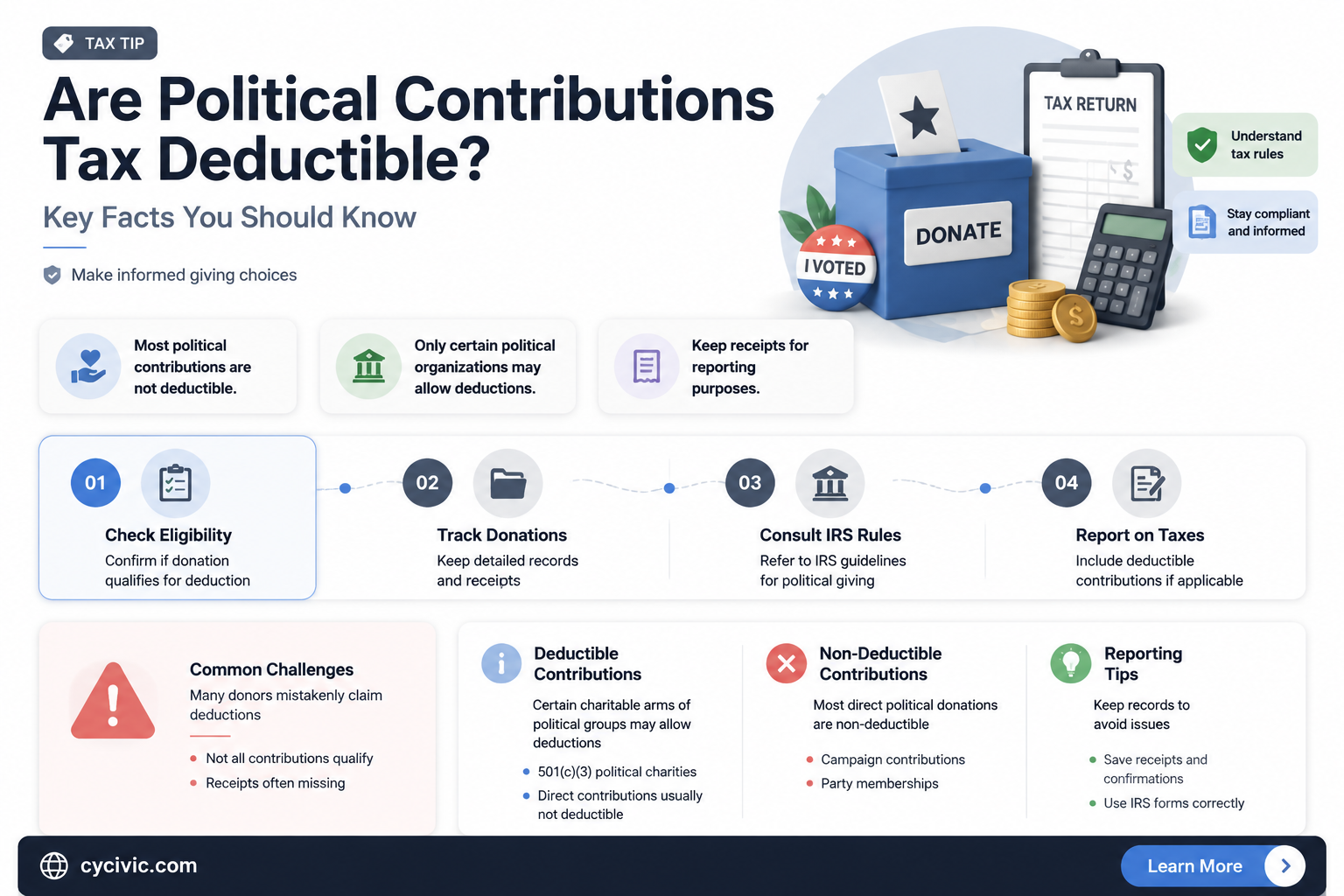

Navigating the complexities of tax deductions can be particularly challenging when it comes to political contributions. Many individuals and businesses wonder whether their financial support for political candidates, parties, or organizations can be deducted from their taxable income. The short answer is no—political contributions are not tax-deductible under U.S. federal law. The Internal Revenue Service (IRS) explicitly states that donations to political campaigns, parties, or action committees (PACs) cannot be claimed as deductions on federal tax returns. However, contributions to certain tax-exempt organizations, such as 501(c)(4) social welfare groups or 527 political organizations, may offer limited tax benefits, though these are not direct deductions. Understanding these distinctions is crucial for taxpayers to avoid errors and ensure compliance with tax regulations.

| Characteristics | Values |

|---|---|

| Deductibility Status | Political contributions are not tax-deductible in the United States. |

| IRS Guidelines | The IRS explicitly states that contributions to political parties, candidates, or campaigns are not eligible for tax deductions. |

| Alternative Deductions | Donations to certain non-profit organizations (e.g., 501(c)(3) charities) are deductible, but political contributions do not qualify. |

| State-Level Variations | Some states may allow deductions for political contributions, but federal tax rules do not permit this. |

| Corporate Contributions | Corporations cannot deduct political contributions as business expenses. |

| Individual Contributions | Individuals cannot claim political contributions as itemized deductions on their federal tax returns. |

| Related Deductible Expenses | Expenses related to volunteering for a political campaign (e.g., travel) may be deductible if there is no compensation. |

| Political Action Committees (PACs) | Contributions to PACs are generally not deductible, though some specific exceptions may apply for certain types of organizations. |

| Last Updated | As of 2023, the IRS maintains that political contributions remain non-deductible under federal tax law. |

Explore related products

$13.9 $25

What You'll Learn

- IRS Rules on Deductions: Political contributions are not tax-deductible as charitable donations under IRS regulations

- (c)(4) Organizations: Donations to certain political groups may be deductible if they meet specific criteria

- State Tax Deductions: Some states allow deductions for political contributions, but rules vary widely

- Business Contributions: Corporations cannot deduct political donations, but individuals can if self-employed

- PAC Donations: Contributions to Political Action Committees (PACs) are generally not tax-deductible

![]()

IRS Rules on Deductions: Political contributions are not tax-deductible as charitable donations under IRS regulations

Political contributions, despite their societal impact, do not qualify as tax-deductible charitable donations under IRS regulations. This rule stems from the IRS's clear distinction between charitable organizations, which must operate exclusively for religious, charitable, scientific, literary, or educational purposes, and political entities, whose primary goal is to influence legislation or support specific candidates. While both types of contributions may reflect personal values, the IRS categorizes them differently for tax purposes. Charitable donations to qualified 501(c)(3) organizations can reduce taxable income, but political contributions, whether to candidates, parties, or political action committees (PACs), offer no such benefit.

For taxpayers seeking to maximize deductions, understanding this distinction is crucial. The IRS Publication 526 outlines eligible charitable contributions, emphasizing that donations to political campaigns, parties, or committees do not meet the criteria. Even contributions to nonprofit organizations with political agendas may not qualify if their primary activities are lobbying or political advocacy. For example, donating to a 501(c)(4) social welfare organization, which can engage in political activities, does not entitle the donor to a deduction. Taxpayers must carefully review the tax status of organizations before assuming their contributions are deductible.

A common misconception arises when individuals conflate political contributions with charitable giving. While both may align with personal beliefs, their tax treatment differs significantly. To avoid errors, taxpayers should maintain clear records of their contributions and verify the tax-exempt status of recipient organizations using the IRS Tax Exempt Organization Search tool. For instance, a donation to a candidate’s campaign fund is not deductible, but a donation to a food bank, even if endorsed by a politician, might be, provided the food bank is a qualified 501(c)(3) organization.

Practical tips for navigating this rule include separating political and charitable contributions in financial records and consulting IRS resources or a tax professional when in doubt. Taxpayers should also be wary of organizations that claim contributions are deductible without proper documentation. For example, a political organization might mistakenly or misleadingly suggest tax benefits, but the IRS’s stance remains firm: political contributions are not deductible. By adhering to these guidelines, taxpayers can ensure compliance while supporting causes they care about without unintended tax consequences.

In summary, the IRS’s exclusion of political contributions from deductible charitable donations reflects a deliberate policy choice to separate political engagement from tax benefits. Taxpayers must remain vigilant, distinguishing between eligible charitable organizations and political entities to avoid errors. While political contributions remain a vital part of civic participation, they do not offer the same financial incentives as charitable donations. Understanding this rule not only ensures compliance but also empowers taxpayers to make informed decisions about their financial and political involvement.

Unequal Political Voice: Does It Shape Democracy and Policy Outcomes?

You may want to see also

Explore related products

![]()

501(c)(4) Organizations: Donations to certain political groups may be deductible if they meet specific criteria

Donations to political organizations often fall into a gray area of tax deductibility, but 501(c)(4) organizations present a unique case. Unlike 501(c)(3) charities, which are strictly prohibited from substantial political activity, 501(c)(4) groups—known as social welfare organizations—can engage in political campaigns and lobbying. However, the deductibility of donations to these groups hinges on the purpose of the contribution. If the donation is earmarked for non-political activities, such as community improvement or educational programs, it may qualify as a tax-deductible business expense under specific circumstances. For instance, a corporation donating to a 501(c)(4) for a local infrastructure project could potentially deduct the contribution as an ordinary and necessary business expense, provided it directly benefits the company’s trade or business.

The IRS scrutinizes donations to 501(c)(4) organizations closely to ensure compliance with tax laws. To qualify for a deduction, the donor must demonstrate that the contribution is not made for political purposes. This distinction is critical because direct political donations, such as those used for campaign ads or candidate endorsements, are never deductible. For example, if a business donates to a 501(c)(4) organization that primarily engages in political advocacy, the contribution would likely not qualify for a deduction. Donors must carefully review the organization’s activities and ensure their donation is allocated to non-political initiatives, such as voter education or community service programs.

One practical tip for donors is to request written confirmation from the 501(c)(4) organization detailing how the contribution will be used. This documentation can serve as evidence to the IRS that the donation was intended for non-political purposes. Additionally, donors should consult with a tax professional to ensure their contribution meets the criteria for deductibility. For instance, a small business owner donating $5,000 to a 501(c)(4) for a local economic development project could claim the deduction if the project directly benefits their business operations, such as improving foot traffic in the area.

Comparatively, donations to 501(c)(3) organizations are straightforwardly deductible for individuals and businesses, but 501(c)(4) donations require a more nuanced approach. While 501(c)(3) groups must remain non-political, 501(c)(4) organizations have more flexibility, which complicates the deductibility question. For example, a donation to a 501(c)(4) focused on environmental advocacy might be deductible if it funds research or public awareness campaigns but not if it supports lobbying efforts. This distinction underscores the importance of understanding the organization’s activities before making a contribution.

In conclusion, donations to 501(c)(4) organizations can be deductible if they are allocated to non-political activities and meet specific IRS criteria. Donors must exercise diligence by verifying the purpose of their contribution and maintaining proper documentation. While the rules are more complex than those for 501(c)(3) donations, strategic giving to 501(c)(4) groups can offer tax benefits while supporting social welfare initiatives. Always consult a tax advisor to navigate this intricate landscape and ensure compliance with current regulations.

Barbie's Political Impact: Unraveling the Movie's Cultural and Social Commentary

You may want to see also

Explore related products

$7.99

$19.58 $36.99

![]()

State Tax Deductions: Some states allow deductions for political contributions, but rules vary widely

While federal tax law prohibits deductions for political contributions, some states offer this benefit, creating a patchwork of rules that donors must navigate carefully. This state-level variation means that where you live can significantly impact the financial implications of your political giving. For instance, in states like Alabama, Arizona, and Iowa, residents can claim deductions or credits for contributions to political parties, candidates, or political action committees (PACs). However, the specifics—such as contribution limits, eligible recipients, and deduction caps—differ widely. Understanding these nuances is crucial for maximizing tax benefits while staying compliant.

Consider Alabama, where taxpayers can deduct up to $50 for individual contributions or $100 for joint filers. In contrast, Iowa allows a credit of up to $50 per taxpayer for contributions to political parties or candidates. Arizona offers a dollar-for-dollar credit for contributions to political parties, but the maximum credit is capped at $443 for individuals and $886 for joint filers in 2023. These examples highlight the importance of consulting state-specific tax codes or a tax professional to ensure eligibility and proper reporting. Missteps could result in disallowed deductions or penalties.

The rationale behind these state deductions varies. Some states aim to encourage political participation by reducing the financial burden of contributing. Others view it as a way to support local political engagement. However, critics argue that such deductions disproportionately benefit wealthier donors who can afford larger contributions. Regardless of intent, the practical takeaway for donors is clear: state tax deductions can offset the cost of political giving, but only if you understand and follow the rules.

To leverage these deductions effectively, start by verifying your state’s policy. Most state revenue departments provide detailed guidance on their websites. Keep meticulous records of contributions, including receipts and acknowledgment letters from recipients. When filing, use the appropriate state tax forms and schedules to claim the deduction or credit. For example, in Arizona, Form 301 is used to claim the political contribution credit. Finally, stay updated on legislative changes, as tax laws can evolve annually. By taking these steps, you can turn your political contributions into a tax-smart strategy.

Understanding the Political Landscape: How Most Americans Engage in Politics

You may want to see also

Explore related products

![]()

Business Contributions: Corporations cannot deduct political donations, but individuals can if self-employed

In the realm of political contributions, a stark contrast emerges between corporations and self-employed individuals. While corporations are barred from deducting political donations, self-employed individuals can claim deductions for such contributions under specific circumstances. This distinction hinges on the tax classification of the contributor and the nature of the donation. For self-employed individuals, political contributions may be deductible as a business expense if they can demonstrate a direct connection between the donation and their trade or business.

Consider the scenario of a freelance consultant who specializes in environmental policy. If this individual donates to a political campaign that advocates for green energy initiatives, the contribution might be deductible as a business expense. The rationale is that supporting such a campaign could potentially benefit the consultant's business by fostering a favorable regulatory environment for their clients. However, the IRS scrutinizes these deductions closely, requiring clear documentation and a reasonable explanation of the business nexus.

To navigate this deduction successfully, self-employed individuals should follow a structured approach. First, ensure the contribution is made to a qualified organization, such as a political party, candidate, or PAC. Second, maintain detailed records, including receipts and documentation linking the donation to business purposes. Third, consult a tax professional to verify eligibility and avoid potential audits. For instance, a sole proprietor might contribute $5,000 to a local candidate’s campaign, then deduct this amount on Schedule C if it directly relates to their business interests, such as influencing legislation affecting their industry.

Contrast this with corporate contributions, which face strict prohibitions. The Bipartisan Campaign Reform Act (BCRA) of 2002 explicitly bans corporations from using treasury funds for political donations. While corporations can establish Political Action Committees (PACs) funded by employee contributions, these donations are not tax-deductible for the corporation. This disparity underscores the tax code’s emphasis on individual agency in political participation, rewarding self-employed individuals for aligning their contributions with business objectives.

In practice, self-employed individuals must tread carefully to maximize this benefit. For example, a graphic designer contributing to a campaign because of personal beliefs would not qualify for a deduction unless the candidate’s platform directly impacts the design industry. The key is proving that the donation serves a legitimate business purpose, not merely personal or ideological interests. By adhering to these guidelines, self-employed individuals can strategically leverage political contributions as a deductible expense, while corporations remain excluded from this tax advantage.

Is a Nation-State Inherently Political? Exploring Sovereignty and Governance

You may want to see also

Explore related products

![]()

PAC Donations: Contributions to Political Action Committees (PACs) are generally not tax-deductible

Contributions to Political Action Committees (PACs) are a common way for individuals and organizations to support political causes, but they come with a critical financial nuance: these donations are generally not tax-deductible. Unlike charitable contributions to 501(c)(3) organizations, which qualify for deductions on federal income taxes, PAC donations fall into a different regulatory category. The IRS classifies PACs as 527 organizations, which are primarily focused on influencing elections or advocating for political issues. This distinction means that while your donation may amplify your political voice, it won’t reduce your taxable income.

Understanding this rule is essential for anyone considering PAC donations. For instance, if you contribute $500 to a PAC supporting a candidate or issue, that $500 is an after-tax expense. It’s treated like any other personal expenditure, such as dining out or purchasing entertainment. This lack of deductibility is intentional, as it prevents taxpayers from using their political contributions to lower their tax liability, which could indirectly subsidize political activity with public funds. For high-income earners in the 37% tax bracket, this means a $1,000 PAC donation effectively costs $1,000, not $630 (after a hypothetical deduction).

One practical tip for donors is to carefully review the tax status of the organization before contributing. Some groups may operate under multiple tax designations, and while their 501(c)(3) arm might accept deductible donations, their PAC arm does not. Always request documentation confirming the organization’s tax status and consult a tax professional if unsure. Additionally, keep detailed records of your contributions, as they may still be subject to reporting requirements, especially if they exceed certain thresholds (e.g., $200 annually for federal PACs).

Comparatively, this rule highlights the broader tax treatment of political versus charitable giving. While both aim to support causes, the IRS draws a clear line between activities that benefit the public at large (charitable) and those that advance specific political interests (PACs). This distinction reflects the government’s interest in maintaining neutrality in the political process, ensuring that tax benefits aren’t used to favor one political group over another. For donors, this means aligning their giving strategy with their financial goals: if tax efficiency is a priority, charitable donations may be more advantageous.

In conclusion, while PAC donations are a powerful tool for political engagement, their non-deductible nature requires careful consideration. Donors should weigh their financial impact, ensure compliance with reporting rules, and distinguish between PACs and charitable organizations. By understanding these specifics, individuals can make informed decisions that align with both their political values and their financial circumstances.

Mastering Polite Communication: Tips for Respectful and Effective Conversations

You may want to see also

Frequently asked questions

No, political contributions are not tax-deductible. The IRS does not allow deductions for donations to political parties, candidates, or campaigns.

Donations to 501(c)(3) nonprofit organizations are generally tax-deductible, but if the organization engages in substantial political campaigning, the portion of your donation used for political activities is not deductible.

No, contributions to PACs are not tax-deductible. These donations are considered political in nature and do not qualify for deductions.

Some out-of-pocket expenses for volunteering, like travel costs, may be deductible if they are not reimbursed and meet IRS guidelines, but direct political contributions are not deductible.

No, donations to 527 organizations or Super PACs are not tax-deductible. These groups are primarily political in nature, and contributions to them do not qualify for deductions.