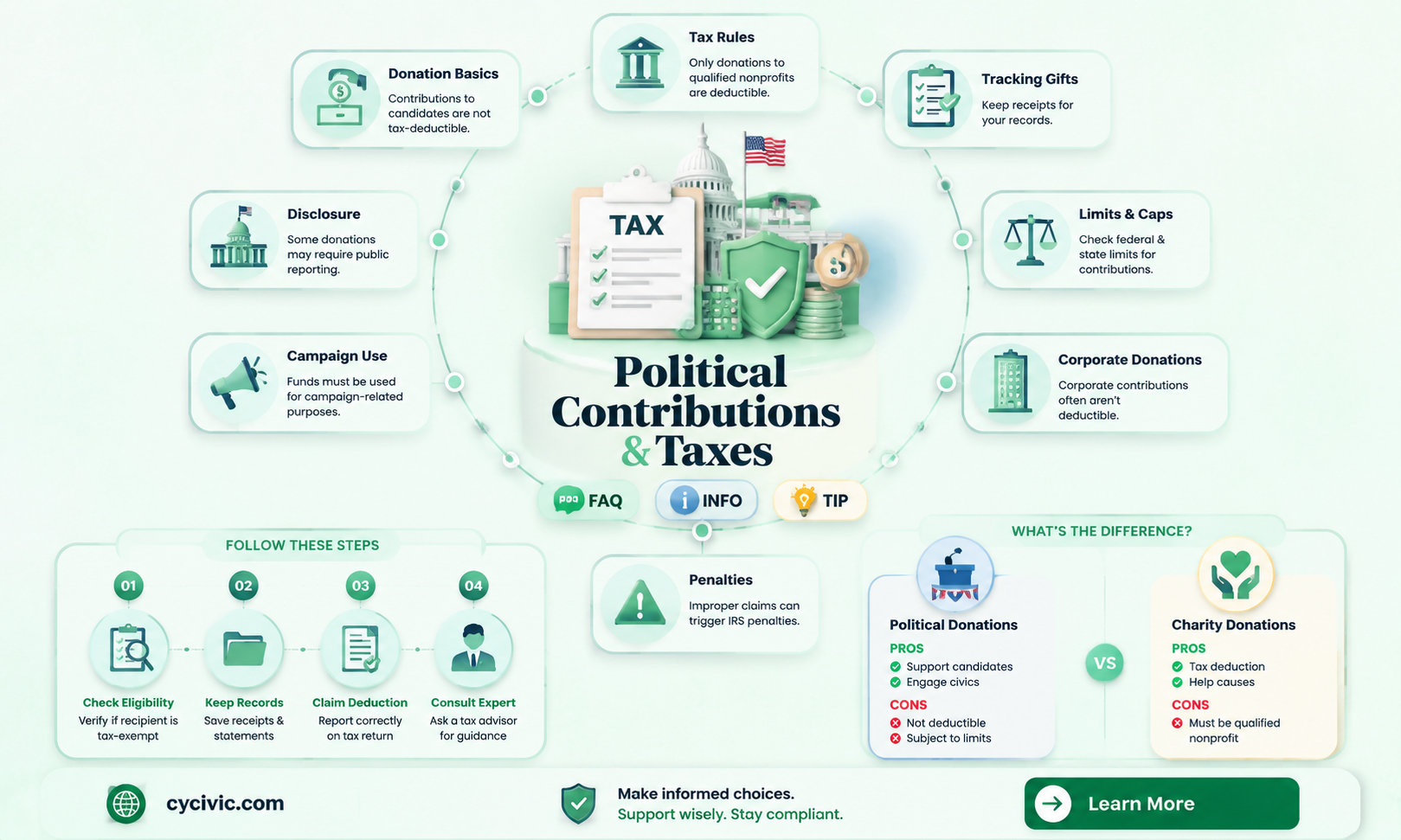

Political contributions are a common way for individuals and organizations to support candidates, parties, or political causes, but they are generally not tax-deductible in the United States. The Internal Revenue Service (IRS) clearly states that donations to political campaigns, parties, or action committees (PACs) cannot be claimed as charitable deductions on federal tax returns. This is because political contributions are considered personal expenses rather than charitable gifts. However, donations to certain tax-exempt organizations, such as 501(c)(4) social welfare groups or 527 political organizations, may offer limited tax benefits, though these are typically unrelated to individual income tax deductions. Understanding these distinctions is crucial for taxpayers to avoid errors or penalties when filing their returns.

| Characteristics | Values |

|---|---|

| Tax Deductibility in the U.S. | Political contributions to candidates, parties, or PACs are not tax-deductible. |

| Tax Deductibility for 501(c)(3) Organizations | Donations to certain non-partisan 501(c)(3) organizations (e.g., voter education groups) may be tax-deductible if they meet IRS criteria. |

| Tax Deductibility for 501(c)(4) Organizations | Donations to 501(c)(4) organizations (e.g., advocacy groups) are not tax-deductible. |

| Tax Deductibility for 527 Organizations | Contributions to 527 political organizations are not tax-deductible. |

| Itemized Deductions | Political contributions cannot be claimed as itemized deductions on federal tax returns. |

| State Tax Laws | Some states may allow deductions for political contributions, but this varies by state. |

| Corporate Contributions | Corporations cannot deduct political contributions as business expenses. |

| IRS Guidelines | The IRS explicitly states that political contributions are not deductible under federal tax law. |

| Alternative Tax Benefits | Some states offer tax credits for political contributions, but this is separate from federal deductions. |

| Recent Changes (as of 2023) | No recent federal changes have made political contributions tax-deductible. |

Explore related products

$13.9 $25

What You'll Learn

- Federal vs. State Rules: Federal law prohibits deductions; some states allow local political donations

- (c)(4) Organizations: Donations to certain nonprofits for political activities may be deductible

- Campaign Donations: Direct contributions to candidates or parties are not tax-deductible

- PAC Contributions: Donations to Political Action Committees (PACs) are generally not deductible

- Charitable vs. Political: Distinguishing between charitable donations (deductible) and political contributions (not deductible)

![]()

Federal vs. State Rules: Federal law prohibits deductions; some states allow local political donations

Federal law draws a clear line in the sand: political contributions are not tax deductible. This prohibition, rooted in the Internal Revenue Code, applies to donations made to candidates, political parties, and Political Action Committees (PACs) at the federal level. The rationale is straightforward—preventing taxpayers from using deductions to indirectly subsidize political campaigns with public funds. This rule ensures that political spending remains a personal choice rather than a taxpayer-supported endeavor.

Contrast this with state-level regulations, where the landscape is far less uniform. Some states, such as Oregon and Virginia, allow taxpayers to deduct contributions made to local political campaigns or state political parties. For instance, Oregon permits a tax credit for contributions to qualified political candidates, effectively reducing the taxpayer’s state tax liability. These state-specific allowances reflect a different policy approach, one that encourages civic engagement by easing the financial burden of political participation.

Navigating these discrepancies requires careful attention to detail. Taxpayers must distinguish between federal and state rules to avoid errors. For example, a donation to a federal candidate is never deductible, but the same contribution to a state-level candidate might be, depending on the state’s laws. This dual-level system underscores the importance of consulting state tax guidelines or a tax professional to maximize potential benefits while staying compliant.

The takeaway is clear: while federal law uniformly prohibits deductions for political contributions, state rules offer a patchwork of opportunities. Taxpayers who engage in local politics may find unexpected advantages in their state’s tax code. However, this benefit is not universal, and eligibility often hinges on specific criteria, such as donation limits or candidate qualifications. Understanding these nuances can transform political contributions from purely altruistic acts into strategically advantageous financial decisions.

Decoding His Behavior: Polite Gestures vs. Genuine Interest Explained

You may want to see also

Explore related products

![]()

501(c)(4) Organizations: Donations to certain nonprofits for political activities may be deductible

Donations to 501(c)(4) organizations present a unique opportunity for taxpayers seeking to support political activities while potentially benefiting from tax deductions. Unlike contributions to political campaigns or parties, which are explicitly non-deductible, donations to certain nonprofits under this tax code section may qualify—but only if the organization’s primary purpose is not political. This distinction is critical, as the IRS scrutinizes the allocation of funds within these organizations to ensure compliance with tax laws. For instance, a 501(c)(4) focused on social welfare might engage in political advocacy as a secondary activity, allowing donors to deduct contributions that support non-political initiatives.

To navigate this landscape, donors must carefully evaluate the organization’s structure and activities. A 501(c)(4) can spend up to 49% of its resources on political campaigns or lobbying without losing its tax-exempt status, but only donations earmarked for non-political programs are deductible. For example, a donation to a 501(c)(4) environmental group might be deductible if it funds educational campaigns or community projects, but not if it directly supports political ads or candidate endorsements. Donors should request detailed documentation from the organization outlining how funds are allocated to ensure compliance.

One practical tip is to consult IRS Publication 526, which clarifies deductible charitable contributions, and Form 1098-C, which organizations may provide to acknowledge donations. Additionally, donors should retain records, such as receipts or acknowledgment letters, to substantiate their deductions in case of an audit. While the rules are complex, strategic giving to 501(c)(4) organizations can align philanthropic goals with tax benefits, provided donors prioritize due diligence.

A comparative analysis highlights the advantage of 501(c)(4) donations over direct political contributions. While the latter offers no tax benefit, supporting a 501(c)(4) allows donors to indirectly influence political discourse while potentially reducing taxable income. However, this approach requires a nuanced understanding of the organization’s activities and a commitment to ensuring funds are directed toward deductible purposes. For high-income earners in higher tax brackets, this strategy can yield significant savings, making it a valuable tool for tax-efficient philanthropy.

In conclusion, donations to 501(c)(4) organizations offer a pathway to deductible political engagement, but only when executed thoughtfully. By focusing on nonprofits whose primary activities are non-political and maintaining meticulous records, donors can maximize their impact while adhering to IRS guidelines. This approach not only supports causes they care about but also optimizes their financial contributions through strategic tax planning.

Do Political Bumper Stickers Influence Votes or Just Spark Debates?

You may want to see also

Explore related products

![]()

Campaign Donations: Direct contributions to candidates or parties are not tax-deductible

In the United States, individuals often wonder how their financial support for political candidates or parties impacts their taxes. A critical point to understand is that direct campaign donations to candidates or political parties are not tax-deductible. This means if you contribute $100 to a congressional candidate or a political party, you cannot claim that amount as a deduction on your federal income tax return. The IRS explicitly classifies these contributions as gifts for political purposes, not charitable donations, which are the only type of gifts eligible for tax deductions.

To illustrate, consider a scenario where a donor gives $5,000 to a presidential campaign. Despite the substantial amount, this donation does not reduce their taxable income. The rationale behind this rule is to prevent taxpayers from using political contributions as a means to lower their tax liability while potentially influencing political outcomes. This distinction is crucial for donors to avoid misunderstandings or errors when filing their taxes.

From a practical standpoint, donors should carefully track their political contributions separately from charitable donations. For instance, if you donate $200 to a local charity and $300 to a state senator’s campaign, only the $200 charitable donation qualifies for a tax deduction. Using accounting tools or spreadsheets to categorize these contributions can help maintain clarity and ensure compliance with tax regulations. Additionally, donors should retain receipts or acknowledgment letters from campaigns, not for tax purposes, but for personal record-keeping and transparency.

A comparative analysis reveals that while political contributions are not tax-deductible, donations to certain political organizations with charitable arms, such as 501(c)(3) nonprofits, may offer tax benefits. For example, contributing to a candidate’s affiliated educational foundation might be deductible if it meets charitable criteria. However, this is a nuanced area, and donors should consult tax professionals to avoid missteps. The key takeaway is that direct campaign donations remain non-deductible, regardless of the candidate or party.

Finally, understanding this rule empowers donors to make informed decisions. While financial support for political causes is a form of civic engagement, it should not be motivated by tax advantages. Donors can instead explore other tax-efficient ways to support causes they care about, such as contributing to charitable organizations aligned with their values. By separating political contributions from tax strategies, individuals can navigate the political landscape responsibly and ethically.

Mastering Political Knowledge: A Self-Teaching Guide for Aspiring Learners

You may want to see also

Explore related products

$19.58 $36.99

![]()

PAC Contributions: Donations to Political Action Committees (PACs) are generally not deductible

Donations to Political Action Committees (PACs) are a common way for individuals and organizations to support political causes, but these contributions come with a critical tax implication: they are generally not deductible. Unlike charitable donations to qualified 501(c)(3) organizations, which can reduce taxable income, PAC contributions fall into a different category under the U.S. tax code. This distinction is rooted in the Internal Revenue Code (IRC), which treats political donations as personal expenditures rather than charitable gifts. As a result, taxpayers cannot claim these contributions as deductions on their federal income tax returns.

Understanding this rule requires a closer look at the purpose of PACs. Political Action Committees are formed to raise and spend money to elect or defeat political candidates. Their activities are regulated by the Federal Election Commission (FEC), and their funds are used for campaign-related expenses, such as advertising, travel, and staff salaries. While these efforts may align with a donor’s political beliefs, the IRS does not consider them charitable in nature. Instead, they are viewed as investments in a political outcome, which does not qualify for tax relief. This classification ensures that taxpayers cannot use deductions to indirectly subsidize political campaigns.

For individuals considering PAC donations, it’s essential to separate the act of giving from its tax consequences. Contributions to PACs can range from small, individual donations to large corporate gifts, but regardless of the amount, the tax treatment remains the same. For example, if someone donates $500 to a PAC, they should not expect to reduce their taxable income by that amount. This rule applies equally to connected PACs (associated with corporations or labor unions) and non-connected PACs (independent groups). Even contributions to Super PACs, which can accept unlimited donations, are not deductible.

One practical tip for donors is to keep detailed records of all political contributions, even though they are not tax-deductible. This documentation can be useful for tracking spending and ensuring compliance with FEC regulations, which limit individual contributions to PACs to $5,000 per year per committee. Additionally, donors should be aware of state-level rules, as some states may offer tax credits or deductions for certain political contributions, though these are rare and vary widely. Always consult a tax professional or refer to state tax guidelines for specific information.

In conclusion, while PAC contributions are a powerful tool for political engagement, they do not provide a tax benefit. Donors should approach these gifts with a clear understanding of their financial implications, focusing on the impact of their support rather than potential deductions. By separating the motivations for giving from tax considerations, individuals can make informed decisions that align with their political values without unexpected financial surprises.

Is Homosexual a Polite Term? Exploring Language and Respect in LGBTQ+ Discourse

You may want to see also

Explore related products

![]()

Charitable vs. Political: Distinguishing between charitable donations (deductible) and political contributions (not deductible)

Taxpayers often confound charitable donations and political contributions, but the IRS draws a clear line between the two. Charitable donations to qualified 501(c)(3) organizations—such as churches, schools, and disaster relief funds—are tax-deductible, provided they meet certain criteria (e.g., itemizing deductions on Schedule A). Political contributions, however, are explicitly non-deductible. This distinction hinges on the purpose of the organization: charitable entities serve public welfare, while political groups aim to influence elections or legislation. Understanding this difference is crucial for accurate tax reporting and avoiding penalties.

Consider a scenario where a taxpayer donates $500 to a local food bank (a 501(c)(3)) and another $500 to a political action committee (PAC). The former is deductible if the taxpayer itemizes, but the latter is not. The IRS scrutinizes such contributions, particularly when taxpayers attempt to mislabel political donations as charitable. For instance, donating to a 501(c)(4) social welfare organization, which can engage in political activity, is not deductible, even if the organization has a charitable-sounding name. Always verify an organization’s tax status using the IRS’s Tax Exempt Organization Search tool before assuming deductibility.

The rationale behind this distinction is rooted in policy. Charitable deductions incentivize support for public good, while disallowing political deductions prevents taxpayers from using write-offs to subsidize partisan activities. This rule applies regardless of contribution size or frequency. For example, a $25 monthly donation to a political candidate’s campaign fund remains non-deductible, whereas a $25 monthly donation to a homeless shelter could reduce taxable income if itemized. Taxpayers should retain receipts and acknowledgment letters for charitable donations, as the IRS may require documentation for amounts over $250.

Practical tip: If you’re unsure whether a contribution qualifies as charitable, ask the organization for their IRS determination letter confirming their 501(c)(3) status. Avoid conflating political activism with philanthropy—donations to advocacy groups, even those aligned with your values, are generally not deductible. For instance, a contribution to a nonprofit fighting climate change may be deductible, but a donation to a PAC supporting environmental candidates is not. Clarity on this distinction ensures compliance and maximizes potential tax benefits.

How Political Machines Shaped Urban Power and Influence Historically

You may want to see also

Frequently asked questions

No, political contributions to candidates, political parties, or political action committees (PACs) are not tax deductible.

Donations to 501(c)(3) organizations are generally tax deductible, but if the organization engages in substantial political campaigning, the contribution may not qualify for a deduction.

No, contributions to 527 organizations, which are political organizations, are not tax deductible.

If the charity or foundation is a qualified 501(c)(3) organization, the donation may be tax deductible, but only if it meets IRS guidelines and is not tied to political campaigning.

No, business expenses related to political contributions are not tax deductible, as they are considered personal expenses under IRS rules.