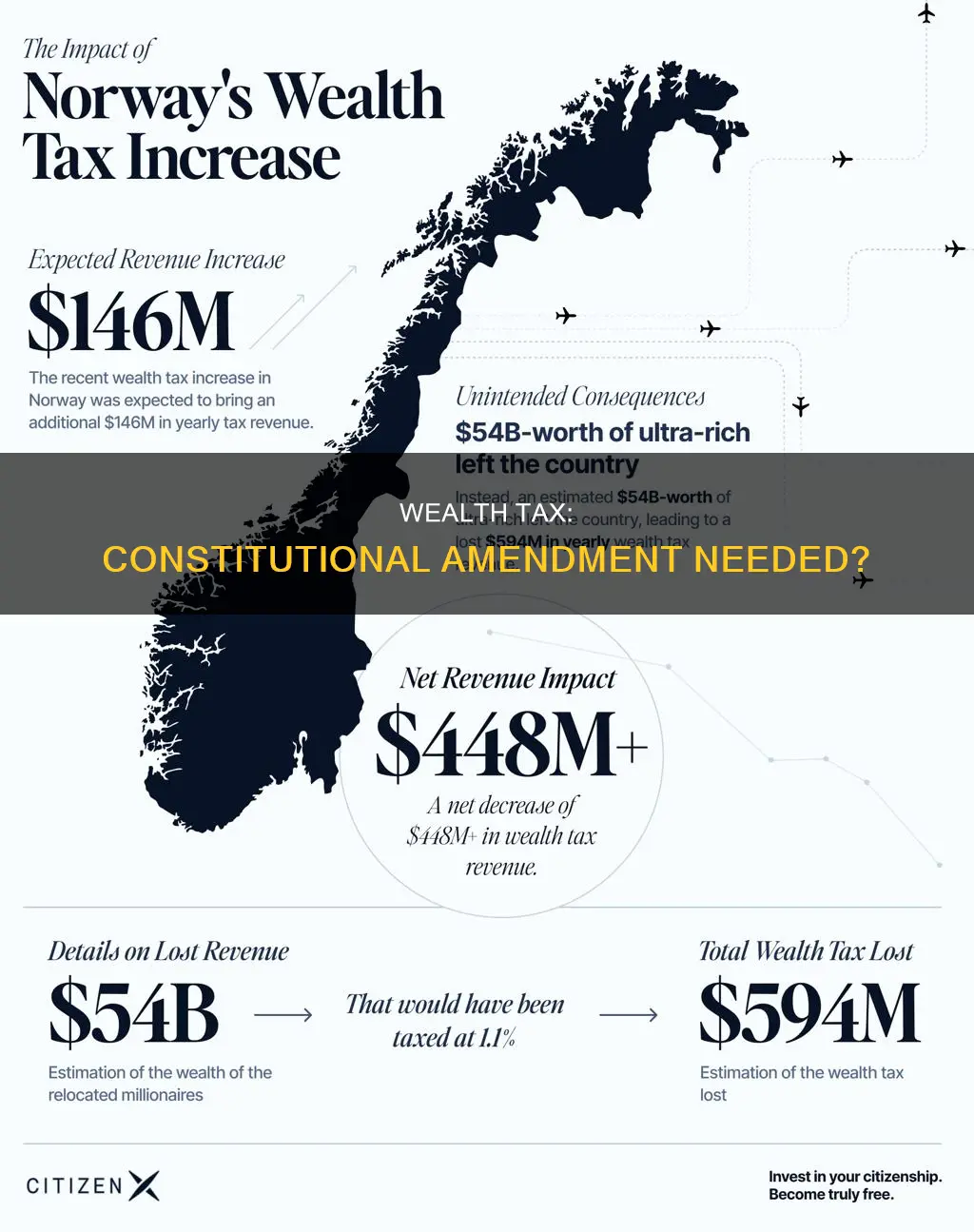

The idea of a wealth tax has gained traction in recent years, with proponents suggesting it could be a means to reduce inequality and generate revenue. However, the constitutionality of such a tax is a complex issue, with some arguing that it would require a constitutional amendment. The primary question revolves around whether a wealth tax would be considered a direct tax under the US Constitution, which would require apportionment among the states based on population. The Supreme Court has addressed the issue of direct taxes in several cases, but the definition remains unclear, and the Court's reinterpretation of direct taxes or creation of a new exception could significantly impact the feasibility of a wealth tax.

| Characteristics | Values |

|---|---|

| Constitutionality of wealth tax | Uncertain, would likely require a constitutional amendment |

| Constitutionality of income tax | Authorized by the 16th Amendment |

| State-level wealth taxes | Likely constitutional |

| Federal wealth tax | Likely unconstitutional without another amendment |

| Apportionment | Required for direct taxes, including taxes on real estate and personal property (wealth) |

| Direct tax | A wealth tax would likely be classified as a direct tax, requiring apportionment |

| Supreme Court | Could potentially reinterpret the definition of direct taxes, creating an exception for wealth taxes |

| Founders' standards | Apportionment of a wealth tax by population would require higher tax rates in poorer states, which would be unjust |

| Constitutional requirements | Significant judicial interpretation would be required for a wealth tax to align with constitutional requirements |

Explore related products

What You'll Learn

![]()

The 5th Amendment's no taking clause

The question of whether a wealth tax would require a constitutional amendment in the United States is a complex one. Some argue that it is indeed constitutional under the standards laid down by the Founders, as apportionment of a wealth or land tax by population was not written to protect wealth. Instead, it was meant to reach wealth by what was thought to be the best then-available measure of wealth.

On the other hand, some argue that it may be unconstitutional, as the 16th Amendment only allows the collection of income taxes. State-level wealth taxes are almost certainly constitutional as they already exist, but this does not impact whether a federal wealth tax is constitutional.

The Fifth Amendment's "No Taking Clause" is relevant to this discussion as it limits the government's power of eminent domain. The clause states that private property can only be taken for public use if the government provides "just compensation". This clause was likely adopted in response to the Continental Army's practice of seizing military supplies without compensation during the Revolutionary War. It is important to note that the Takings Clause originally applied only to the federal government, but a Supreme Court ruling in 1897 extended its effects to the states.

In conclusion, while there are differing opinions on whether a wealth tax requires a constitutional amendment, the Fifth Amendment's No Taking Clause protects citizens by requiring just compensation for the taking of private property for public use.

Amendments for Prohibition: A Historical Overview

You may want to see also

Explore related products

![]()

The 16th Amendment

Critics of the 16th Amendment argue that it enables expansive federal government spending and facilitates central banking policies. Some have also questioned whether a wealth tax would be constitutional, as the 16th Amendment only mentions income taxes. However, state-level wealth taxes already exist and are considered constitutional, and supporters of a federal wealth tax argue that it would be constitutional under the standards laid down by the Founders.

Racial Profiling: The Constitutional Amendment Protection

You may want to see also

Explore related products

![]()

The definition of direct tax

The definition of a direct tax is a tax imposed directly on an individual or company, which cannot be passed on to another taxpayer. Direct taxes are paid directly to the government and are progressive in nature, meaning that the tax burden increases with income. In other words, individuals or companies with higher incomes will pay a larger share of the tax burden. Common examples of direct taxes include income tax, corporate tax, property tax, capital gains tax, and use taxes such as vehicle licensing and registration fees.

Direct taxes are the opposite of indirect taxes, which can be passed on to another entity or individual. Indirect taxes are levied on goods and services, and the supplier or manufacturer passes the tax on to the consumer, who ultimately pays the tax. Examples of indirect taxes include sales tax, excise tax, value-added tax (VAT), and goods and services tax (GST).

The distinction between direct and indirect taxes is important for companies to understand their cost structure and how much they may owe in taxes. Direct taxes can be complex, especially for companies operating in multiple states, so tax software can be leveraged to speed up and automate the financial close process.

In the United States, the 16th Amendment to the Constitution in 1913 changed the tax code by allowing the levying of numerous direct and indirect taxes. Prior to this amendment, direct taxes had to be directly apportioned to a state's population, which limited the federal government's ability to impose many direct taxes. The constitutionality of a wealth tax in the United States is still a matter of debate, with some arguing that it would require a constitutional amendment. However, state-level wealth taxes already exist and are considered constitutional.

Understanding Group Formation: The Constitutional Amendment

You may want to see also

Explore related products

![]()

The question of what counts as income

The Supreme Court has addressed the issue of direct taxes in several cases, including Pollock v. Farmers' Loan & Trust Co. (1895), where it ruled that taxes on real estate and personal property are direct taxes requiring apportionment. The Court's decision in Eisner v. Macomber (1920) further established that income must be "realized" to be taxable under the 16th Amendment. This perspective was reinforced by the Court's summary in 1955, which stated that taxable "gross income" includes "undeniable accessions to wealth, clearly realized, and over which the taxpayers have complete dominion".

The proposed wealth tax by Senator Warren and others would be a tax on wealth itself, rather than accessions to wealth, and it would be levied before realization. This raises the question of whether wealth can be considered income under the 16th Amendment. Some scholars and policymakers argue that the current perspective on realization is outdated and that there may be a realization requirement under the amendment.

Additionally, proposals to tax unrecognized gains or unrealized capital gains among the extremely wealthy have emerged. However, this approach faces constitutional hurdles as it may fall outside the scope of income taxation as defined by the 16th Amendment, reinforcing the view that it would be a direct tax requiring apportionment. The constitutionality of a wealth tax on unrealized gains is uncertain and would likely face significant legal challenges, requiring either a constitutional amendment or a reinterpretation of existing tax law by the Supreme Court.

Floridians Supporting Amendments: Who's Behind the Changes?

You may want to see also

Explore related products

![]()

The valuation of assets

Parametric Valuation: One approach to valuing assets for a wealth tax is parametric valuation, which relies on easily measurable characteristics or parameters. For instance, the valuation of real estate could be based on square footage and location, while the valuation of stocks and bonds could be based on their market prices. This method is relatively straightforward and transparent, ensuring consistency in assessment across taxpayers. However, parametric valuation may oversimplify the worth of certain assets and fail to capture unique characteristics that could affect value.

Income-Based Valuation: Another approach ties the valuation of assets to the income they generate. This income-based approach is particularly relevant for assets that provide a stream of future benefits or cash flows, such as rental properties or businesses. By discounting future income streams to their present value, a more economically meaningful valuation can be derived. This method is advantageous for illiquid assets that may not have a readily observable market price. However, accurately projecting future income streams and selecting an appropriate discount rate can be challenging and subject to manipulation or dispute.

Market-Based Valuation: Market-based valuation relies on the principle of substitutability, where the value of an asset is determined by the price of similar assets traded in an active market. This approach is commonly used for publicly traded securities and commodities. It provides a more immediate and objective valuation, particularly for liquid assets. However, market-based valuation may not be feasible for unique or illiquid assets without direct comparables, and it can be susceptible to market volatility and manipulation.

Independent Appraisal: In certain cases, particularly for unique or illiquid assets, independent appraisals may be necessary. This involves engaging qualified experts to assess the value of an asset based on a set of relevant factors. Appraisals can be complex and time-consuming, and the quality and objectivity of the valuation heavily depend on the expertise and independence of the appraiser. To ensure consistency and prevent bias, a standardized framework for selecting and engaging appraisers would need to be established.

International Coordination: Implementing a wealth tax in a globalized economy requires international coordination to prevent tax avoidance through offshore holdings. This coordination could include information sharing between tax authorities, common standards for asset valuation, and harmonized tax rates to reduce the incentive to move assets to lower-tax jurisdictions. International collaboration is crucial to ensuring the effectiveness and fairness of a wealth tax, particularly given the mobile nature of financial capital.

Frequency of Valuation: The frequency of asset valuation would also need to be determined. A yearly valuation could be burdensome and lead to volatility in tax liabilities, especially for assets with fluctuating market values. Alternatively, a less frequent valuation, such as every three to five years, could reduce administrative costs and provide more stability for taxpayers, but it may also create opportunities for tax avoidance through strategic timing of asset transfers.

In conclusion, the valuation of assets for a wealth tax requires a careful balance between simplicity and accuracy. A comprehensive wealth tax would necessitate a combination of these valuation approaches, tailored to different types of assets. While parametric and market-based valuations offer simplicity and transparency, income-based valuations and independent appraisals may be more appropriate for certain illiquid or unique assets. International coordination and careful consideration of valuation frequency are also essential to ensure the effectiveness and fairness of the tax system.

The Right to Vote: Constitutional Amendment for All

You may want to see also

Frequently asked questions

It is unclear whether a wealth tax would be constitutional. Some scholars argue that a wealth tax would be unconstitutional, citing an 1895 case—Pollock v. Farmers’ Loan and Trust—where the Supreme Court ruled that an income tax was a direct tax. However, others argue that a wealth tax would be constitutional, claiming that the Pollock decision was wrongly decided.

The Fifth Amendment states that there shall be "no taking of private property without just compensation". As a person's assets are property, taxes based on a person's net worth are in violation of the "no-taking clause".

Proponents of a wealth tax argue that the tax is not a direct tax for which apportionment is required. Apportionment was not written to protect wealth but to reach wealth by the best available measure.

During the 2020 presidential campaign, Senators Bernie Sanders and Elizabeth Warren proposed wealth taxes on the holdings of the very wealthy. However, the unique features of the US tax system, economy, and Constitution could impede the adoption of a wealth tax.