Virginia Question 2, the Remove Restriction on Residence for Surviving Spouse of Disabled Veteran Tax Exemption Amendment, was proposed by Rep. Jason S. Miyares (R-82) and introduced into the Virginia General Assembly as House Joint Resolution 562 on December 23, 2016. The amendment was approved by the House of Representatives on February 6, 2017, with a vote of 95 to 0. This proposed amendment aimed to remove the restriction on surviving spouses of disabled veterans, allowing them to claim a real property tax exemption regardless of their place of residence. It was on the ballot in Virginia as a legislatively referred constitutional amendment on November 6, 2018, and was approved by voters.

| Characteristics | Values |

|---|---|

| Date | November 6, 2018 |

| Title | Remove Restriction on Residence for Surviving Spouse of Disabled Veteran Tax Exemption Amendment |

| Description | Amended the state constitution to remove restrictions on the surviving spouse's ability to receive the property tax exemption and move to a new principal place of residence |

| Proposer | Rep. Jason S. Miyares (R-82) |

| Result | Approved |

Explore related products

$9.99 $9.99

What You'll Learn

![]()

Tax exemption for spouses of soldiers killed in action

The proposed Virginia Constitutional Amendment Question 2, which will be voted on in the November 2024 elections, seeks to extend tax exemption to the surviving spouses of soldiers who died in the line of duty, in addition to those killed in action.

Currently, under the Virginia Constitution, all property is subject to taxation. However, specific types of property may be exempted. The Constitution allows the General Assembly to exempt the principal residence of a surviving spouse of a soldier killed in action, as determined by the U.S. Department of Defense, from taxation.

The proposed amendment aims to expand this tax exemption to include surviving spouses of all soldiers who died in the line of duty, as determined by the U.S. Department of Defense. This means that if the amendment is approved, surviving spouses of soldiers who died while serving their country, regardless of whether they were killed in direct combat, would be eligible for the same property tax exemption on their primary residence.

The specific wording of the proposed amendment is not yet available, but the ballot question will ask voters whether they approve of this expansion of the tax exemption. A "yes" vote will allow surviving spouses of soldiers who died in the line of duty to claim the same property tax exemption, while a "no" vote will maintain the current situation, where only surviving spouses of soldiers killed in action are eligible for the exemption.

This amendment is part of a series of proposed changes to the Virginia Constitution, which are put to a vote every two years. The tax exemption for spouses of soldiers killed in action was previously addressed in the 2018 ballot, where the scope of eligible spouses was expanded to include those who moved to a new principal place of residence.

Florida Amendment Petitions: Where to Mail?

You may want to see also

Explore related products

![]()

Tax exemption for spouses of disabled veterans

The proposed Virginia Constitutional Amendment Question 2 seeks to expand the tax exemption benefit to surviving spouses of soldiers who died in the line of duty, in addition to those killed in action. This amendment will ensure that the spouses of disabled veterans can retain their tax exemption even if they move to a different locality within Virginia, as long as the new residence is their principal place of residence and they do not remarry.

The current Virginia Constitution mandates the taxation of all property, but it also specifies certain types of property that are exempt from taxation. One such exemption is the principal residence of a soldier's surviving spouse, but only if the soldier was killed in action, as determined by the U.S. Department of Defense. The proposed amendment aims to extend this exemption to surviving spouses of all soldiers who died in the line of duty, as determined by the same authority.

The tax exemption for spouses of disabled veterans is a valuable benefit that provides financial relief to those who have sacrificed much for their country. The proposed amendment recognizes that the loss of a spouse through their service to the country is a significant sacrifice, regardless of whether the soldier was killed in action or died in the line of duty. By expanding the tax exemption, this amendment seeks to offer a measure of support and recognition to these surviving spouses.

To qualify for the tax exemption, the spouse must not remarry and must occupy the property as their principal place of residence. The property can be owned by the veteran, the veteran's spouse, or jointly by both. In the case of multiple qualified claimants residing in the same property, each claimant is entitled to the exemption relative to their interest in the property. Additionally, if the claimant is confined to a hospital or care facility, the property is still considered their principal place of residence, provided it is not rented or leased to another party.

The process to claim the tax exemption involves providing the necessary documentation to the local assessor's office. This includes proof of the veteran's disability, usually in the form of a letter from the USDVA, and proof that the character of service was under "other than dishonorable" conditions. Unmarried surviving spouses may also need to attach additional documents depending on the specific circumstances.

Amending the Constitution: Exploring the Process

You may want to see also

Explore related products

![]()

Redistricting commission proposal

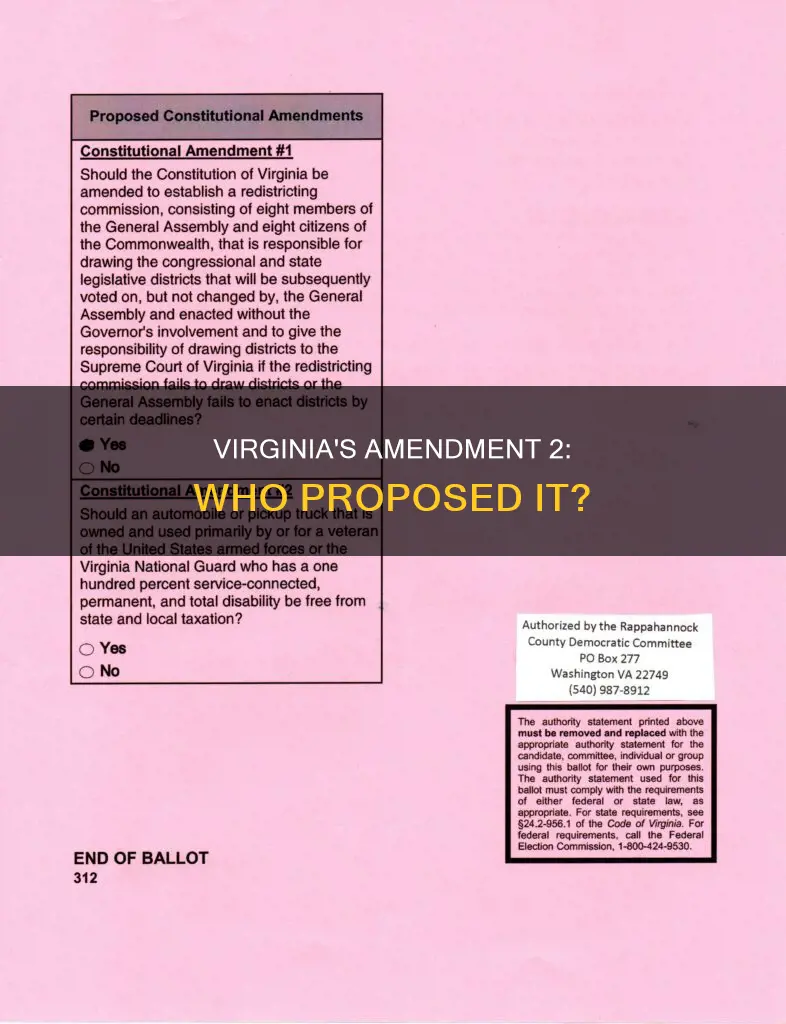

The Redistricting Commission Proposal, also known as Virginia Question 1, was a ballot measure proposed as Senate Joint Resolution 306 (SJR 306) and House Joint Resolution 615 (HJR 615). The proposal aimed to amend the Constitution of Virginia to establish a redistricting commission responsible for drawing congressional and state legislative districts.

The current process in Virginia involves the General Assembly and the Governor being responsible for drawing new election districts for the U.S. House of Representatives, the state Senate, and the House of Delegates. These districts are required to be compact, contiguous, and have equal populations. The proposed amendment sought to shift this responsibility to a redistricting commission, consisting of eight members of the General Assembly and eight citizens of the Commonwealth. The commission's task would be to draw districts that would be subsequently voted on by the General Assembly without the involvement of the Governor. If the commission or the General Assembly failed to meet certain deadlines, the responsibility would then fall to the Supreme Court of Virginia.

The proposal was introduced by Sen. George Barker (D-39) as SJR 306 on January 9, 2019, and Del. Mark Cole (R-88) as HJR 615 on January 1, 2019. Both resolutions initially presented different approaches to changing the redistricting process. However, in a conference committee, the texts were modified to be identical, and both were passed by the General Assembly. SJR 306 received overwhelming approval in the House of Delegates with an 85-13 vote and in the Senate with a 39-1 vote. HJR 615 also passed with the necessary majority in the House and Senate.

On February 11, 2020, the state Senate voted 38-2 to pass the constitutional amendment, with two Democrats dissenting. On March 5, 2020, the state House voted 54-46 to pass SJR 18, with Republicans and nine Democrats in support and 46 Democrats opposed. This vote sent the redistricting reform measure to the voters as a constitutional amendment proposal for the 2020 ballot.

Amending the Constitution: What's Required?

You may want to see also

Explore related products

![]()

Property tax exemption for certain veterans

The proposed Virginia Constitutional Amendment Question 2, also known as the "Remove Restriction on Residence for Surviving Spouse of Disabled Veteran Tax Exemption Amendment", seeks to address property tax exemptions for certain veterans and their surviving spouses. This amendment was on the ballot in Virginia as a legislatively referred constitutional amendment on November 6, 2018, and was approved.

The amendment aims to provide property tax relief to a specific group of veterans and their spouses. In the context of this amendment, "certain veterans" typically refers to disabled veterans or those who have been killed in action. The amendment proposes to remove the restriction that requires the surviving spouse to continue residing in the place of residence of their deceased spouse to claim a property tax exemption. This means that if the amendment is approved, the surviving spouse of a disabled veteran or one killed in action would be able to receive the property tax exemption even if they choose to move to a new principal place of residence.

Currently, the Virginia Constitution mandates the taxation of all property, but it also specifies certain types of property that may be exempt from taxation. The proposed amendment seeks to expand the existing tax exemptions to include not only the surviving spouses of soldiers killed in action but also those who died while performing their duty. This expansion ensures that a broader range of surviving spouses can benefit from the tax exemption on their primary residence.

The Virginia Constitution, in its current form, allows the General Assembly to grant tax exemptions for the principal residence of surviving spouses of soldiers who, according to the U.S. Department of Defense, were killed in action. By extending this exemption to include soldiers who died in the line of duty, the amendment ensures that surviving spouses of soldiers who passed away while serving their country, regardless of the specific circumstances, can benefit from this tax relief.

A "yes" vote on this amendment would enable the surviving spouse of a soldier who died while performing their duty to claim the same property tax exemption on their principal residence that is currently exclusive to the surviving spouses of soldiers killed in action. Conversely, a "no" vote would maintain the existing restrictions, preventing additional surviving spouses from claiming the property tax exemption.

Who Proposes Amendments to Iowa's Constitution?

You may want to see also

Explore related products

![]()

Virginia Constitution and taxation laws

The Virginia Constitution, first enacted in 1776, has been amended 15 times since 2006. The most recent amendment, approved on November 5, 2024, concerned taxation laws.

Virginia's Taxation and Finance Laws

Article X of the Virginia Constitution, consisting of eleven sections, establishes the basic structure for taxation of personal property in the state. It outlines that all non-exempt real and personal property is subject to taxation at its fair market value. Real estate, coal and other mineral lands, and tangible personal property are subject to local taxation and shall be assessed for taxation as prescribed by the General Assembly.

The General Assembly has the authority to exempt certain types of property from taxation. For example, the Constitution allows the General Assembly to exempt from taxation the principal place of residence of a surviving spouse of a soldier killed in action, as determined by the U.S. Department of Defense.

Proposed Constitutional Amendment Question 2

The proposed Constitutional Amendment Question 2, to be voted on in the November 2024 elections, seeks to expand the current tax exemption for surviving spouses of soldiers. Currently, only the surviving spouses of soldiers killed in action are eligible for the tax exemption. The amendment proposes to extend this exemption to the surviving spouses of all soldiers who died in the line of duty, as determined by the U.S. Department of Defense.

This amendment would ensure that the surviving spouses of soldiers who died while serving their country, regardless of the specific circumstances, would receive the same tax benefits.

Amending the Constitution: Founding Fathers' Vision

You may want to see also

Frequently asked questions

Rep. Jason S. Miyares (R-82) proposed Virginia Constitutional Amendment Question 2 in 2018.

Virginia Constitutional Amendment Question 2 in 2018 was the "Remove Restriction on Residence for Surviving Spouse of Disabled Veteran Tax Exemption Amendment".

The amendment was approved.