often conflated, but they are distinct entities with different regulatory frameworks and purposes. While both can influence elections, PACs are primarily regulated by the Federal Election Commission (FEC) and are limited in their contributions to candidates and parties, whereas 527s, named after the section of the tax code that governs them, are typically tax-exempt organizations that focus on voter education, issue advocacy, or fundraising, with fewer restrictions on spending. Not all political PACs are 527s, as PACs operate under stricter contribution limits and reporting requirements, while 527s have broader flexibility in their activities but cannot directly advocate for the election or defeat of a candidate. Understanding these differences is crucial for navigating the complex landscape of political financing and compliance.

| Characteristics | Values |

|---|---|

| Definition | Not all political PACs are 527 organizations. A 527 is a tax-exempt group primarily formed to influence the selection, nomination, election, appointment, or defeat of candidates to federal, state, or local public office. PACs (Political Action Committees) are committees that pool campaign contributions from members and donate those funds to campaign for or against candidates, ballot measures, or legislation. |

| Tax Status | 527s are tax-exempt under Section 527 of the Internal Revenue Code but must pay income tax on certain political activities. PACs registered with the FEC are not tax-exempt and must comply with different reporting requirements. |

| Regulation | 527s are regulated by the IRS and must file periodic reports on their finances. PACs are regulated by the Federal Election Commission (FEC) and are subject to contribution limits and disclosure rules. |

| Contribution Limits | 527s can accept unlimited contributions from individuals, corporations, and unions. PACs have strict contribution limits imposed by the FEC. |

| Spending Focus | 527s often focus on issue advocacy and voter mobilization, though they can engage in express advocacy. PACs primarily focus on directly supporting or opposing candidates. |

| Disclosure Requirements | 527s must disclose donors and expenditures to the IRS, but the frequency and detail vary. PACs must disclose donors, expenditures, and independent expenditures to the FEC on a regular basis. |

| Coordination with Campaigns | 527s can coordinate with campaigns on issue advocacy but not on express advocacy. PACs cannot coordinate with campaigns on any election-related activities. |

| Examples | Examples of 527s include the Swift Boat Veterans for Truth and the Progressive Change Campaign Committee. Examples of PACs include ActBlue and the National Rifle Association Political Victory Fund. |

| Reporting Frequency | 527s file periodic reports with the IRS, typically monthly or quarterly. PACs file regular reports with the FEC, often monthly or quarterly, depending on election cycles. |

| Purpose | 527s are often used for issue advocacy, voter registration, and mobilization. PACs are primarily used to raise and spend money to directly influence elections. |

Explore related products

What You'll Learn

![]()

Definition of 527 Organizations

527 organizations, named after the section of the U.S. tax code that governs them, are tax-exempt groups organized to influence elections or advocate for political causes. Unlike traditional Political Action Committees (PACs), which primarily raise money to directly support candidates, 527s operate with more flexibility in their activities. They can engage in issue advocacy, voter mobilization, and even direct campaign advertising, as long as their efforts do not explicitly coordinate with candidates or political parties. This distinction is crucial: while all 527s are political in nature, not all political PACs are 527s, and vice versa.

To understand the scope of 527 organizations, consider their role in modern political campaigns. For instance, a 527 might run ads highlighting a candidate’s stance on healthcare without directly urging voters to support that candidate. This is known as "issue advocacy," a gray area that allows 527s to skirt some of the stricter regulations governing PACs. However, this flexibility comes with reporting requirements. 527s must disclose their donors and expenditures to the IRS, though these rules are less stringent than those for PACs, which report to the Federal Election Commission (FEC).

One practical takeaway for anyone involved in political fundraising or advocacy is to carefully consider the structure of their organization. If the goal is to directly support candidates, a PAC might be the better choice. If the focus is broader issue advocacy or grassroots mobilization, a 527 could offer more operational freedom. For example, a group aiming to raise awareness about climate change policies might opt for 527 status to run educational campaigns without being tied to specific candidates.

A cautionary note: while 527s enjoy greater flexibility, they must navigate the fine line between issue advocacy and express advocacy (directly supporting or opposing a candidate). Crossing this line can trigger additional regulations and scrutiny. For instance, a 527 that runs an ad saying, "Vote for Candidate X because they support clean energy," would likely be classified as express advocacy, subjecting it to PAC-like restrictions.

In conclusion, 527 organizations are a unique tool in the political landscape, offering a middle ground between direct candidate support and issue-based advocacy. By understanding their definition, structure, and limitations, political operatives can strategically leverage 527s to maximize their impact while staying compliant with legal requirements. Whether you’re a campaign manager, donor, or activist, knowing the difference between 527s and PACs is essential for effective political engagement.

Navigating the Path to Australian Politics: A Beginner's Comprehensive Guide

You may want to see also

Explore related products

![]()

Differences Between PACs and 527s

Political Action Committees (PACs) and 527 organizations are both vehicles for political spending, but they operate under distinct rules and serve different purposes. A key difference lies in their regulatory framework: PACs are governed by the Federal Election Commission (FEC) and are primarily designed to contribute directly to candidates, parties, or other PACs. In contrast, 527s are regulated by the IRS and focus on issue advocacy, voter mobilization, or general political activities, but they cannot directly contribute to candidates. This fundamental distinction shapes their funding limits, disclosure requirements, and strategic use in campaigns.

Consider the funding mechanisms. PACs are limited in how much they can accept from individuals, typically capped at $5,000 per person per year for traditional PACs and $10,000 for leadership PACs. They must also disclose donors and expenditures regularly to the FEC. 527s, however, can accept unlimited contributions from individuals, corporations, and unions, though they must report expenditures to the IRS. This flexibility makes 527s attractive for high-dollar donors seeking to influence elections without the constraints of direct candidate contributions. For instance, a 527 might run ads highlighting a candidate’s stance on an issue without explicitly endorsing them, while a PAC would need to adhere to strict contribution limits and disclosure rules.

Strategically, PACs and 527s serve complementary but distinct roles in political campaigns. PACs are ideal for direct financial support to candidates, making them a cornerstone of party and candidate fundraising. 527s, on the other hand, excel in shaping public opinion through issue-based campaigns, often operating in the gray area between advocacy and explicit electioneering. For example, a 527 might focus on voter registration drives or run ads criticizing a policy without mentioning a specific candidate, while a PAC would directly fund a candidate’s campaign materials or events. Understanding these differences allows political operatives to deploy resources more effectively.

Finally, transparency and accountability vary between the two. PACs face stringent disclosure requirements, with detailed reports on contributions and expenditures filed regularly. This transparency helps voters trace the influence of money in politics. 527s, while required to report expenditures, often operate with less scrutiny, particularly if they avoid explicit electioneering. This opacity has led to criticism of 527s as a loophole for "dark money," though their role in issue advocacy remains legally protected. For donors and voters alike, recognizing these differences is crucial for navigating the complex landscape of political spending.

Understanding Mansfield Politics: A Comprehensive Guide for Engaged Citizens

You may want to see also

Explore related products

![]()

Tax Implications for 527 Groups

527 groups, named after the section of the tax code that governs them, are tax-exempt organizations that are often involved in political activities. While they share some similarities with Political Action Committees (PACs), not all PACs are 527s, and understanding their tax implications is crucial for compliance and strategic planning. These organizations must navigate a complex landscape of IRS regulations to maintain their tax-exempt status, which hinges on their primary purpose and activities.

One key tax consideration for 527 groups is the distinction between their political and non-political expenditures. The IRS allows 527s to engage in political activities, but these must not constitute their primary function. For example, a 527 group focused on voter education can retain its tax-exempt status, provided it does not primarily advocate for or against specific candidates. Contributions to 527s are typically not tax-deductible for donors, unlike donations to 501(c)(3) charities, which further differentiates their tax treatment.

Another critical aspect is reporting requirements. 527 groups must file periodic reports with the IRS, detailing their income, expenditures, and activities. Failure to comply can result in penalties, including the loss of tax-exempt status. For instance, a 527 group that fails to disclose large contributions or expenditures in a timely manner may face scrutiny. Practical tip: Use IRS Form 8872 to report political activities and ensure transparency to avoid compliance issues.

Comparatively, while PACs and 527s both engage in political activities, their tax treatments differ significantly. PACs, registered with the Federal Election Commission (FEC), are subject to stricter contribution limits and disclosure rules. In contrast, 527s have more flexibility in fundraising but must carefully manage their activities to avoid being classified as a political organization, which would alter their tax status. This distinction underscores the importance of strategic planning for organizations operating in the political sphere.

Finally, 527 groups should be mindful of state-level tax implications, as some states impose additional regulations or taxes on political organizations. For example, California requires 527s to register with the Secretary of State and file annual reports. To navigate these complexities, organizations should consult tax professionals or legal advisors to ensure full compliance. Takeaway: While 527 groups offer flexibility for political engagement, their tax implications require careful management to avoid pitfalls and maintain their tax-exempt status.

Is Abolition a Political Belief? Exploring Its Ideological Roots and Impact

You may want to see also

Explore related products

![]()

Disclosure Requirements for 527s

527 organizations, named after the section of the tax code that governs them, are tax-exempt groups primarily formed to influence the selection, nomination, election, or appointment of individuals to federal, state, or local public office. Unlike traditional Political Action Committees (PACs), 527s are not subject to the same contribution limits, but they must adhere to specific disclosure requirements to maintain transparency in political spending. These requirements are crucial for ensuring that the public can track the flow of money in politics, even as the landscape of campaign finance continues to evolve.

One of the key disclosure mandates for 527s is the periodic filing of reports with the Internal Revenue Service (IRS). These reports must detail the organization’s contributions and expenditures, including the names and addresses of donors who contribute more than $200 in a calendar year. This threshold is significantly lower than that of some other political entities, such as Super PACs, which only require disclosure for contributions over $200 per election cycle. The frequency of these filings depends on the organization’s activity level, with more active 527s required to file monthly or quarterly reports. For example, a 527 engaged in a high-stakes election might file monthly to keep pace with rapid spending, while a less active group might only file quarterly.

While the IRS oversees the tax status of 527s, the Federal Election Commission (FEC) also plays a role in regulating their activities if they engage in federal electioneering. This dual oversight can create complexities, as 527s must ensure compliance with both agencies’ rules. For instance, if a 527 runs ads explicitly advocating for or against a federal candidate, it must register with the FEC and adhere to additional disclosure requirements, such as reporting independent expenditures within 24 or 48 hours, depending on the timing of the election. This layered regulatory environment underscores the importance of meticulous record-keeping and legal counsel for 527 organizations.

Despite these requirements, critics argue that the disclosure rules for 527s are not stringent enough to prevent "dark money" from influencing elections. Unlike traditional PACs, 527s are not required to disclose the ultimate source of funds if they receive donations from other organizations. This loophole allows donors to remain anonymous, undermining the transparency that disclosure laws aim to achieve. For example, a corporation could donate to a nonprofit, which then donates to a 527, effectively shielding the corporation’s involvement from public scrutiny. This lack of transparency has fueled calls for reform, including proposals to lower disclosure thresholds and require real-time reporting of contributions.

In practice, navigating the disclosure requirements for 527s demands vigilance and a proactive approach. Organizations should establish clear internal protocols for tracking contributions and expenditures, ensuring that all staff and volunteers understand their obligations. Utilizing specialized software to manage financial records can reduce the risk of errors and streamline the filing process. Additionally, 527s should stay informed about changes to campaign finance laws, as regulatory updates can introduce new compliance challenges. By prioritizing transparency and adhering to disclosure requirements, 527s can maintain public trust while effectively pursuing their political objectives.

Is Nozick a Political Liberal? Examining His Libertarian Philosophy

You may want to see also

Explore related products

$15.83

![]()

Role in Political Campaigns

Political Action Committees (PACs) and 527 organizations are distinct entities with unique roles in political campaigns, yet their functions often overlap, leading to confusion. While all 527s are tax-exempt groups under the IRS code, not all PACs are 527s. PACs, primarily regulated by the Federal Election Commission (FEC), are designed to pool campaign contributions and make direct donations to candidates or parties. In contrast, 527s, named after the IRS tax code section, focus on voter mobilization, issue advocacy, and independent expenditures, often operating with fewer restrictions on fundraising but without direct candidate coordination.

In campaigns, PACs serve as financial conduits, bundling contributions from individuals, corporations, or unions to support specific candidates or parties. For instance, a corporate PAC might raise $10,000 from employees and donate $5,000 to a congressional candidate, adhering to FEC limits. This direct financial support is a PAC’s primary role, making it a critical tool for candidates seeking to fund advertising, staff, and events. However, PACs must navigate strict contribution limits—$5,000 per candidate per election—and disclosure requirements, ensuring transparency but limiting their influence compared to 527s.

Meanwhile, 527s excel in shaping public opinion through issue advocacy and independent expenditures. Unlike PACs, they cannot coordinate with candidates but can spend unlimited amounts on ads, rallies, or research to support or oppose a candidate indirectly. For example, a 527 might spend $1 million on a TV campaign highlighting a candidate’s environmental record without directly donating to their campaign. This flexibility allows 527s to amplify messages that PACs, bound by coordination rules, cannot. However, 527s must report donors and expenditures to the IRS, though less frequently than PACs, creating a trade-off between influence and transparency.

The interplay between PACs and 527s in campaigns is strategic. PACs provide direct financial lifelines to candidates, while 527s offer broader, uncoordinated support to sway public sentiment. For instance, a candidate might rely on a PAC for campaign funds while benefiting from a 527’s independent ads targeting undecided voters. This dual approach maximizes both direct and indirect influence, showcasing how these entities complement each other despite their regulatory differences.

In practice, campaigns must carefully navigate the legal boundaries between PACs and 527s to avoid violations. For example, a 527 cannot use a candidate’s campaign materials without triggering coordination rules, while a PAC must ensure donations stay within FEC limits. Understanding these distinctions is crucial for compliance and effectiveness. By leveraging both tools, campaigns can secure financial backing and amplify their message, illustrating the nuanced yet essential roles of PACs and 527s in modern political strategy.

Transamerica Coverage for Political Exiles: What You Need to Know

You may want to see also

Frequently asked questions

No, not all political PACs (Political Action Committees) are 527 organizations. PACs are regulated by the Federal Election Commission (FEC) and primarily focus on contributing to candidates or political parties. 527 organizations, on the other hand, are tax-exempt groups under Section 527 of the Internal Revenue Code, often used for political activities like issue advocacy, but they are not the same as traditional PACs.

The main difference lies in their regulatory framework and purpose. PACs are strictly regulated by the FEC and are designed to raise and spend money to directly support or oppose candidates. 527 organizations are regulated by the IRS and focus on broader political activities, such as issue advocacy, voter mobilization, or independent expenditures, but they cannot directly coordinate with candidates or parties.

While a 527 organization can engage in political activities, it cannot function exactly like a PAC. PACs are specifically authorized to contribute directly to candidates and parties, whereas 527s are generally limited to independent expenditures and issue advocacy. However, some 527s may operate in ways that resemble PACs, but they must adhere to different legal and reporting requirements.