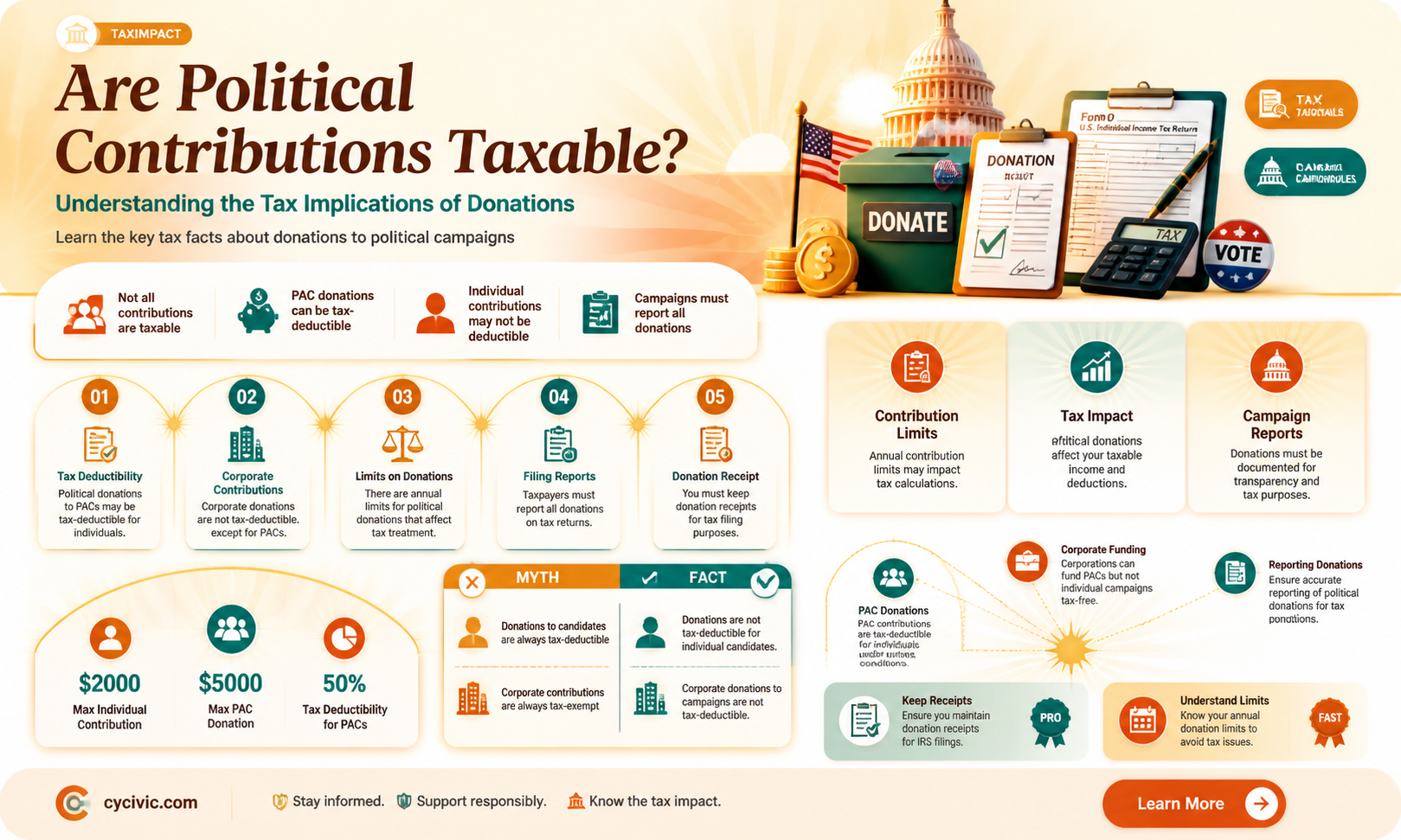

The question of whether contributions to politics are taxable is a complex and nuanced issue that intersects tax law, campaign finance regulations, and political participation. In many jurisdictions, including the United States, individual donations to political campaigns or organizations are generally not considered taxable income for the recipient, as they are viewed as gifts rather than revenue. However, these contributions may be subject to reporting requirements and limits to ensure transparency and prevent corruption. Additionally, while donors typically do not receive a tax deduction for political contributions, certain exceptions exist, such as donations to political action committees (PACs) or charitable arms of political organizations. Understanding the tax implications of political contributions requires careful consideration of both federal and state laws, as well as the specific nature of the contribution and the entity receiving it.

| Characteristics | Values |

|---|---|

| Taxability of Political Contributions | Generally, contributions to political campaigns, parties, or candidates are not tax-deductible for individuals. |

| 501(c)(4) Organizations | Donations to 501(c)(4) social welfare organizations, which can engage in political activities, are not tax-deductible. |

| 527 Organizations | Contributions to 527 political organizations are not tax-deductible. |

| PACs (Political Action Committees) | Donations to PACs are not tax-deductible. |

| Super PACs | Contributions to Super PACs are not tax-deductible. |

| Charitable Organizations (501(c)(3)) | Donations to 501(c)(3) charitable organizations are tax-deductible, but these organizations are prohibited from engaging in substantial political activity. |

| State and Local Tax Laws | Some states may allow deductions for political contributions, but this varies widely and is generally limited. |

| Corporate Contributions | Corporations cannot deduct political contributions as business expenses for federal income tax purposes. |

| Gift Tax Considerations | Large political contributions may be subject to gift tax rules if they exceed the annual gift tax exclusion amount. |

| IRS Reporting Requirements | Political organizations may need to file IRS forms (e.g., Form 8872) to report contributions, but this does not affect the taxability of contributions for donors. |

| Foreign Contributions | It is illegal for foreign nationals to contribute to U.S. political campaigns, and such contributions are not tax-deductible. |

| Bundling Contributions | Bundling contributions (collecting and forwarding donations) does not change their non-deductible status. |

Explore related products

What You'll Learn

- Campaign Donations: Are individual contributions to political campaigns considered taxable income or deductible expenses

- Political Action Committees (PACs): How are PAC contributions taxed for donors and organizations

- In-Kind Contributions: Are non-monetary donations (e.g., services, goods) taxable for political entities

- Tax Deductions for Donors: Can individuals or businesses deduct political contributions from taxable income

- Foreign Contributions: Are political donations from non-U.S. citizens or entities taxable or illegal

![]()

Campaign Donations: Are individual contributions to political campaigns considered taxable income or deductible expenses?

In the United States, individual contributions to political campaigns are generally not considered taxable income for the recipient candidate or campaign. The Internal Revenue Service (IRS) classifies these donations as gifts, which are not subject to federal income tax. However, this does not mean donors can claim these contributions as deductible expenses on their personal tax returns. The tax treatment of campaign donations is governed by specific rules that balance the principles of free speech with the need for transparency and fairness in the political process.

For donors, the key takeaway is that contributions to political campaigns are typically not tax-deductible. Unlike charitable donations, which can reduce taxable income, political contributions fall into a separate category. The IRS explicitly states that donations to political parties, candidates, or political action committees (PACs) are not eligible for deductions. This rule applies regardless of the amount donated, whether it’s $50 or $5,000. For example, if an individual donates $250 to a local candidate, they cannot subtract this amount from their taxable income when filing their annual return.

One exception to this rule involves contributions to certain political organizations that qualify as 501(c)(4) social welfare organizations or 527 political organizations. In rare cases, donations to these groups may be partially deductible as business expenses if they are directly related to the taxpayer’s trade or business. However, this is a narrow exception and requires careful documentation to avoid scrutiny from the IRS. For instance, a small business owner might deduct a contribution if it can be proven that the donation was made to influence legislation directly impacting their industry.

It’s also important to note that while donations themselves are not taxable or deductible, the way campaigns use those funds can have tax implications. Campaigns must report contributions over certain thresholds to the Federal Election Commission (FEC) and may be subject to payroll taxes if they pay staff or contractors. Donors, however, remain unaffected by these requirements. To stay compliant, donors should keep records of their contributions, especially if they approach or exceed federal limits, such as the $3,300 per election cap for individual donations to a candidate committee.

In summary, individual contributions to political campaigns are neither taxable income for recipients nor deductible expenses for donors under standard IRS rules. While exceptions exist for specific types of political organizations, these are limited and require careful justification. Donors should focus on understanding contribution limits and reporting requirements rather than seeking tax benefits. By adhering to these guidelines, individuals can participate in the political process without unintended financial consequences.

Are Asian Americans Politically Oppressed? Exploring Systemic Barriers and Representation

You may want to see also

Explore related products

![]()

Political Action Committees (PACs): How are PAC contributions taxed for donors and organizations?

Political Action Committees (PACs) serve as vital conduits for funneling money into political campaigns, but the tax implications of contributing to these organizations are often misunderstood. For individual donors, contributions to PACs are generally not tax-deductible. The IRS classifies these donations as gifts to political organizations rather than charitable contributions, meaning they cannot be claimed as deductions on federal income tax returns. This rule applies regardless of whether the PAC supports a candidate, party, or specific issue. Donors should carefully track their contributions to avoid mistakenly claiming them as deductions during tax season.

Organizations, particularly corporations and unions, face distinct rules when contributing to PACs. Under federal law, corporations and unions are prohibited from donating directly to federal candidates or party committees, but they can legally contribute to PACs. These contributions, however, are not tax-deductible as business expenses. Additionally, organizations must ensure compliance with reporting requirements, as failure to disclose PAC contributions can result in penalties. For instance, corporations must report PAC donations on their tax returns using specific forms, such as Schedule C for Form 1120, to maintain transparency and avoid legal repercussions.

One critical distinction in PAC taxation lies in the treatment of Super PACs versus traditional PACs. Traditional PACs, also known as connected PACs, are subject to contribution limits and can only accept donations from individuals, other PACs, and certain organizations. Super PACs, on the other hand, can accept unlimited contributions from individuals, corporations, and unions but are prohibited from coordinating directly with candidates. Despite these differences, contributions to both types of PACs remain non-deductible for tax purposes. Donors to Super PACs, however, should be aware of potential state-level regulations, as some states impose additional restrictions or reporting requirements on large political donations.

Practical tips for navigating PAC contributions include maintaining detailed records of all donations, consulting a tax professional to ensure compliance, and staying informed about changes in campaign finance laws. For organizations, establishing internal policies for PAC contributions can help prevent accidental violations. Individuals should also be cautious of scams or fraudulent PACs, as legitimate PACs are required to register with the Federal Election Commission (FEC) and disclose their financial activities. By understanding the tax rules and regulatory landscape, donors and organizations can support political causes effectively while avoiding costly mistakes.

Are Most Political Reporters Liberal? Uncovering Media Bias in Journalism

You may want to see also

Explore related products

![]()

In-Kind Contributions: Are non-monetary donations (e.g., services, goods) taxable for political entities?

Non-monetary donations, such as services, goods, or property, known as in-kind contributions, play a significant role in political campaigns and organizations. These contributions can range from volunteering time and expertise to donating office space, equipment, or even meals for campaign events. While the tax treatment of cash contributions to political entities is relatively straightforward, the rules surrounding in-kind donations are more nuanced and often misunderstood.

In the United States, the Federal Election Commission (FEC) considers in-kind contributions as anything of value given to a political committee, candidate, or party for political purposes. This broad definition encompasses a wide array of non-monetary donations. For instance, a graphic designer offering to create campaign materials or a local business providing free advertising space would both be making in-kind contributions. The key distinction here is that these donations are not made in cash but still hold value and can significantly impact a political campaign's success.

From a tax perspective, the treatment of in-kind contributions can be complex. Generally, the donor of an in-kind contribution cannot claim a tax deduction for the fair market value of the goods or services provided. This is because political contributions, whether monetary or in-kind, are not considered charitable donations for tax purposes. The Internal Revenue Service (IRS) clearly states that contributions to political parties, candidates, or action committees are not deductible. However, there is an important exception for volunteers' out-of-pocket expenses. If a volunteer incurs expenses while providing services for a political organization, they may be able to deduct these expenses on their tax return, provided they are not reimbursed and the expenses are directly related to the volunteer work.

It is crucial for political entities to properly value and report in-kind contributions. The FEC requires that the value of in-kind contributions be estimated and reported, ensuring transparency and compliance with campaign finance laws. For example, if a company donates the use of its corporate jet for a candidate's travel, the campaign must report the fair market value of that travel as an in-kind contribution. This valuation process can be challenging, especially for unique or specialized services, and may require professional appraisals to ensure accuracy.

In summary, while in-kind contributions are a vital part of political fundraising, they are generally not taxable for the recipient political entities. However, donors should be aware that they cannot claim tax deductions for these non-monetary donations. Proper valuation and reporting of in-kind contributions are essential to maintain compliance with election regulations, ensuring a transparent and fair political process. This unique aspect of political contributions highlights the importance of understanding the specific rules governing non-monetary donations in the political arena.

Mastering Polite Conversation: Tips to Engage and Connect Effortlessly

You may want to see also

Explore related products

![]()

Tax Deductions for Donors: Can individuals or businesses deduct political contributions from taxable income?

In the United States, political contributions by individuals and businesses are generally not tax-deductible. This rule is rooted in the Internal Revenue Code (IRC) Section 162(e), which explicitly disallows deductions for contributions made to political parties, candidates, or campaign committees. The rationale is to prevent taxpayers from using deductions to indirectly subsidize political activities, ensuring that such funding remains transparent and voluntary.

For individuals, this means that donations to political campaigns, parties, or political action committees (PACs) cannot be claimed as charitable deductions or itemized deductions on federal tax returns. Similarly, businesses face restrictions under IRC Section 162(e)(1), which prohibits the deduction of political contributions as ordinary and necessary business expenses. However, there’s a nuanced exception: businesses can deduct certain lobbying expenses, provided they are separately stated and not directly tied to political campaigns.

A common misconception arises from the tax treatment of donations to 501(c)(4) organizations, often referred to as "social welfare" groups. While contributions to these organizations are not deductible, they can engage in limited political activity. Donors must carefully distinguish between deductible charitable contributions (e.g., to 501(c)(3) nonprofits) and non-deductible political or advocacy-related donations. For instance, a $1,000 donation to a candidate’s campaign is non-deductible, whereas a donation to a charity supporting voter education might qualify, depending on the organization’s structure.

Practical tip: Individuals and businesses should maintain clear records of political contributions to avoid inadvertently claiming them as deductions. Tax software and accountants often flag such entries, but proactive awareness can prevent errors. Additionally, businesses should consult tax professionals to ensure lobbying expenses are properly documented and comply with IRS guidelines.

In contrast to the U.S., some countries allow limited tax deductions for political contributions under specific conditions. For example, Canada permits individuals to claim a tax credit for political donations up to $650 annually, with a tiered credit rate. This comparative approach highlights the U.S. system’s stricter stance, emphasizing the importance of understanding local tax laws when engaging in political giving. Ultimately, while political contributions remain a vital part of civic engagement, their non-deductible nature underscores the separation between private financial incentives and public political participation.

Do You Believe in Politics? Exploring Trust, Ideals, and Reality

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![]()

Foreign Contributions: Are political donations from non-U.S. citizens or entities taxable or illegal?

Political donations from non-U.S. citizens or entities are strictly prohibited under U.S. federal law. The Federal Election Campaign Act (FECA) explicitly bans foreign nationals, foreign corporations, and foreign governments from making contributions, donations, or expenditures in connection with any U.S. election. This prohibition extends to all levels of political campaigns, including federal, state, and local races. Violations can result in severe penalties, including fines and imprisonment, as enforced by the Federal Election Commission (FEC) and the Department of Justice (DOJ).

The rationale behind this ban is rooted in national security and the integrity of the democratic process. Allowing foreign contributions could enable outside influences to sway U.S. elections, undermining the principle of self-governance. For instance, a foreign entity might donate to a candidate who aligns with their geopolitical interests, potentially compromising U.S. sovereignty. This concern is not hypothetical; high-profile cases, such as the 2016 investigation into foreign interference, highlight the risks of unregulated foreign involvement in U.S. politics.

Despite the clear legal prohibition, enforcement remains challenging. Foreign actors may attempt to circumvent the law through straw donors, shell companies, or other covert methods. The rise of digital fundraising platforms has further complicated detection, as online donations can be harder to trace. To address this, the FEC and DOJ have increased scrutiny of campaign finances, particularly during election seasons. Campaigns are required to vet donors carefully, rejecting any contributions that appear to originate from foreign sources.

For individuals and organizations involved in political fundraising, understanding these rules is critical. Campaigns must implement robust compliance measures, such as verifying donor citizenship and ensuring transparency in financial reporting. Failure to do so can result in legal consequences for both the donor and the recipient. For example, a campaign that unknowingly accepts a foreign donation could face fines, negative publicity, and damage to its credibility.

In summary, foreign contributions to U.S. political campaigns are not only illegal but also non-taxable, as they are prohibited outright. The law prioritizes protecting the electoral process from external influence, even if it means forgoing potential revenue. For those engaged in political fundraising, vigilance and adherence to legal guidelines are essential to avoid inadvertently violating this critical restriction.

Is Critical Race Theory Political? Unraveling the Debate and Implications

You may want to see also

Frequently asked questions

No, contributions to political campaigns are generally not taxable for the donor. However, they are not tax-deductible either, as they are considered gifts for tax purposes.

No, political contributions made by individuals are not subject to income tax. They are treated as personal expenses, not taxable income.

Corporations and organizations cannot deduct political contributions as business expenses, and such contributions are typically made with after-tax dollars. However, they may face other restrictions or reporting requirements depending on the jurisdiction.

No, political donations are generally not considered taxable income for the recipient. They are treated as nontaxable gifts or contributions for political purposes, though they must comply with campaign finance laws and reporting requirements.

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UL320_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UL320_.jpg)

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)