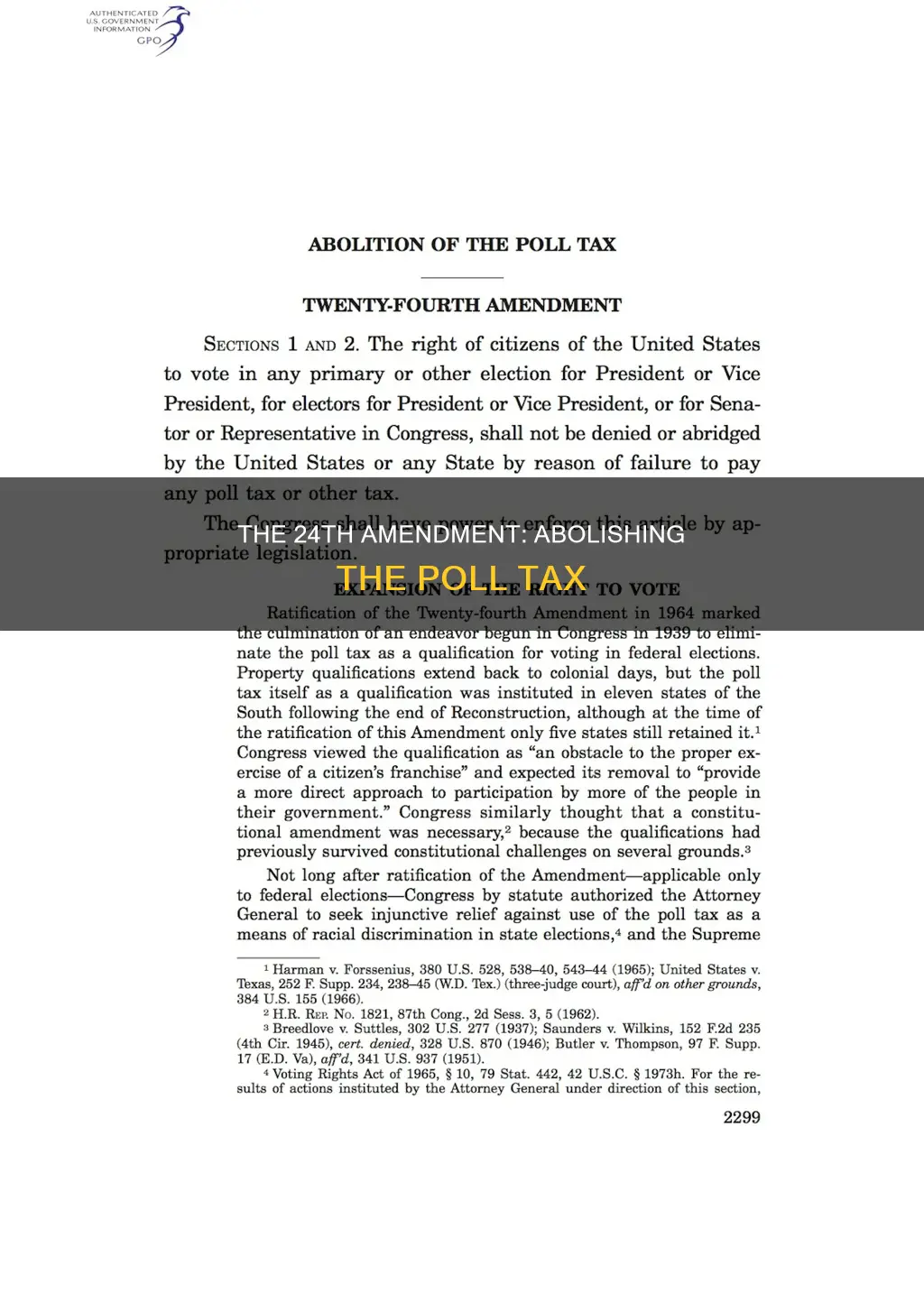

The Twenty-Fourth Amendment to the US Constitution, ratified on January 23, 1964, abolished poll taxes as a requirement for voting in federal elections. The amendment was proposed by Congress to the states on August 27, 1962, and was a significant step in the pursuit of civil rights during the turbulent 1960s. Poll taxes, which required voters to pay a fee to enter polling places and cast their ballots, had been used as a discriminatory tool to restrict the voting rights of African Americans and poor whites in the South. The ratification of the Twenty-Fourth Amendment marked the culmination of a Congressional effort that began in 1939 to eliminate poll taxes as a voting qualification.

| Characteristics | Values |

|---|---|

| Name of the Amendment | Twenty-fourth Amendment (Amendment XXIV) |

| Date of Ratification | 23 January 1964 |

| What it Abolished | Poll tax |

| What the Poll Tax was | A fee voters had to pay to enter polling places to cast their ballots |

| Who it Affected | Poor people, especially African Americans and poor whites |

| Who Proposed it | Congress |

| Who it Applied to | Federal elections |

| What it Changed | The landscape of voting rights in America |

| What it Prohibits | Federal and state governments from imposing taxes on voters during federal elections |

| What it Grants Congress | The power to enforce the amendment by appropriate legislation |

| Landmark Cases | Breedlove v. Suttles (1937), Harman v. Forssenius (1965), Harper v. Virginia Board of Elections (1966) |

Explore related products

![Historic Framed Print, [Vote bill trying to clear the Poll Tax amendment].Gib Crockett., 17-7/8" x 21-7/8"](https://m.media-amazon.com/images/I/4189W1OGGaL._AC_UY218_.jpg)

What You'll Learn

![]()

The Twenty-Fourth Amendment

> The right of citizens of the United States to vote in any primary or other election for President or Vice President, for electors for President or Vice President, or for Senator or Representative in Congress, shall not be denied or abridged by the United States or any State by reason of failure to pay poll tax or other tax. The Congress shall have power to enforce this article by appropriate legislation.

The amendment was proposed by Congress to the states on August 27, 1962, and was a significant step towards civil rights in the turbulent 1960s. It was passed the same year as the Civil Rights Act, which ended legal segregation in the US, and a year after the Voting Rights Act of 1965, which made voting a constitutional right for all American men and women for the first time.

Amendments Expanding Voting Rights: A Historical Overview

You may want to see also

Explore related products

![]()

Poll tax history

The poll tax in the United States was a fee that voters were required to pay to participate in elections. It was primarily prevalent in southern states after the Civil War. Initially intended as a means for states to generate revenue, these taxes became a significant barrier to voting, particularly for poor citizens, including many African Americans.

The implementation of poll taxes often coincided with Jim Crow laws, further reinforcing racial discrimination in voting practices. Despite the Fifteenth Amendment granting the right to vote to all male American citizens in 1870, many African Americans were disenfranchised due to their inability to afford the poll tax. The tax emerged in some states in the late nineteenth century and was used alone or together with a literacy qualification. In a kind of grandfather clause, North Carolina in 1900 exempted men entitled to vote as of January 1, 1867, from the poll tax. This excluded all black men, who did not have suffrage at that time.

The legality of poll taxes was upheld by the Supreme Court in several early cases, including the 1937 case of Breedlove v. Suttles, which held that poll taxes were constitutional. However, the situation began to change with the passage of the Twenty-Fourth Amendment in 1964, which abolished the use of poll taxes in federal elections. The official text of the amendment states:

> The right of citizens of the United States to vote in any primary or other election for President or Vice President, for electors for President or Vice President, or for Senator or Representative in Congress, shall not be denied or abridged by the United States or any State by reason of failure to pay a poll tax or other tax.

The Voting Rights Act of 1965 further contributed to the outlawing of poll taxes nationwide, and made it enforceable by law. Finally, in 1966, the Supreme Court ruled in Harper v. Virginia Board of Electors that under the Fourteenth Amendment, states could not levy a poll tax as a prerequisite for voting in state and local elections. This completely eliminated poll taxes in all elections – federal, state, and local.

How Judicial Interpretation Impacts the Constitution

You may want to see also

Explore related products

![]()

The Voting Rights Act of 1965

The Act was designed to secure the right to vote for racial minorities, particularly in the South, where African Americans faced significant obstacles to voting, including poll taxes, literacy tests, and other bureaucratic restrictions. These discriminatory voting practices had been adopted in many Southern states after the Civil War, and African Americans who tried to register or vote also risked harassment, intimidation, economic reprisals, and physical violence.

The Act gave the U.S. Attorney General the authority to pursue injunctive relief and challenge the use of poll taxes in state and local elections, which were deemed unconstitutional by the Supreme Court in Harper v. Virginia Board of Elections in 1966.

The Right to Vote: Constitutional Amendments

You may want to see also

Explore related products

![]()

Supreme Court decisions

The 24th Amendment to the US Constitution, ratified in 1964, abolished the use of the poll tax as a prerequisite for voting in federal elections. However, it did not address poll taxes in state elections. The Voting Rights Act of 1965 further clarified and enforced the abolition of poll taxes nationwide.

In the 1937 case of Breedlove v. Suttles, the US Supreme Court had upheld the constitutionality of poll taxes. However, in 1966, the Supreme Court reversed this decision in Harper v. Virginia State Board of Elections. The Court ruled that poll taxes in all elections, including state and local elections, were unconstitutional, as they violated the Equal Protection Clause of the 14th Amendment.

The Harper ruling was a significant milestone in the civil rights movement of the 1960s. It was celebrated as a victory for voting rights, particularly for poor African Americans and whites who had been disenfranchised due to poll taxes. The ruling emphasised that "fee payments or wealth, like race, creed, or colour, are unrelated to the citizen's ability to participate intelligently in the electoral process".

In the same year, the Supreme Court also decided Harman v. Forssenius, which involved a Virginia law that required residents to file a certificate of residence to vote in federal elections. The Court unanimously found this arrangement unconstitutional, stating that for federal elections, "the poll tax is abolished absolutely as a prerequisite to voting, and no equivalent or milder substitute may be imposed".

These Supreme Court decisions played a crucial role in eliminating poll taxes as a barrier to voting and advancing voting rights in the United States.

The Evolution of New Jersey's Constitution

You may want to see also

Explore related products

![]()

The Fifteenth Amendment

The poll tax was ruled constitutional by the Supreme Court in 1937 in the case of Breedlove v. Suttles. This decision was upheld in the 1946 case of Harman v. Forssenius, where the Court found that the poll tax was not a violation of constitutional rights. However, the tide began to turn against the poll tax during the Roosevelt Administration of the 1930s and 1940s, with President Franklin D. Roosevelt speaking out against it.

Despite the initial setbacks, Congress continued its efforts to abolish the poll tax. This culminated in the proposal of the Twenty-fourth Amendment, which was ratified on January 23, 1964. The amendment abolished poll taxes in federal elections and prohibited both Congress and the states from requiring their payment as a condition for voting. This marked a significant step forward in voting rights, as it ensured that financial status would not be a barrier to participation in federal elections.

While the Twenty-fourth Amendment abolished poll taxes in federal elections, it did not extend to state and local elections. This gap was addressed by the Voting Rights Act of 1965, which gave the Attorney General the authority to challenge the use of poll taxes in state and local elections. The Act enforced the Fifteenth Amendment's guarantee of voting without racial discrimination and required "covered jurisdictions," mainly in Southern states, to obtain pre-clearance before enacting any new voting rights legislation.

In summary, while the Fifteenth Amendment granted universal male suffrage in theory, it was not fully realized for African Americans due to discriminatory practices like the poll tax. The Twenty-fourth Amendment and the Voting Rights Act of 1965 played crucial roles in dismantling these barriers, ensuring that voting rights were protected regardless of race or economic status.

The Constitution's Fiscal Amendments: What's Guaranteed?

You may want to see also

Frequently asked questions

The Twenty-fourth Amendment (Amendment XXIV) of the United States Constitution abolished the poll tax.

The Twenty-fourth Amendment was ratified on January 23, 1964.

The Twenty-fourth Amendment prohibits both Congress and the states from requiring the payment of a poll tax or any other tax to vote in federal elections.