The question of which political party taxed Social Security has been a contentious issue in American politics, with both major parties, Democrats and Republicans, playing roles in shaping the taxation of these benefits. Initially, Social Security benefits were tax-free, but in 1983, under President Ronald Reagan, a Republican, and with bipartisan support from Congress, legislation was passed to allow a portion of Social Security benefits to be subject to federal income tax for higher-income recipients. This change was part of a broader effort to address Social Security’s solvency. Later, in 1993, during the Clinton administration, a Democrat, further changes were made to increase the share of benefits subject to taxation, again targeting higher-income individuals. While both parties have contributed to the taxation of Social Security, the issue remains a point of debate, with critics arguing it affects retirees’ financial planning and supporters defending it as a means to ensure the program’s long-term sustainability.

Explore related products

What You'll Learn

![]()

Historical Context of Social Security Taxation

The taxation of Social Security benefits began in 1983 under the Reagan administration, a bipartisan effort to address the program's solvency crisis. The Amendments to the Social Security Act, signed into law by President Ronald Reagan, introduced a provision allowing up to 50% of Social Security benefits to be subject to federal income tax for individuals earning above certain thresholds. This change was part of a broader package of reforms aimed at ensuring the long-term viability of the program, which was projected to face significant funding shortfalls. The bipartisan nature of this reform is notable, as both Democratic and Republican leaders supported the measure, reflecting a rare moment of cross-party cooperation in addressing a critical fiscal issue.

In 1993, the Clinton administration expanded the taxation of Social Security benefits, increasing the proportion of benefits subject to tax from 50% to 85% for higher-income recipients. This change was part of the Omnibus Budget Reconciliation Act, which sought to reduce the federal deficit. The rationale behind this expansion was to ensure that wealthier beneficiaries contributed more to the program's sustainability, aligning with a progressive tax philosophy. Critics argued that this move effectively raised taxes on retirees, but proponents emphasized its role in shoring up Social Security's finances. This reform underscores the evolving role of Social Security taxation as a tool for both fiscal responsibility and income redistribution.

The historical context of Social Security taxation reveals a pattern of incremental adjustments rather than sweeping changes. Both the 1983 and 1993 reforms were implemented during periods of fiscal concern, highlighting the program's sensitivity to broader economic conditions. Importantly, these changes were not driven by a single political party but rather by bipartisan or cross-party agreements, reflecting a shared commitment to preserving Social Security. However, the increasing reliance on benefit taxation has sparked debates about the program's original intent as a universal safety net, with some arguing that taxing benefits undermines its foundational principles.

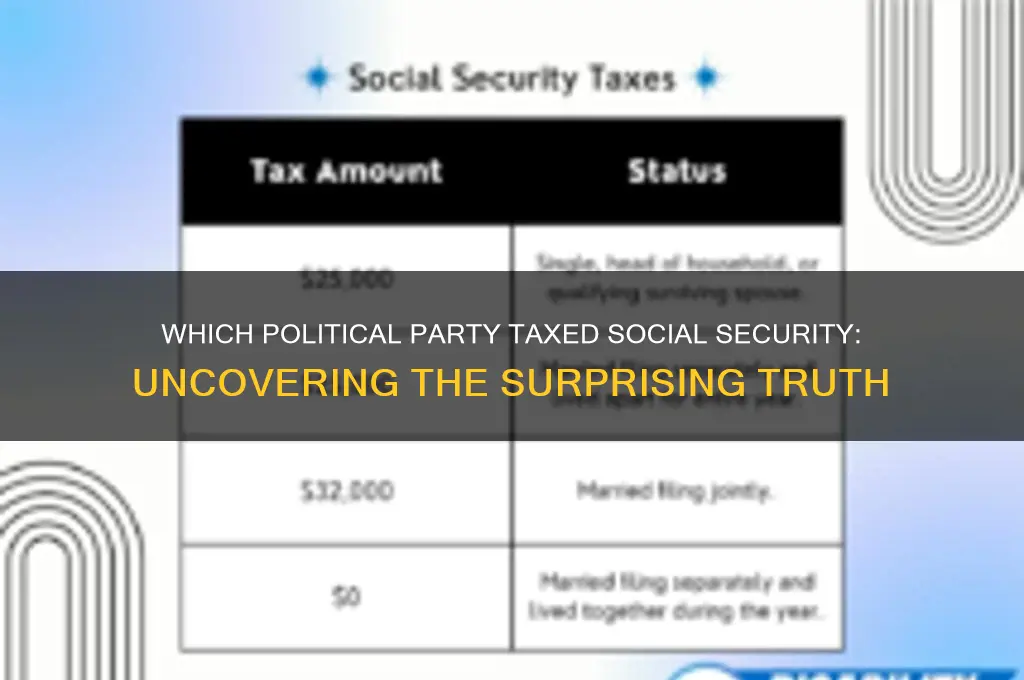

Practical implications of these reforms are still felt today, as millions of retirees face federal income tax on their Social Security benefits. For example, in 2023, individuals with combined income (adjusted gross income plus nontaxable interest plus half of Social Security benefits) exceeding $25,000 ($32,000 for married couples filing jointly) may have up to 50% of their benefits taxed, while those above $34,000 ($44,000 for couples) may see up to 85% taxed. Retirees can mitigate this impact by strategically managing their income sources, such as delaying withdrawals from taxable accounts or utilizing Roth IRAs, which do not count toward the combined income threshold. Understanding these rules is essential for effective retirement planning, as they directly affect post-retirement cash flow.

In conclusion, the historical context of Social Security taxation illustrates a pragmatic approach to addressing fiscal challenges, marked by bipartisan cooperation and incremental reforms. While these changes have bolstered the program's finances, they have also raised questions about equity and the program's core purpose. For retirees, navigating the complexities of benefit taxation requires proactive financial planning, underscoring the enduring relevance of these historical decisions in contemporary retirement strategies.

Ideology vs. Party: Understanding the Core Differences in Politics

You may want to see also

Explore related products

![]()

Democratic Party’s Role in Social Security Taxes

The Democratic Party has played a pivotal role in shaping the taxation of Social Security, often positioning itself as a defender of the program while navigating complex fiscal realities. One key example is the 1983 Social Security Amendments, signed into law by President Ronald Reagan but crafted through bipartisan efforts, including significant Democratic input. These amendments raised payroll taxes and gradually increased the full retirement age to ensure the program's solvency. Democrats supported these changes, arguing they were necessary to protect Social Security for future generations, even though they involved higher taxes on workers.

Analyzing the Democratic stance reveals a consistent theme: balancing fiscal responsibility with a commitment to social welfare. During the Obama administration, for instance, Democrats resisted calls to privatize Social Security or reduce benefits, instead advocating for targeted tax increases on higher earners. The Affordable Care Act included a provision to raise the Medicare payroll tax for individuals earning over $200,000 and couples earning over $250,000, indirectly affecting Social Security funding by bolstering the overall fiscal health of entitlement programs. This approach reflects the party's strategy of addressing funding gaps through progressive taxation rather than benefit cuts.

A comparative perspective highlights the contrast between Democratic and Republican approaches. While Republicans often propose reducing payroll taxes or capping benefits, Democrats have historically prioritized maintaining or expanding Social Security's funding base. For example, during the 2020 presidential campaign, Democratic candidates uniformly opposed cutting Social Security taxes, instead proposing to lift the payroll tax cap, which currently exempts earnings above $168,600 (as of 2023). This would require higher-income individuals to pay more into the system, a policy Democrats argue is fair and sustainable.

Practical implications of Democratic policies on Social Security taxation are worth noting. For workers, the party's stance means a continued reliance on payroll taxes as the primary funding mechanism, with potential increases for higher earners. Retirees benefit from the party's commitment to preserving benefits, though they may face indirect impacts if tax changes affect economic growth. To navigate these policies, individuals should stay informed about proposed changes, such as the potential lifting of the payroll tax cap, and plan their finances accordingly. For instance, those nearing retirement might consider consulting a financial advisor to understand how tax adjustments could impact their Social Security benefits.

In conclusion, the Democratic Party's role in Social Security taxation is characterized by a commitment to progressive funding solutions and benefit preservation. While this approach has ensured the program's stability, it also places a continued burden on workers, particularly higher earners. As debates over Social Security's future persist, understanding the Democrats' stance provides critical insight into the program's likely trajectory and the trade-offs involved in maintaining this cornerstone of American social welfare.

The Rise of Political Bosses and Their Corrupt Practices

You may want to see also

Explore related products

![]()

Republican Party’s Stance on Social Security Taxation

The Republican Party's stance on Social Security taxation is rooted in a commitment to fiscal responsibility and a belief in minimizing government intervention in personal finances. Historically, Republicans have supported measures that reduce taxes on Social Security benefits, arguing that retirees should keep more of their hard-earned money. For instance, during the Reagan administration, the 1983 Social Security Amendments included provisions to limit the taxation of benefits, reflecting a broader GOP philosophy of lower taxes. However, this stance has evolved over time, with some Republicans advocating for reforms that could indirectly affect Social Security taxation, such as means-testing benefits or raising the retirement age, which could reduce overall payouts and, by extension, taxable benefits.

Analyzing the GOP’s approach reveals a tension between their tax-cutting ethos and the need to ensure Social Security’s solvency. While Republicans often oppose increasing taxes on higher-income earners, they have also proposed changes that could shift the tax burden on benefits. For example, the 1993 budget reconciliation bill, signed by President Clinton but supported by some Republicans, introduced taxation on up to 85% of Social Security benefits for higher-income individuals. This move, though not initiated by the GOP, has since become a point of contention, with some Republicans arguing it undermines their goal of reducing taxes on retirees. This duality highlights the party’s challenge in balancing fiscal conservatism with the program’s long-term viability.

From a practical standpoint, understanding the Republican stance on Social Security taxation requires examining their legislative priorities. GOP proposals often focus on protecting lower- and middle-income retirees from benefit taxation while targeting higher earners for reforms. For instance, some Republicans have suggested exempting beneficiaries below certain income thresholds from taxation altogether. Conversely, they have also floated ideas like applying a flat tax rate to benefits, which could simplify the system but potentially increase taxes for some retirees. These proposals underscore the party’s emphasis on fairness and efficiency, though they often face criticism for disproportionately impacting wealthier retirees.

Comparatively, the Republican approach contrasts sharply with Democratic policies, which typically aim to expand Social Security benefits and fund the program through higher taxes on top earners. While Democrats advocate for increasing payroll taxes or lifting the wage cap, Republicans generally resist such measures, arguing they would harm economic growth. Instead, the GOP favors reforms like encouraging private savings or adjusting the cost-of-living calculation to reduce program costs. This comparative perspective highlights the ideological divide over Social Security taxation, with Republicans prioritizing tax relief and structural reforms over revenue increases.

In conclusion, the Republican Party’s stance on Social Security taxation is characterized by a desire to minimize taxes on retirees while ensuring the program’s sustainability. Their historical and current proposals reflect a commitment to fiscal conservatism, though they often grapple with trade-offs between tax cuts and program solvency. For retirees and policymakers alike, understanding this stance is crucial for navigating the complexities of Social Security taxation and its implications for future generations.

Exploring Diverse Career Paths: Who Employs Political Scientists Today?

You may want to see also

Explore related products

$14.21 $17.99

![]()

Key Legislation Affecting Social Security Taxes

The Social Security Amendments of 1983 marked a pivotal shift in how Social Security taxes were structured, introducing changes that still resonate today. Signed into law under President Ronald Reagan, a Republican, this bipartisan legislation addressed the program’s solvency crisis by gradually increasing the payroll tax rate, raising the retirement age, and, notably, taxing a portion of Social Security benefits for higher-income recipients. This move, though controversial, demonstrated a willingness to reform the system to ensure its long-term viability. The amendments also indexed benefits to inflation, providing a safety net for beneficiaries against rising costs of living. While both parties supported the bill, its implementation underscored the complexity of balancing fiscal responsibility with social welfare.

Another critical piece of legislation was the Tax Equity and Fiscal Responsibility Act (TEFRA) of 1982, enacted under President Reagan’s administration. This act expanded the taxation of Social Security benefits, applying federal income tax to up to 50% of benefits for individuals earning above certain thresholds. Though TEFRA was primarily a tax reform bill, its impact on Social Security taxation was significant, as it marked the first time benefits were subject to federal income tax. This change disproportionately affected higher-income retirees, sparking debates about the fairness of taxing a program funded by payroll taxes. TEFRA’s legacy lies in its role as a precursor to further benefit taxation, setting a precedent for using Social Security as a revenue source.

The Budget Reconciliation Act of 1993, signed by President Bill Clinton, a Democrat, further expanded the taxation of Social Security benefits. This legislation increased the portion of benefits subject to federal income tax from 50% to 85% for higher-income individuals and couples. The act aimed to reduce the federal deficit by targeting wealthier beneficiaries, a move that aligned with Clinton’s focus on fiscal responsibility. Critics argued that this change eroded the universality of Social Security, as it effectively reduced net benefits for a subset of recipients. However, proponents viewed it as a necessary measure to ensure the program’s sustainability in the face of demographic and economic challenges.

Comparing these legislative actions reveals a pattern: both Republican and Democratic administrations have taxed Social Security benefits, albeit with different rationales and impacts. While the 1983 amendments were part of a broader solvency package, TEFRA and the 1993 act focused on generating revenue to address budget deficits. This evolution highlights the dual role of Social Security as both a safety net and a fiscal tool. For individuals, understanding these changes is crucial for retirement planning, as benefit taxation can significantly affect post-retirement income. Practical tips include estimating taxable benefit amounts using IRS worksheets and considering strategies like Roth IRA conversions to minimize tax exposure. Ultimately, the history of Social Security taxation underscores the program’s adaptability and the ongoing tension between equity and fiscal pragmatism.

Exploring Michigan's Political Landscape: Which Party Dominates the State?

You may want to see also

Explore related products

![]()

Impact of Social Security Taxation on Voters

The taxation of Social Security benefits, implemented under the Reagan administration in 1983 with bipartisan support, has had a profound and multifaceted impact on voters. Initially, only 50% of Social Security benefits were subject to federal income tax for individuals earning over $25,000 or couples over $32,000. However, in 1993, under President Clinton, the taxable portion increased to 85% for higher-income recipients. This shift disproportionately affected seniors in the upper brackets, many of whom had planned their retirements without anticipating such taxation. The result? A growing sense of financial insecurity among older voters, who now face higher tax liabilities on what was once considered untaxed income.

Analyzing voter behavior reveals that Social Security taxation has become a wedge issue, particularly among older demographics. For instance, seniors in states like Florida and Arizona, where retirees are a significant voting bloc, have increasingly scrutinized candidates’ stances on this issue. A 2020 AARP survey found that 77% of voters aged 50+ considered Social Security a top priority when casting their ballots. Candidates who propose reducing or eliminating Social Security taxation often gain traction with these voters, while those perceived as indifferent or supportive of such taxes risk alienating this critical group. This dynamic has forced politicians to tread carefully, balancing fiscal responsibility with the political cost of upsetting retirees.

From a practical standpoint, voters must understand how Social Security taxation affects their bottom line. For example, a retired couple with a combined income of $60,000 may see up to 85% of their Social Security benefits taxed, reducing their net income significantly. To mitigate this, retirees can employ strategies like delaying Social Security claims, diversifying income sources (e.g., Roth IRAs, which aren’t taxed in retirement), or relocating to one of the 37 states that don’t tax Social Security benefits. However, these solutions aren’t feasible for everyone, leaving many voters feeling trapped by a system they perceive as punitive.

Comparatively, the impact of Social Security taxation on younger voters is less direct but no less significant. Millennials and Gen Z, already skeptical of Social Security’s solvency, view its taxation as another example of an unfair burden shifted onto future generations. This sentiment has fueled support for candidates advocating for systemic reforms, such as raising the payroll tax cap or investing Social Security funds in higher-yield assets. While younger voters may not feel the immediate sting of Social Security taxation, their long-term financial planning and political allegiances are undeniably shaped by it.

In conclusion, the taxation of Social Security benefits has become a litmus test for voter trust in government fiscal policies. Older voters, hit hardest by these taxes, demand relief and accountability, while younger generations seek systemic change to ensure the program’s viability. Politicians who fail to address this issue risk alienating a broad spectrum of voters, making Social Security taxation a pivotal yet often overlooked factor in electoral outcomes. Understanding its impact is essential for both voters navigating retirement and candidates seeking to earn their trust.

Whig Party's Collapse: Key Political Challenges and Internal Struggles

You may want to see also

Frequently asked questions

Both the Democratic and Republican parties have been involved in taxing Social Security benefits, with the initial taxation implemented under President Franklin D. Roosevelt (Democrat) in 1937, though the specific taxation of benefits as income began in 1983 under President Ronald Reagan (Republican).

The taxation of Social Security benefits as income began under President Ronald Reagan, a Republican, in 1983 as part of the Amendments to the Social Security Act.

Both parties have contributed to increases in Social Security taxation. In 1993, under President Bill Clinton (Democrat), the threshold for taxing benefits was lowered, affecting more beneficiaries.

Both parties have played roles in taxing Social Security, but the initial framework for taxing benefits was established under a Republican administration (Reagan), while Democrats (Clinton) expanded the scope of taxation.

Both parties have proposed various plans to reduce or eliminate taxes on Social Security benefits, but no major legislation has been passed to completely remove these taxes as of now. Some politicians from both parties have advocated for changes, but it remains a debated issue.