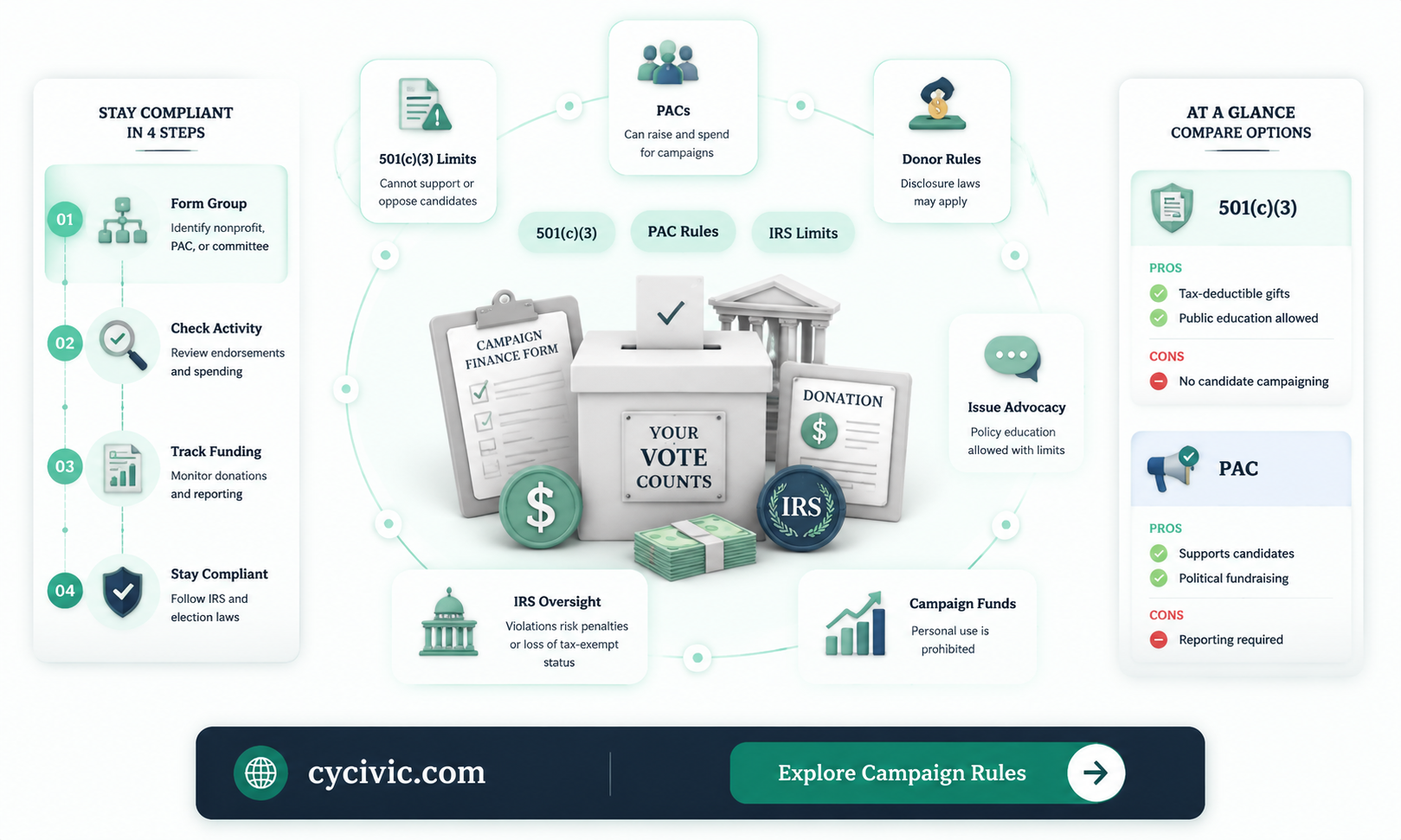

Political campaigns are a crucial aspect of the democratic process, allowing candidates to connect with voters and present their visions for the future. While they are essential, they are also costly, often relying on donations and funding from various sources. This raises the question of whether these campaigns are tax-exempt, and if so, what conditions must be met. The tax status of political campaigns is a complex issue, with various regulations and restrictions in place that determine whether a campaign or organisation is eligible for tax exemption. This includes considerations such as the type of organisation, the nature of its activities, and the rules outlined by the Internal Revenue Service (IRS). Understanding these factors is essential for campaigns to maintain compliance and for donors to be aware of any limitations or implications of their contributions.

Are political campaigns tax exempt?

| Characteristics | Values |

|---|---|

| Political organizations under IRC § 527 | Political parties, campaign committees for candidates for federal, state or local office, and political action committees |

| Requirements for tax exemption under IRC § 527 | Must file periodic reports on Form 8872 with the IRS |

| Tax exemption for organizations with political objectives | Code Section 501(c)(4) organizations can engage in substantial lobbying if it is "germane" to the organization's program |

| Tax exemption for charitable nonprofits | 501(c)(3) charitable nonprofits cannot engage in "political campaign activity" to maintain tax-exempt status |

| Tax deductibility of political contributions | Political contributions are not tax-deductible |

Explore related products

What You'll Learn

![]()

Political donations are not tax-deductible

The tax code is very clear about this, specifically stating that no business expense deduction may be claimed for "any amount paid or incurred in connection with influencing legislation." This rule is so strict that it prevents political candidates from deducting their own out-of-pocket expenses incurred while running for office. Campaign expenses for individuals running for any political office or seeking re-election to any political office cannot be deducted.

The only exception to this rule is for organisations with substantial political or lobbying objectives that are recognised as tax-exempt under Code Section 501(c)(4). Donations to these organisations are not tax-deductible, but they are permitted to engage in substantial lobbying as long as it is "germane" to the organisation's program. An example of a 501(c)(4) organisation is the American Civil Liberties Union, which is permitted to endorse candidates.

On the other hand, charitable donations are generally tax-deductible. Typically, deductible charitable contributions are those made to organisations that are tax-exempt under §501(c)(3) of the Internal Revenue Code. These organisations are specifically barred from attempting to influence legislation or participating in any political campaigns. Examples of charitable organisations that qualify for tax-deductible donations include the American Red Cross, United Way, Girl Scouts of America, and Boy Scouts of America.

Harris' Texas Triumph: Will He Win?

You may want to see also

Explore related products

![]()

Charities and nonprofits can lose tax-exempt status due to political involvement

Charities and nonprofits can lose their tax-exempt status if they engage in "political campaign activity". This prohibition applies to all candidates for federal, state, and local elections. For instance, if a candidate for public office asks to speak at a charitable nonprofit function, the nonprofit should decline the request if the candidate plans to talk about their campaign. However, if the candidate intends to discuss topics related to the nonprofit's mission and other candidates are also invited, then the nonprofit may accept the invitation.

Nonprofits are permitted to engage in nonpartisan voter registration and voter and civic engagement activities, which are not considered partisan campaign activities or lobbying. They can also engage in advocacy and lobbying, which are treated separately under the law. Lobbying involves communicating with decision-makers about existing legislation and urging a vote for or against it. Charitable nonprofits may engage in lobbying as long as they do not expend a significant amount of energy, finances, or other resources on these activities.

Organizations with substantial political or lobbying objectives may be recognized as tax-exempt under Code Section 501(c)(4). The rules for 501(c)(4) organizations differ from those for 501(c)(3) organizations and allow for more substantial lobbying efforts. However, donations to 501(c)(4) organizations are not tax-deductible.

To maintain their tax-exempt status, charitable nonprofits must be vigilant in ensuring that their activities do not cross the line into partisan political campaign activity. Failure to do so could result in losing tax-exempt status or facing penalties, such as intermediate sanctions. Additionally, nonprofits recognized as tax-exempt must file an annual return with the IRS. Not doing so can lead to the automatic revocation of tax-exempt status and the imposition of back taxes and penalties.

Blocking Political Texts: Regaining Your Peace

You may want to see also

Explore related products

$29.22 $33.99

![]()

Political organizations are defined by IRC 527

It is important to note that organizations with substantial political or lobbying objectives may be recognized as tax-exempt under Code Section 501(c)(4). The rules for 501(c)(4) organizations differ from those of 501(c)(3) organizations, allowing the former to engage in significant lobbying activities as long as they are "germane" to the organization's program and meet other limitations. Donations made to 501(c)(4) organizations are not tax-deductible.

On the other hand, 501(c)(3) charitable nonprofits, foundations, or religious organizations typically promise the federal government that they will refrain from engaging in "political campaign activity" to maintain their tax-exempt status. The Supreme Court Decision, Citizens United v. Federal Election Commission, does not alter the restrictions on election-related activities of 501(c)(3) charitable nonprofits.

In summary, while IRC 527 defines political organizations and outlines their tax and filing requirements, other sections of the tax code, such as 501(c)(4) and 501(c)(3), specifically address the tax-exempt status of organizations with political or lobbying activities, with distinct rules and limitations for each type of entity.

The Long Road: Presidential Campaigns and Their Durations

You may want to see also

Explore related products

![]()

IRC 527 outlines requirements for tax exemption

IRC 527 outlines the requirements for tax exemption for political organizations. This includes political parties, campaign committees for candidates for federal, state, or local office, and political action committees. These organizations are subject to specific filing requirements, such as the electronic filing of Form 8872, "Political Organization Report of Contributions and Expenditures."

To maintain their tax-exempt status, organizations must comply with certain restrictions. For instance, 501(c)(3) charitable nonprofits, foundations, or religious organizations must refrain from engaging in "political campaign activity." This restriction applies to all candidates for federal, state, and local elections. Supreme Court decisions, such as Citizens United v. Federal Election Commission, do not override other laws that limit the election-related activities of these nonprofits.

Additionally, 501(c)(3) organizations must not be organized or operated for the benefit of private interests, and none of their net earnings may benefit any private shareholder or individual. They are also prohibited from attempting to influence legislation as a substantial part of their activities. However, it is important to distinguish between political campaign activity and lobbying or legislative activities, which are treated separately under the law. Lobbying by charitable nonprofits is permitted as long as it is not a substantial part of their activities and falls within certain limitations.

Organizations with substantial political or lobbying objectives may seek tax exemption under Section 501(c)(4). These organizations are permitted to engage in substantial lobbying as long as it is "germane" to their program and meets other limitations. Donations to 501(c)(4) organizations are not tax-deductible.

Campaigns: Best Times to Launch and Gain Traction

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![]()

Some tax-exempt organizations can engage in lobbying

While 501(c)(3) charitable nonprofits, foundations, or religious organizations are prohibited from engaging in "political campaign activity" in return for their tax-exempt status, they are allowed to engage in some lobbying. However, they must be careful not to expend too much energy, finances, or other resources on these activities, or they risk losing their tax-exempt status.

Lobbying is defined as communicating with decision-makers about existing legislation and urging a vote for or against it. Direct lobbying involves contacting members or employees of a legislative body or government officials involved in formulating legislation, such as members of Congress, their staff, or committee staff. Grassroots lobbying, on the other hand, attempts to influence public opinion and encourage the audience to take action on the legislation.

There are two methods to determine whether an organization has engaged in "substantial" lobbying activities: the substantial part test, which considers the facts and circumstances, and the expenditure test, a mathematical formula based on the filing of a 501(h) election. At the federal level, no more than 25% of lobbying expenses can be allocated to grassroots lobbying.

Organizations with substantial political or lobbying objectives may be recognized as tax-exempt under Code Section 501(c)(4). Unlike 501(c)(3) organizations, 501(c)(4) organizations are permitted to engage in substantial lobbying as long as it is "germane" to the organization's program and meets other limitations. Donations to 501(c)(4) organizations are not tax-deductible.

It is important to note that engaging in issues of public policy does not constitute lobbying. For example, organizations may conduct educational meetings or distribute educational materials without jeopardizing their tax-exempt status.

Political Texts: Why Am I Getting Bombarded?

You may want to see also

Frequently asked questions

Political organizations are exempt from taxes under IRC Section 527. This includes political parties, campaign committees for candidates for federal, state, or local office, and political action committees. However, organizations with charitable or educational purposes, such as 501(c)(3) organizations, are prohibited from engaging in political campaign activity to maintain their tax-exempt status.

A political organization, as defined by Section 527(e)(1), is "a party, committee, association, fund, or other organization" that primarily accepts contributions and/or makes expenditures for influencing federal, state, or local elections.

No, political contributions are not tax-deductible. This applies to donations made to political candidates, parties, or action committees. However, you may be able to lower your taxable income by claiming other deductions, such as itemized deductions for mortgage interest, state and local taxes, or medical expenses.

While tax-exempt organizations can engage in some political activities, they must be careful not to cross the line into "political campaign activity." This includes allowing a candidate for public office to speak at a function if they plan to talk about their campaign. Charities, churches, and other 501(c)(3) organizations have lost their tax-exempt status due to involvement with political campaigns.

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UY218_.jpg)