The practice of redlining, a discriminatory policy that denied services or increased the cost of services such as banking, insurance, access to healthcare, or even supermarkets to residents in minority and low-income neighborhoods, has its roots in the early 20th century. While redlining was not directly initiated by a single political party, its institutionalization is closely tied to policies and programs established during the New Deal era under President Franklin D. Roosevelt’s administration, which was led by the Democratic Party. Specifically, the Home Owners' Loan Corporation (HOLC), a federal agency created in 1933, played a pivotal role in codifying redlining by creating residential security maps that graded neighborhoods based on perceived risk, often correlating race with financial risk. These maps effectively segregated communities and denied African Americans and other minorities access to fair housing and lending opportunities, laying the groundwork for decades of systemic racial and economic inequality.

Explore related products

What You'll Learn

- Origins of Redlining: New Deal policies and the Home Owners' Loan Corporation's role in segregating neighborhoods

- Democratic Party Involvement: Franklin D. Roosevelt's administration and the implementation of discriminatory housing practices

- Republican Party Stance: Historical Republican policies and their impact on housing segregation and redlining

- Federal Housing Administration (FHA): FHA's use of racial covenants and redlining maps to deny loans

- Local Government Participation: How city and state governments enforced redlining through zoning laws and regulations

![]()

Origins of Redlining: New Deal policies and the Home Owners' Loan Corporation's role in segregating neighborhoods

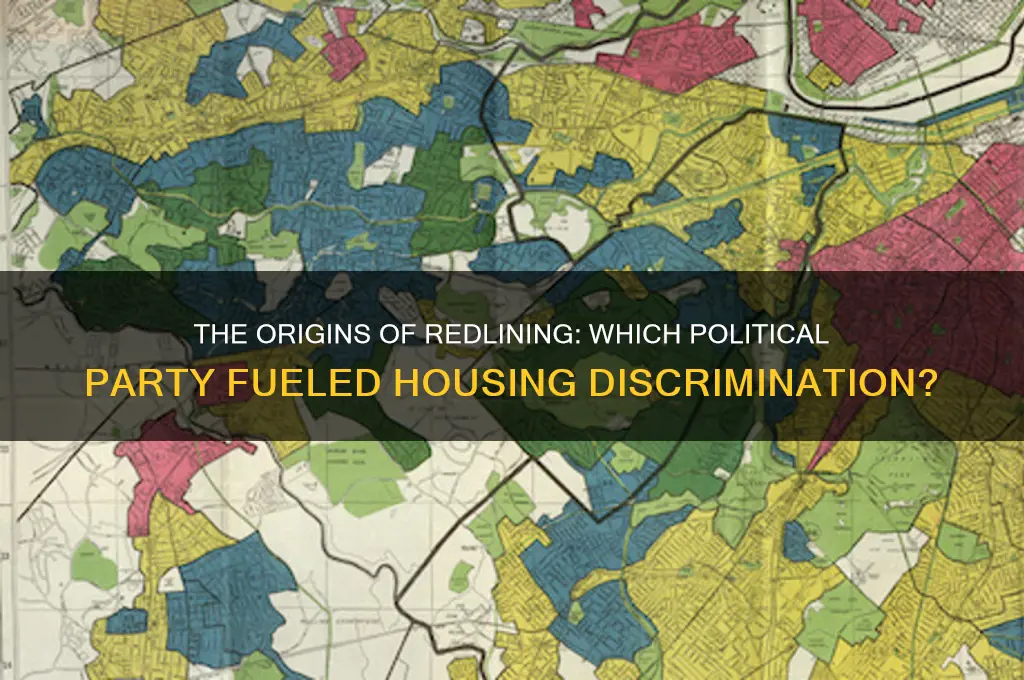

The roots of redlining trace back to the 1930s, when the Home Owners Loan Corporation (HOLC), a New Deal agency, introduced color-coded maps to assess mortgage risk. These maps, ostensibly designed to stabilize the housing market during the Great Depression, inadvertently institutionalized racial segregation. Neighborhoods with significant African American populations were outlined in red, deemed "hazardous" for investment, effectively cutting off residents from home loans and economic opportunity. This federal policy, though not explicitly racist in its language, codified and perpetuated racial disparities in housing that persist to this day.

To understand HOLC’s role, consider its methodology. Appraisers evaluated neighborhoods based on criteria like property values, infrastructure, and the racial composition of residents. Areas with Black residents, regardless of their actual economic health, were systematically downgraded. For instance, a thriving Black neighborhood might be labeled "risky" simply because of its demographics, while a struggling white neighborhood could receive a higher rating. This biased system not only denied Black families access to homeownership but also devalued their communities, creating a self-fulfilling prophecy of decline.

The HOLC’s actions were not isolated; they were part of a broader New Deal framework that often excluded or marginalized Black Americans. While programs like the Federal Housing Administration (FHA) aimed to boost homeownership, they explicitly favored white borrowers. The FHA’s underwriting manual, for example, warned against loans in racially mixed neighborhoods, effectively endorsing segregation. This duality—New Deal policies providing relief to some while entrenching inequality for others—highlights the complex legacy of these initiatives.

A critical takeaway is that redlining was not merely a private sector practice but a government-sanctioned policy. The HOLC’s maps became the blueprint for decades of discriminatory lending, shaping the racial and economic contours of American cities. Today, neighborhoods once redlined often remain underserved, with lower property values, fewer amenities, and limited access to credit. Recognizing this history is essential for addressing contemporary housing inequities, as the effects of these policies are still felt generations later.

To combat the ongoing impact of redlining, policymakers and advocates must focus on targeted interventions. Programs like community land trusts, affordable housing initiatives, and reparations-focused policies can begin to reverse the damage. Additionally, educating the public about this history fosters accountability and encourages systemic change. While the origins of redlining lie in the New Deal era, its dismantling requires a concerted effort in the present, informed by a clear understanding of its roots.

Explaining Political Parties to Kids: A Simple Guide for Families

You may want to see also

Explore related products

![]()

Democratic Party Involvement: Franklin D. Roosevelt's administration and the implementation of discriminatory housing practices

The roots of redlining trace back to the 1930s, when Franklin D. Roosevelt’s administration, under the banner of the Democratic Party, implemented policies that institutionalized racial discrimination in housing. The Home Owners’ Loan Corporation (HOLC), established in 1933 as part of the New Deal, created color-coded maps to assess mortgage risk in urban areas. Neighborhoods with significant African American populations were outlined in red, deemed “hazardous” for investment, and effectively cut off from federal housing loans. This practice, though not explicitly race-based in legislation, was underpinned by racist assumptions and had devastating long-term consequences for minority communities.

Analyzing the HOLC’s methodology reveals its discriminatory intent. Appraisers considered factors like the racial composition of neighborhoods, often labeling areas with Black residents as undesirable, regardless of their economic stability. This systemic bias was further entrenched by the Federal Housing Administration (FHA), which adopted HOLC’s guidelines to insure mortgages. By refusing to back loans in redlined areas, the FHA effectively segregated housing markets, funneling investment into white neighborhoods while denying opportunities to communities of color. This government-sanctioned discrimination laid the groundwork for decades of wealth inequality and urban decay.

A persuasive argument can be made that Roosevelt’s administration, while celebrated for its economic reforms, perpetuated racial inequality through these policies. The New Deal’s housing programs were designed to stabilize the economy and boost homeownership, but they did so at the expense of marginalized groups. For instance, the FHA’s underwriting manual explicitly warned against lending in racially mixed neighborhoods, codifying segregation into federal policy. This exclusionary approach not only denied Black families access to homeownership but also devalued their communities, creating a cycle of poverty that persists to this day.

Comparing the Democratic Party’s role in redlining to other historical contexts highlights its significance. While both parties have contributed to systemic racism, the HOLC and FHA policies were direct creations of the Roosevelt administration, a Democratic stronghold. These institutions were not rogue entities but core components of the New Deal, reflecting the party’s priorities at the time. This contrasts with later Republican policies, which often exacerbated redlining’s effects through neglect rather than active implementation. Understanding this distinction is crucial for holding political parties accountable for their historical actions.

Practically, the legacy of Roosevelt-era redlining continues to shape modern housing disparities. Redlined neighborhoods still face lower property values, limited access to credit, and inadequate public services. To address this, policymakers must prioritize targeted investments in historically marginalized communities, such as affordable housing initiatives and community development grants. Additionally, individuals can advocate for fair housing policies and support organizations working to dismantle systemic racism in real estate. By confronting this history, we can begin to undo the damage caused by these discriminatory practices.

Exploring Denmark's Diverse Political Landscape: Parties and Representation

You may want to see also

Explore related products

![]()

Republican Party Stance: Historical Republican policies and their impact on housing segregation and redlining

The roots of redlining trace back to the 1930s, when the Home Owners' Loan Corporation (HOLC), a federal agency, began mapping neighborhoods to assess mortgage risk. While the HOLC was established under President Franklin D. Roosevelt, a Democrat, the policies that enabled and perpetuated redlining were influenced by a broader political and economic context. Republicans, particularly during the mid-20th century, played a significant role in shaping housing policies that exacerbated segregation. Their emphasis on limited federal intervention and support for local control often aligned with practices that reinforced racial disparities in housing.

One critical example is the Republican stance during the post-World War II era, when the GI Bill provided housing benefits to returning veterans. While the bill itself was bipartisan, Republican lawmakers at the state and local levels often supported practices that excluded Black veterans from accessing these benefits. In many Southern and Midwestern states, where Republicans held significant influence, local real estate boards and banks systematically denied mortgages to Black families, effectively segregating neighborhoods. This de facto redlining was not solely a federal policy but was enabled by Republican-backed local policies that prioritized property values and racial homogeneity over equitable access to housing.

Analyzing the 1960s and 1970s reveals a more direct Republican resistance to federal efforts to combat redlining. When the Fair Housing Act of 1968 was passed, Republicans in Congress, while not uniformly opposed, often criticized the legislation as an overreach of federal power. This ideological stance translated into weak enforcement mechanisms, as Republican-appointed officials in agencies like the Department of Housing and Urban Development (HUD) were less likely to pursue aggressive anti-discrimination measures. For instance, during the Nixon administration, HUD under Secretary George Romney faced significant pushback from Republican lawmakers when attempting to implement policies that would desegregate suburban neighborhoods, effectively limiting the act’s impact.

A comparative analysis highlights the Republican Party’s role in perpetuating redlining through its support for deregulation and privatization in the housing market. In the 1980s, under President Ronald Reagan, Republicans championed policies that reduced federal oversight of lending practices, leading to the rise of predatory lending in minority communities. While not explicitly redlining, these policies created a system where Black and Brown families were disproportionately targeted with subprime loans, further entrenching economic and housing disparities. This approach contrasts sharply with Democratic efforts during the same period to strengthen fair housing laws, underscoring the Republican Party’s indirect but significant contribution to the legacy of redlining.

In conclusion, while redlining cannot be attributed solely to one political party, the Republican Party’s historical policies and ideological stances have played a pivotal role in shaping and sustaining housing segregation. From enabling local discriminatory practices to resisting federal anti-discrimination efforts, Republicans have consistently prioritized limited government intervention and property rights over equitable housing access. Understanding this history is crucial for addressing the ongoing impacts of redlining and crafting policies that promote housing justice today.

Southern Political Allegiance: Which Party Did the South Historically Support?

You may want to see also

Explore related products

$39.41 $54.99

$39.99 $39.99

![]()

Federal Housing Administration (FHA): FHA's use of racial covenants and redlining maps to deny loans

The Federal Housing Administration (FHA), established in 1934 under President Franklin D. Roosevelt’s New Deal, was designed to stimulate the housing market by providing government-backed loans. While its intent was to make homeownership accessible to middle-class Americans, the FHA institutionalized racial discrimination through its use of racial covenants and redlining maps. These tools effectively denied loans to Black and minority communities, shaping decades of housing inequality.

Racial covenants, legally binding agreements embedded in property deeds, explicitly prohibited the sale or rental of homes to non-white individuals. The FHA not only endorsed these covenants but also included them in its underwriting guidelines, ensuring they became a standard practice in the housing market. For example, FHA manuals from the 1930s advised against loans in neighborhoods with "inharmonious racial or nationality groups," codifying segregation into federal policy. This practice was not merely a reflection of societal prejudice but an active government-led effort to maintain racial homogeneity in white neighborhoods.

Simultaneously, the FHA employed redlining maps, developed by the Home Owners’ Loan Corporation (HOLC), to assess lending risk. These maps categorized neighborhoods by color, with red areas deemed "hazardous" for investment. Overwhelmingly, redlined areas were predominantly Black or minority neighborhoods, regardless of their actual economic stability. The FHA’s refusal to insure loans in these areas starved them of investment, leading to decay and devaluation. This systemic exclusion was not accidental but a deliberate policy choice, as the FHA’s own guidelines prioritized racial composition over financial viability.

The consequences of the FHA’s actions were profound and long-lasting. By denying Black families access to federally subsidized loans, the FHA effectively excluded them from the post-WWII housing boom, one of the largest wealth-building opportunities in American history. This disparity widened the racial wealth gap, as homeownership became a cornerstone of middle-class stability for whites while remaining out of reach for minorities. The legacy of redlining persists today, with formerly redlined neighborhoods often experiencing higher poverty rates, poorer infrastructure, and limited access to quality education and healthcare.

Understanding the FHA’s role in redlining is critical for addressing contemporary housing inequities. While the Fair Housing Act of 1968 outlawed racial covenants, the damage was already done. Modern efforts to rectify this history, such as community reinvestment programs and affordable housing initiatives, must confront the systemic roots of the problem. Policymakers and advocates can learn from this history by prioritizing equitable lending practices, investing in underserved neighborhoods, and dismantling the structural barriers that perpetuate racial segregation in housing. The FHA’s legacy serves as a stark reminder that government policies, not just private actions, have shaped the unequal housing landscape we see today.

Unveiling William Hurd's Political Party Affiliation: A Comprehensive Overview

You may want to see also

Explore related products

$24.99 $24.99

![]()

Local Government Participation: How city and state governments enforced redlining through zoning laws and regulations

Redlining, a practice rooted in the 1930s, was not merely a federal initiative but a localized enforcement mechanism that relied heavily on city and state governments. These local entities wielded zoning laws and regulations as tools to segregate communities, often under the guise of urban planning and economic development. By designating certain areas as "hazardous" for investment based on racial demographics, they effectively restricted access to housing and resources for minority groups, particularly African Americans. This systemic discrimination was not an accident but a deliberate policy, codified in ordinances that dictated where people could live, work, and thrive.

Consider the role of zoning maps, which were often drawn to exclude minority neighborhoods from desirable amenities like schools, parks, and commercial districts. For instance, in cities like Chicago and Detroit, zoning laws were used to create industrial buffers between white and Black neighborhoods, exposing the latter to pollution and economic disinvestment. These maps were not neutral documents; they reflected the racial biases of local officials who sought to maintain segregation. The enforcement of these laws was equally telling—minority residents faced fines, demolitions, or legal barriers when attempting to improve their properties, while white neighborhoods enjoyed leniency and incentives for development.

A closer examination of the legislative process reveals how local governments institutionalized redlining. City councils and planning commissions passed ordinances that restricted multi-family housing to specific zones, often correlating with minority-heavy areas. This effectively prevented upward mobility and integration, as single-family zoning in white neighborhoods became a protected status. Additionally, building codes and permit requirements were selectively enforced, making it prohibitively expensive for minority homeowners to renovate or expand their properties. These policies were not just about land use; they were about controlling the racial composition of neighborhoods.

The impact of these local policies was profound and long-lasting. By confining minority populations to under-resourced areas, cities and states ensured generational wealth gaps and limited access to quality education and healthcare. For example, in cities like Baltimore and St. Louis, redlined neighborhoods still struggle with disinvestment, while formerly white-only zones have seen significant appreciation in property values. This legacy underscores the importance of understanding local government’s role in perpetuating racial inequality, as federal policies alone cannot explain the depth and persistence of redlining’s effects.

To dismantle this legacy, modern local governments must take proactive steps. This includes revisiting zoning laws to eliminate exclusionary practices, investing in historically redlined neighborhoods, and creating affordable housing initiatives. Transparency in planning processes and community engagement are also critical, ensuring that residents have a say in the development of their neighborhoods. While the origins of redlining may be traced to federal policies, its enforcement and impact were deeply local—and so must be the solutions.

Understanding Ralph Northam's Political Party Affiliation in Virginia Politics

You may want to see also

Frequently asked questions

Redlining was not initiated by a single political party but was a practice institutionalized by the federal government under the Home Owners' Loan Corporation (HOLC) during the New Deal era in the 1930s, under President Franklin D. Roosevelt's administration, which was led by the Democratic Party.

While redlining was formalized under a Democratic administration, the practice of discriminatory lending and housing policies was supported by both political parties and private institutions, reflecting broader societal racism and segregationist policies of the time.

No, redlining was a systemic practice that transcended party lines. Both Democrats and Republicans, along with private banks and real estate entities, participated in or benefited from the discriminatory policies that led to redlining.

At the time redlining was institutionalized, neither major political party actively opposed it. It wasn’t until the civil rights movement and the passage of the Fair Housing Act in 1968, under a Democratic administration, that legal steps were taken to address the practice.