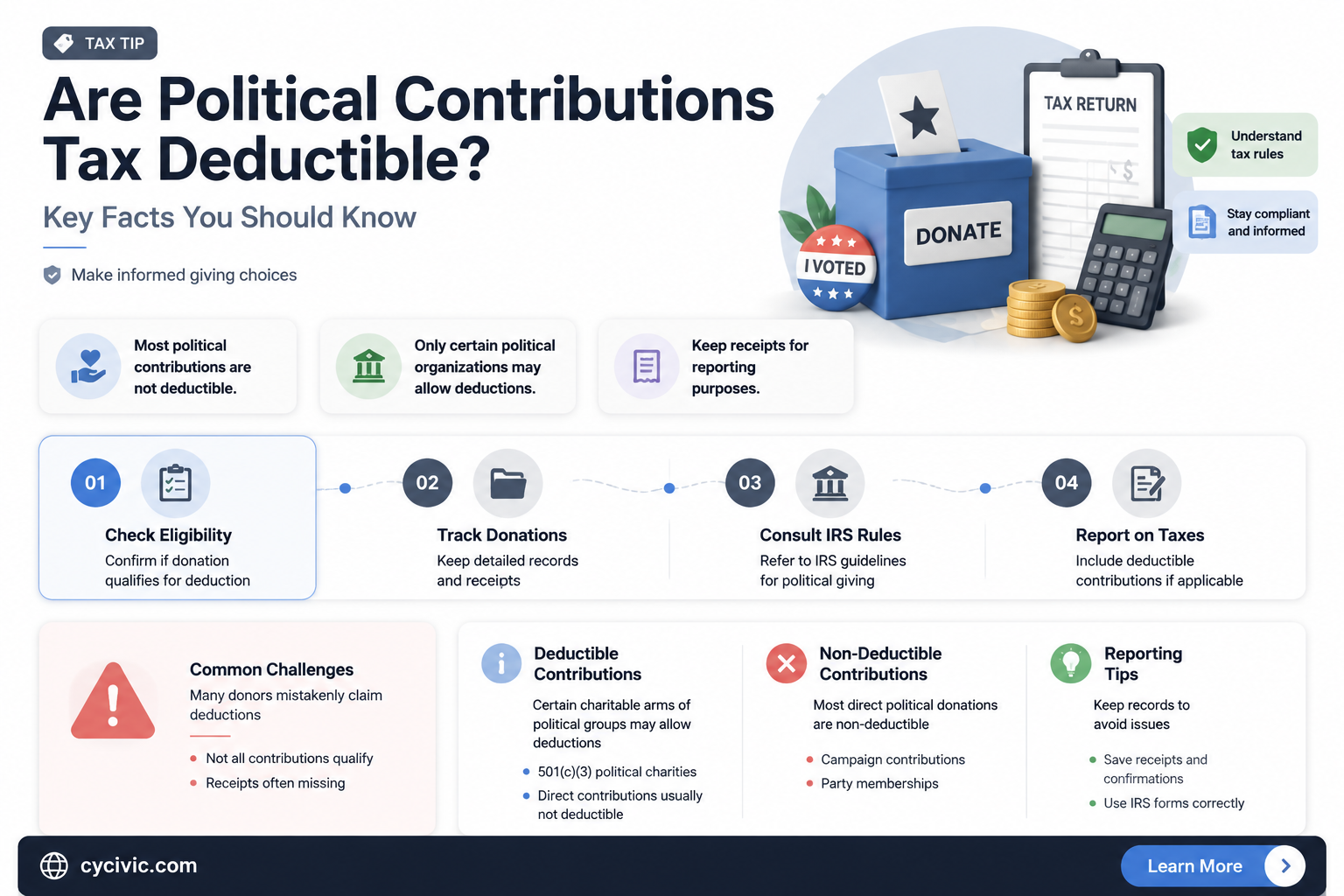

Navigating the complexities of tax deductions, many individuals and businesses wonder whether political contributions qualify as deductible expenses. In the United States, the Internal Revenue Service (IRS) clearly states that donations to political parties, candidates, or campaigns are not tax-deductible. This rule applies to both federal and state taxes, ensuring that political contributions remain separate from charitable giving, which is eligible for deductions. While some contributions to certain political organizations, like 501(c)(4) groups, may offer indirect benefits, they still do not qualify for tax deductions. Understanding this distinction is crucial for taxpayers to avoid errors and potential penalties when filing their returns.

| Characteristics | Values |

|---|---|

| Deductibility Status | Political contributions are not tax-deductible in the United States. |

| IRS Classification | Treated as personal expenses, not charitable contributions. |

| Applicable Tax Law | Internal Revenue Code (IRC) § 162(e) explicitly disallows deductions. |

| State Tax Treatment | Varies by state; some states may allow deductions, but federal rules apply. |

| Corporate Contributions | Corporations cannot deduct political contributions federally. |

| Individual Contributions | Individuals cannot claim deductions on federal tax returns. |

| Alternative Benefits | Contributions may qualify for state tax credits in certain jurisdictions. |

| Reporting Requirements | Contributions over certain limits must be reported to the FEC or state agencies. |

| Recent Changes (as of 2023) | No federal changes to deductibility rules. |

| Common Misconception | Often confused with charitable donations, which are deductible. |

Explore related products

What You'll Learn

![]()

IRS Rules on Deductions

Political contributions, while a cornerstone of civic engagement, do not qualify as deductible expenses under IRS rules. This is a critical distinction for taxpayers who may mistakenly assume that supporting a political cause aligns with charitable deductions. The IRS categorically excludes political donations from the list of eligible write-offs, treating them as personal expenditures rather than charitable acts. This rule applies universally, regardless of the political party, candidate, or campaign committee receiving the funds. Understanding this boundary is essential to avoid errors on tax returns that could trigger audits or penalties.

The rationale behind this rule lies in the IRS’s definition of charitable contributions, which are limited to qualified organizations under section 501(c)(3) of the tax code. Political campaigns and parties do not meet this criteria, as their primary purpose is not charitable but rather to influence elections and policy. Even donations to political action committees (PACs) or 527 organizations, which often engage in issue advocacy, are non-deductible. Taxpayers should carefully review the recipient’s tax status before assuming a contribution is eligible for deduction, as misclassification can lead to complications.

One common misconception is that attending political fundraising events qualifies for partial deduction. While the cost of a ticket or meal may seem like a charitable expense, the IRS disallows any deduction if the primary purpose of the event is political. For example, if a $500 gala ticket includes a $100 meal and $400 donation, the entire $500 is non-deductible. However, if the event is hosted by a 501(c)(3) organization and the political activity is secondary, a portion may be deductible—but this is rare and requires meticulous documentation. Taxpayers should consult IRS Publication 526 for guidance on separating charitable and non-charitable components.

For those seeking to maximize tax benefits while supporting political causes, it’s crucial to differentiate between deductible and non-deductible activities. Contributions to educational foundations or think tanks affiliated with political ideologies may qualify if they hold 501(c)(3) status. For instance, donating to a university’s political science program could be deductible, whereas contributing directly to a candidate’s campaign is not. Taxpayers should verify the recipient’s EIN and tax-exempt status using the IRS’s Tax Exempt Organization Search tool to ensure compliance.

In summary, the IRS rules on deductions are clear: political contributions are not tax-deductible. Taxpayers must navigate this rule carefully, especially when participating in events or organizations with mixed purposes. By understanding the distinctions and verifying the tax status of recipients, individuals can avoid pitfalls and maintain accurate financial records. While political engagement remains a vital aspect of democracy, it does not intersect with tax benefits under current regulations.

Don't Worry Darling: Unraveling the Political Subtext in the Film

You may want to see also

Explore related products

![]()

Eligible Political Contributions

Political contributions can be a powerful way to support causes and candidates you believe in, but not all donations qualify for tax deductions. Understanding which contributions are eligible is crucial for maximizing your financial impact while staying compliant with tax laws. In the United States, for instance, contributions to federal, state, or local candidates, political parties, and political action committees (PACs) are generally not tax-deductible. However, donations to certain political organizations, like 527 groups or 501(c)(4) organizations, may offer limited deductibility under specific circumstances. This distinction highlights the importance of knowing where your money goes and how it’s classified.

To determine eligibility, start by identifying the type of organization you’re contributing to. For example, donations to 501(c)(3) charitable organizations, which may engage in limited political activity, can be deductible if the contribution is used for non-political purposes. Conversely, direct donations to a candidate’s campaign or a party’s general fund are never deductible. A practical tip is to request documentation from the organization confirming how your contribution will be used. This not only helps you understand the impact of your donation but also ensures you have the necessary records for tax purposes.

One common misconception is that all politically motivated donations are non-deductible. While this is largely true for direct campaign contributions, there are exceptions. For instance, contributions to educational or research arms of political organizations, such as think tanks or policy institutes, may qualify for deductions if they meet IRS criteria for charitable giving. However, these cases are rare and require careful scrutiny. Always consult IRS guidelines or a tax professional to avoid errors that could lead to audits or penalties.

Comparing eligible and non-eligible contributions reveals a clear pattern: the deductibility of a donation often hinges on its purpose rather than the recipient’s political affiliation. For example, a donation to a candidate’s campaign is non-deductible, but a contribution to a non-profit organization advocating for policy change might be deductible if it aligns with charitable purposes. This distinction underscores the need to align your giving strategy with your financial goals and tax planning. By focusing on eligible contributions, you can support political causes while potentially reducing your taxable income.

In conclusion, navigating the rules around eligible political contributions requires attention to detail and a clear understanding of tax laws. While most direct political donations are non-deductible, certain contributions to qualifying organizations may offer tax benefits. Always verify the status of the recipient organization, document your donations, and seek professional advice when in doubt. By doing so, you can ensure your political contributions are both impactful and financially prudent.

Are Political Action Committees Taxed? Understanding PAC Taxation Rules

You may want to see also

Explore related products

$13.9 $25

$14.87 $15.95

![]()

Limits and Restrictions

Political contributions, while a fundamental aspect of democratic participation, are subject to strict limits and restrictions to prevent undue influence and maintain fairness. In the United States, the Federal Election Commission (FEC) sets clear boundaries on how much individuals, corporations, and organizations can donate to candidates, parties, and political action committees (PACs). For instance, as of 2023, an individual can contribute up to $3,300 per candidate per election, with a total annual limit of $46,200 to federal candidates. These caps are designed to level the playing field and ensure that no single donor dominates the political landscape.

Beyond federal limits, state-level restrictions add another layer of complexity. Some states, like California, impose lower contribution limits than federal guidelines, while others, such as Florida, align closely with federal rules. Additionally, certain states prohibit contributions from corporations or unions altogether. Donors must navigate this patchwork of regulations carefully to avoid penalties, which can include fines, legal action, or even criminal charges. For example, exceeding contribution limits in New York can result in fines up to three times the excess amount, highlighting the importance of compliance.

One critical restriction often overlooked is the prohibition on foreign nationals contributing to U.S. political campaigns. This ban extends to both direct donations and indirect support, such as funding advertisements or coordinating with campaigns. Even permanent residents (green card holders) are barred from contributing, though U.S. citizens living abroad are exempt. This rule is enforced to safeguard national sovereignty and prevent foreign interference in domestic politics. Violations can lead to severe consequences, including deportation for non-citizens and criminal charges for those involved.

Another key restriction involves the use of corporate and union funds. While corporations and unions can form PACs to pool employee or member contributions, they cannot directly donate to candidates from their general treasuries. This distinction is rooted in the 2010 *Citizens United* Supreme Court decision, which allowed unlimited independent expenditures by corporations and unions but maintained the ban on direct contributions. Donors must ensure their contributions comply with these rules, as misuse of corporate funds can result in both civil and criminal penalties.

Finally, transparency requirements serve as a de facto restriction by mandating disclosure of contributions above certain thresholds. Federal law requires individuals donating over $200 in a year to a single candidate or committee to disclose their name, address, occupation, and employer. This transparency aims to deter quid pro quo arrangements and allow the public to scrutinize political funding. However, loopholes exist, such as donating through multiple LLCs or leveraging "dark money" organizations, which can obscure the true source of funds. Navigating these limits and restrictions requires vigilance, but adherence is essential to uphold the integrity of the political process.

Statistics in Politics: Data-Driven Decisions Shaping Policy and Governance

You may want to see also

Explore related products

![]()

State vs. Federal Laws

Political contributions are subject to a complex interplay of state and federal laws, creating a patchwork of regulations that donors must navigate. At the federal level, the Internal Revenue Service (IRS) clearly states that contributions to political parties, candidates, or campaign committees are not tax-deductible. This rule, rooted in the Internal Revenue Code, ensures that personal political support does not receive a public subsidy through tax benefits. However, federal law does allow deductions for contributions to certain non-political organizations, such as 501(c)(3) charities, which can sometimes blur the line when these groups engage in advocacy work.

In contrast, state laws vary widely and can introduce additional layers of complexity. Some states permit deductions for political contributions, either as a direct state tax deduction or through a tax credit program. For example, Arizona and Oregon offer tax credits for contributions to political parties or candidates, effectively incentivizing political participation at the state level. These programs highlight how state laws can diverge from federal regulations, creating opportunities for donors to offset the cost of their contributions through state tax benefits.

Donors must also be cautious of state-specific restrictions. While federal law caps individual contributions to candidates and political action committees (PACs), states may impose additional limits or reporting requirements. For instance, California requires detailed disclosure of contributions over certain thresholds, while New York restricts corporate political spending. These variations mean that a contribution compliant with federal law could still violate state regulations, underscoring the need for careful research.

Practical tips for navigating this landscape include consulting state tax codes and election laws before making contributions, especially if seeking state-level deductions. Donors should also maintain detailed records of contributions, as state reporting requirements can be more stringent than federal ones. Finally, individuals should avoid assuming that federal rules apply uniformly; instead, they should verify state-specific regulations to ensure compliance and maximize potential tax benefits where available.

In summary, the deductibility of political contributions hinges on a delicate balance between federal prohibitions and state-level allowances. While federal law clearly disallows deductions, state programs can provide avenues for tax relief, though these come with their own rules and limitations. Understanding this state-federal dynamic is essential for donors seeking to support political causes without running afoul of tax laws.

Do Teenagers Engage with Politics? Exploring Youth Interest and Involvement

You may want to see also

Explore related products

![]()

Documentation Requirements

Political contributions, unlike charitable donations, are generally not tax-deductible. However, understanding the documentation requirements for such contributions is crucial for compliance with campaign finance laws and personal record-keeping. Proper documentation ensures transparency and accountability, helping both donors and recipients adhere to legal standards.

For individuals making political contributions, maintaining detailed records is essential. This includes noting the date, amount, and recipient of each contribution. Receipts or acknowledgments from the campaign or political organization should be retained, as they serve as proof of the transaction. While these documents won’t help claim a tax deduction, they are vital for verifying compliance with contribution limits, which vary by jurisdiction and type of campaign. For instance, federal elections in the U.S. have specific caps, and exceeding these limits can result in penalties.

Businesses or organizations contributing to political causes face additional documentation requirements. Corporate contributions often require board approval, and minutes of the meeting where the decision was made should be recorded. In some cases, companies must disclose political spending to shareholders or regulatory bodies, necessitating meticulous documentation. Failure to maintain these records can lead to legal repercussions, including fines or loss of corporate privileges.

A comparative analysis reveals that documentation standards for political contributions are stricter than those for personal expenses. While a casual receipt might suffice for a personal purchase, political contributions demand formal acknowledgments and, in some cases, notarized statements. This heightened scrutiny underscores the importance of accuracy and completeness in record-keeping. For example, contributions to Political Action Committees (PACs) often require detailed reporting, including the donor’s occupation and employer, to comply with Federal Election Commission (FEC) rules.

In conclusion, while political contributions are not tax-deductible, the documentation requirements are stringent and non-negotiable. Donors must prioritize record-keeping to avoid legal pitfalls and ensure transparency. Practical tips include using digital tools to track contributions, setting reminders for reporting deadlines, and consulting legal experts for complex cases. By adhering to these guidelines, individuals and organizations can navigate the political contribution landscape with confidence and integrity.

History's Echoes: Shaping Modern Politics and Global Power Dynamics

You may want to see also

Frequently asked questions

No, political contributions to candidates, political parties, or political action committees (PACs) are not tax-deductible on your federal income tax return.

Donations to 501(c)(3) nonprofit organizations are generally tax-deductible, but if the organization engages in substantial lobbying or political campaign activities, the portion of your donation used for those activities is not deductible.

No, contributions to 527 organizations or Super PACs are not tax-deductible. These organizations are primarily involved in political activities and do not qualify for charitable deductions.

No, expenses incurred while volunteering for a political campaign, such as travel or supplies, are not tax-deductible.

Some states may allow deductions for contributions to state or local political campaigns, but this varies by state. Check your state’s tax laws for specific rules.

![The Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS Penalties](https://m.media-amazon.com/images/I/617DYgupSxL._AC_UL320_.jpg)