The question of which political party moved Social Security funds is a contentious and often misunderstood aspect of U.S. political history. While Social Security itself was established under Democratic President Franklin D. Roosevelt in 1935 as part of the New Deal, discussions about its funding and management have spanned decades and involved both major parties. One notable instance often cited is the 1983 Social Security Amendments, signed into law by Republican President Ronald Reagan, which included a bipartisan agreement to raise payroll taxes and gradually increase the retirement age to ensure the program's solvency. However, the idea that funds were moved typically refers to the practice of transferring Social Security surpluses into the general fund, a practice that has been utilized by both Democratic and Republican administrations to balance the federal budget. This issue highlights the complexity of Social Security's financial structure and the ongoing debate over its long-term sustainability.

Explore related products

What You'll Learn

- FDR's New Deal Legislation: Established Social Security, funded by payroll taxes, under Democratic administration

- Reagan's Surplus Shift: Moved Social Security surplus to unified budget, blending funds with general revenue

- Clinton's Budget Reform: Continued unified budget approach, maintaining Social Security surplus as part of general funds

- Bush Tax Cuts Impact: Reduced revenue, increasing reliance on Social Security surplus to balance budget

- Bipartisan Policy Legacy: Both parties supported unified budget, indirectly affecting Social Security fund allocation

![]()

FDR's New Deal Legislation: Established Social Security, funded by payroll taxes, under Democratic administration

Franklin D. Roosevelt’s New Deal legislation stands as a cornerstone of American social policy, particularly through its establishment of Social Security in 1935. This program, created under a Democratic administration, was designed to provide a safety net for the elderly, the unemployed, and the vulnerable during the Great Depression. Funded primarily through payroll taxes, Social Security represented a significant shift in federal responsibility for citizen welfare. Unlike previous welfare programs, it was not a temporary relief measure but a permanent fixture of the American social contract, reflecting the Democratic Party’s commitment to economic security and collective responsibility.

The funding mechanism for Social Security—payroll taxes—was a deliberate choice to ensure its sustainability and broad-based support. Workers and employers each contributed a portion of wages, creating a dedicated revenue stream that was separate from general federal funds. This structure was both innovative and strategic, as it tied the program’s success to the economic activity of the workforce. By avoiding reliance on general taxation, the Democratic administration insulated Social Security from partisan budget battles, though it also sparked debates about the fairness of taxing wages to fund benefits. This approach remains a defining feature of the program to this day, distinguishing it from other social welfare initiatives.

Critics and proponents alike have debated the implications of this funding model. On one hand, payroll taxes ensure a steady income for Social Security, making it less susceptible to political whims. On the other hand, they place a direct financial burden on workers and businesses, particularly those with lower incomes. The Democratic Party’s decision to fund Social Security in this manner reflects a belief in shared sacrifice for the common good, a principle that has both endured and evolved over the decades. For individuals, understanding this funding structure is crucial for planning retirement and advocating for policy changes that address its limitations.

Practical considerations for workers include understanding how payroll taxes affect take-home pay and future benefits. As of 2023, the Social Security tax rate is 6.2% for employees and employers, each, up to a wage base limit of $160,200. Self-employed individuals pay the full 12.4%. To maximize benefits, workers should ensure accurate wage reporting and consider delaying benefits until full retirement age or later, as this increases monthly payments. Additionally, staying informed about legislative proposals to reform Social Security—such as adjusting the payroll tax rate or raising the wage cap—can empower individuals to engage in meaningful advocacy.

In the broader context of the question, “which political party moved social security funds,” the Democratic Party’s role in establishing and funding Social Security through payroll taxes is undeniable. While no party has “moved” funds in the sense of redirecting them to unrelated purposes, debates over Social Security’s solvency and structure have often highlighted partisan differences. The Democratic approach, rooted in FDR’s New Deal, emphasizes maintaining the program’s integrity and expanding its reach, whereas Republican proposals have occasionally focused on privatization or reducing its scope. For those navigating this complex landscape, recognizing the historical and ideological underpinnings of Social Security is essential to understanding current policy debates and their potential impact on future generations.

Which Party Backed the Kansas-Nebraska Act? A Historical Analysis

You may want to see also

Explore related products

![]()

Reagan's Surplus Shift: Moved Social Security surplus to unified budget, blending funds with general revenue

In the 1980s, President Ronald Reagan implemented a significant change to the federal budget by moving the Social Security surplus into the unified budget, effectively blending these funds with general revenue. This decision, often referred to as "Reagan's Surplus Shift," marked a pivotal moment in the financial management of Social Security. Prior to this, Social Security funds were held in a separate trust fund, ensuring their dedicated use for the program’s beneficiaries. By integrating the surplus into the unified budget, Reagan aimed to address immediate fiscal challenges, but this move also sparked debates about the long-term sustainability and independence of Social Security.

Analytically, the shift had both immediate and long-term implications. In the short term, it provided the federal government with additional funds to offset deficits, offering a temporary solution to budgetary constraints. However, critics argue that this blending of funds undermined the trust and integrity of Social Security, as it allowed the surplus to be used for non-Social Security expenditures. This raised concerns about whether future administrations would prioritize repaying the borrowed funds, especially as the demographic shift toward an aging population increased pressure on the program.

From an instructive perspective, understanding Reagan's Surplus Shift requires examining the mechanics of the unified budget. The unified budget combines all federal revenues and expenditures, including those from trust funds like Social Security. By moving the surplus into this framework, the government could report lower deficits, but it also meant that Social Security’s financial health became intertwined with the overall fiscal health of the nation. This interdependence highlights the importance of transparent budgeting and the need for safeguards to protect dedicated funds.

Persuasively, proponents of Reagan's decision argue that it was a pragmatic response to a fiscal crisis, allowing the government to manage its resources more flexibly. They contend that the surplus was not "spent" but rather borrowed, with the understanding that it would be repaid with interest. However, opponents counter that this approach set a precedent for treating Social Security as a piggy bank for general spending, potentially jeopardizing its ability to fulfill its obligations to retirees, survivors, and disabled individuals.

Comparatively, Reagan's Surplus Shift contrasts with earlier policies that maintained a strict separation of Social Security funds from general revenue. For instance, the 1983 Social Security Amendments, which raised payroll taxes and gradually increased the retirement age, were designed to strengthen the program’s solvency without blending its funds. Reagan’s move, while addressing immediate fiscal needs, introduced a new dynamic that continues to influence debates about Social Security’s funding structure.

In conclusion, Reagan's Surplus Shift represents a critical juncture in the history of Social Security, blending its surplus with general revenue to address short-term fiscal challenges. While this decision provided temporary relief, it also raised enduring questions about the program’s financial independence and long-term viability. As policymakers continue to grapple with Social Security’s future, understanding this shift offers valuable insights into the complexities of federal budgeting and the trade-offs between immediate needs and long-term sustainability.

Understanding State Politics: Power, Policies, and Local Governance Explained

You may want to see also

Explore related products

$16.43 $17.24

![]()

Clinton's Budget Reform: Continued unified budget approach, maintaining Social Security surplus as part of general funds

The Clinton administration's approach to budget reform in the 1990s was marked by a continued commitment to the unified budget framework, which treated Social Security funds as part of the general federal budget. This decision was both pragmatic and controversial, as it allowed the government to leverage the Social Security surplus to reduce the overall federal deficit. By maintaining this unified approach, the Clinton administration aimed to present a more comprehensive view of the nation’s fiscal health, even if it meant blurring the lines between dedicated trust funds and general revenues.

Analytically, the inclusion of Social Security surplus in the general funds served a dual purpose. First, it provided a political tool to showcase deficit reduction efforts, as the surplus helped offset other government spending. Second, it reflected a broader economic strategy to stabilize public finances during a period of economic growth. However, this approach also raised concerns about the long-term sustainability of Social Security, as critics argued that using surplus funds for general spending could undermine the program’s solvency. The Clinton administration countered by emphasizing that the surplus was invested in government securities, ensuring it remained a financial asset for future beneficiaries.

Instructively, understanding this policy requires recognizing the structural differences between Social Security and the general budget. Social Security operates as a pay-as-you-go system, with current payroll taxes funding current benefits. When revenues exceed outlays, the surplus is credited to the Social Security Trust Fund and invested in Treasury bonds. The Clinton administration’s decision to treat this surplus as part of the unified budget did not alter the Trust Fund’s legal status but did change how it was presented in fiscal reporting. This distinction is crucial for policymakers and the public to grasp, as it clarifies that the surplus was not "spent" in the traditional sense but rather accounted for differently.

Persuasively, the Clinton approach can be seen as a pragmatic solution to a complex fiscal challenge. By using the Social Security surplus to reduce the deficit, the administration demonstrated a commitment to fiscal responsibility while avoiding politically difficult cuts to other programs. This strategy also allowed for investments in areas like education and healthcare, which contributed to broader economic prosperity. Critics, however, argue that this approach lacked transparency and risked eroding public trust in Social Security. The debate highlights the tension between short-term fiscal goals and long-term program sustainability, a balance that remains a central challenge in budget policy.

Comparatively, the Clinton administration’s unified budget approach contrasts with later policies, such as the Bush-era tax cuts, which were not offset by equivalent spending reductions or revenue increases. While both administrations faced criticism for their fiscal decisions, Clinton’s use of the Social Security surplus was part of a broader strategy to achieve a balanced budget, a goal realized in 1998. This achievement underscores the importance of context in evaluating budget policies: the economic boom of the 1990s provided a unique opportunity to address fiscal imbalances, and the unified budget approach was a key tool in that effort.

Descriptively, the Clinton budget reform reflected a nuanced understanding of federal finances. By maintaining the Social Security surplus as part of the general funds, the administration created a narrative of fiscal discipline that resonated with both policymakers and the public. This approach also allowed for a more holistic view of the budget, breaking down silos between programs and encouraging a focus on overall economic health. However, it also exposed the fragility of trust fund accounting, as the surplus became a political football in debates over spending priorities. The legacy of this policy continues to shape discussions about budget reform, highlighting the enduring challenge of balancing short-term goals with long-term sustainability.

Are UK Political Party Donations Tax Deductible? What You Need to Know

You may want to see also

Explore related products

$21.84 $22.99

$12.99

![]()

Bush Tax Cuts Impact: Reduced revenue, increasing reliance on Social Security surplus to balance budget

The Bush tax cuts, enacted in 2001 and 2003, significantly reduced federal revenue by lowering tax rates across income brackets, eliminating the estate tax, and reducing taxes on dividends and capital gains. These cuts were projected to reduce federal revenue by $1.35 trillion over ten years, according to the Congressional Budget Office. While proponents argued they would stimulate economic growth, the immediate effect was a sharp decline in government income, creating a fiscal gap that needed bridging.

To compensate for this revenue loss, the federal government increasingly relied on the Social Security surplus to balance the budget. Social Security, funded by payroll taxes, had been running a surplus since the 1980s, with excess funds invested in special Treasury bonds. Instead of using these surpluses to strengthen Social Security’s long-term solvency, the government began using them to offset the deficit caused by the tax cuts. This practice effectively diverted Social Security funds to cover general budget shortfalls, undermining the program’s financial stability.

This reliance on the Social Security surplus was not a sustainable solution. By 2010, the surplus began to shrink as demographic shifts, such as the aging population, increased benefit payouts. The tax cuts, meanwhile, were extended in 2010 and made permanent for most income levels in 2012, further reducing revenue. This dual pressure—reduced income from tax cuts and growing Social Security obligations—exacerbated the program’s funding challenges, leaving it more vulnerable to future shortfalls.

The takeaway is clear: the Bush tax cuts created a revenue gap that led to an over-reliance on Social Security surpluses, diverting funds meant to secure retirees’ futures. This policy decision highlights the interconnectedness of tax policy and entitlement programs, underscoring the need for comprehensive fiscal planning that balances short-term economic goals with long-term financial sustainability.

Understanding the Role and Responsibilities of Political Office

You may want to see also

Explore related products

![]()

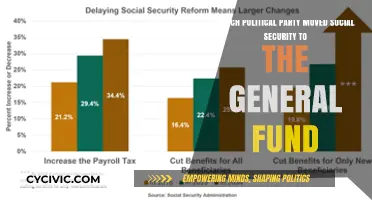

Bipartisan Policy Legacy: Both parties supported unified budget, indirectly affecting Social Security fund allocation

The unified budget, a fiscal framework adopted in 1968, merged federal spending into a single ledger, eliminating the distinction between on-budget and off-budget items like Social Security. Both Democratic and Republican administrations have since relied on this structure, which allows surpluses in one area (e.g., Social Security) to offset deficits elsewhere. While neither party explicitly "moved" Social Security funds, their bipartisan support for the unified budget indirectly enabled the use of Social Security surpluses to mask the true size of federal deficits. This policy legacy highlights how structural choices, not partisan agendas, often drive long-term fiscal outcomes.

Consider the mechanics: Social Security collects payroll taxes exceeding benefit payouts, generating annual surpluses. Under the unified budget, these surpluses are deposited into the Treasury’s general fund, where they are spent on other government programs. In return, the Social Security Trust Fund receives special-issue Treasury bonds, effectively lending its surplus to the federal government. Critics argue this system obscures the need for deficit reduction, as politicians from both parties have historically prioritized spending over addressing structural imbalances. For instance, during the 1990s, when Social Security ran large surpluses, neither party pushed to segregate these funds for future retirees, instead allowing them to subsidize general spending.

A comparative analysis reveals the unified budget’s unintended consequences. Before 1968, Social Security’s finances were accounted for separately, creating political pressure to maintain solvency. Post-unification, the system’s surpluses became a fiscal crutch, delaying reforms. For example, the 1983 Social Security Amendments, which raised payroll taxes and gradually increased the retirement age, were passed only after a bipartisan commission warned of impending insolvency. Yet, even then, the unified budget allowed policymakers to defer more aggressive fixes, as surpluses continued to fund other priorities. This pattern underscores how bipartisan support for a budgeting tool can inadvertently shape policy inertia.

To address this legacy, policymakers could adopt practical reforms. First, reinstate a dual-track budget system, separating Social Security’s finances from general spending. This would force transparency and accountability, as surpluses could no longer offset deficits. Second, establish a bipartisan commission with a mandate to propose solvency solutions, such as adjusting the payroll tax cap or indexing benefits to inflation differently. Finally, educate the public on the distinction between Social Security’s dedicated funding and the general budget, fostering informed debate. While neither party single-handedly "moved" Social Security funds, their shared commitment to the unified budget created a fiscal environment where such funds were indirectly reallocated—a lesson in how structural choices outlast partisan shifts.

Unveiling Ed Kurtz's Political Party Affiliation: A Comprehensive Overview

You may want to see also

Frequently asked questions

Neither major political party has moved Social Security funds into the federal budget. Social Security funds are held in trust funds separate from the general federal budget, as established by law.

No, the Democratic Party has not redirected Social Security funds for other government programs. Social Security funds are legally restricted to paying benefits and administrative costs.

The federal government, under both Republican and Democratic administrations, has borrowed from Social Security trust funds by issuing Treasury bonds. This is part of the intergovernmental borrowing process and does not involve "moving" funds.

Neither party is responsible for using the Social Security trust fund surplus for other purposes. The surplus is invested in Treasury securities, and the funds remain dedicated to Social Security beneficiaries.

Some Republican leaders, notably during George W. Bush's presidency, proposed partial privatization of Social Security, allowing individuals to invest a portion of their payroll taxes in private accounts. However, this proposal did not involve moving existing trust fund assets.