The 16th Amendment to the US Constitution, ratified on February 3, 1913, grants Congress the authority to levy and collect income taxes without apportionment among states or consideration of population. This amendment was proposed by President William Howard Taft in 1909 as a 2% federal income tax on corporations and was ratified by 36 states, coming into effect on February 25, 1913. The 16th Amendment's impact was significant, shifting how the federal government received funding and marking a notable change in the American way of life.

| Characteristics | Values |

|---|---|

| Date proposed | June 16, 1909 |

| Date passed by Congress | July 2, 1909 |

| Date ratified | February 3, 1913 |

| Date took effect | February 25, 1913 |

| Purpose | Grant Congress the authority to issue an income tax without determining it based on population |

| Powers granted to Congress | Power to lay and collect taxes on incomes from whatever source derived |

| Powers removed from Congress | Ability to impose a duty or tax upon personal property or upon income arising from rents of real estate or personal property |

Explore related products

What You'll Learn

![]()

Congress's right to impose federal income tax

The 16th Amendment to the U.S. Constitution, ratified on February 3, 1913, established Congress's right to impose a federal income tax. The amendment was first proposed by Senator Norris Brown of Nebraska, who submitted two proposals, Senate Resolutions Nos. 25 and 39. The proposal finally accepted was Senate Joint Resolution No. 40, introduced by Senator Nelson W. Aldrich of Rhode Island, the Senate Majority Leader, and Finance Committee Chairman.

The 16th Amendment grants Congress the power to "lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration." This means that Congress can impose income taxes without determining the tax based on population, which was previously required for "direct" taxes under Article I of the Constitution.

The amendment was passed by Congress on July 2, 1909, and ratified by the requisite 36 states on February 3, 1913, with Delaware being the final state to approve it. The amendment was subsequently ratified by six additional states, bringing the total number of ratifying states to 42 out of the then 48 states.

The 16th Amendment had a significant impact on how the federal government received funding for its operations. It also had far-reaching social and economic impacts, as it changed the way Americans paid taxes and raised funds for the government. The amendment was part of a series of political maneuvers that culminated in a curious turn of events, as it was originally intended to temporarily defuse progressive calls for new taxes in the 1909 Payne-Aldrich Tariff Act.

Challenges to Congress's power to tax income under the 16th Amendment have typically centred on the definition of "income." However, legal scholars argue that the focus should not be on whether the item being taxed satisfies an isolated definition of "income" but rather on the original meaning of "taxes on incomes." They contend that the 16th Amendment's purpose was to restore Congress's "complete and plenary power of income taxation" by overruling the Supreme Court case of Pollock v. Farmers' Loan & Trust Co., which had introduced impediments to Congress's taxation powers.

Amending the Constitution: What Percentage is Needed?

You may want to see also

Explore related products

![]()

The shift in federal government funding

The 16th Amendment to the US Constitution, ratified in 1913, established Congress's right to impose a federal income tax without determining it based on each state's population. This amendment shifted the way the federal government received funding for its operations.

Before the 16th Amendment, the majority of funds given to the federal government came from tariffs on domestic and international goods. The 16th Amendment's income tax provision allowed the federal government to collect taxes from a broader range of sources, including personal income, property, bonds, stocks, and investments. This shift in taxation powers had a significant long-term impact on how the federal government received funding and resulted in dramatic changes in the American way of life.

The 16th Amendment was proposed by President William Howard Taft in 1909 as a way to impose a 2% federal income tax on corporations. It was part of the congressional debate over the 1909 Payne-Aldrich Tariff Act, and its proposal aimed to temporarily defuse progressive calls for new taxes within the act. The amendment faced opposition from some, who argued that it would lead to a more powerful and centralized federal government. However, with the rise of the Progressive Party and the victory of the Democratic Party in the 1912 election, the amendment gained momentum and was ratified by the required number of states in 1913.

The amendment's impact on federal government funding was significant. The Revenue Act of 1913, enacted shortly after ratification, lowered tariffs and implemented a federal income tax. While exemptions and deductions meant that initially, only a small percentage of the population paid income taxes, the amendment laid the foundation for a broader tax base and a more stable source of revenue for the federal government.

The 16th Amendment's authorization of income taxation empowered Congress to collect taxes from a diverse range of sources, marking a shift from the previous reliance on tariffs and indirect forms of taxation. This shift in funding sources allowed the federal government to access a more consistent and substantial revenue stream, enabling it to finance its operations and support its growing political and military power.

Civil War's Constitutional Legacy: Amendments

You may want to see also

Explore related products

![]()

The impact on citizens

The 16th Amendment to the US Constitution, ratified on February 3, 1913, established Congress's right to impose and collect federal income tax without determining it based on each state's population. This amendment had a significant impact on the lives of American citizens.

Firstly, it changed the way the federal government received funding for its operations. Before the 16th Amendment, the majority of funds for the federal government came from tariffs on domestic and international goods. The amendment shifted the primary source of funding to income taxes, which were now imposed on citizens' incomes from various sources without regard to population or census data. This meant that citizens' contributions to the federal government were now directly linked to their income levels, rather than being based solely on the consumption of goods.

Secondly, the 16th Amendment had a significant impact on the distribution of economic power in the country. Before its ratification, there were concerns that the wealthiest Americans had consolidated too much economic power. By imposing an income tax, the amendment aimed to redistribute wealth and ensure that those with higher incomes contributed more to the nation's finances. This had a direct impact on citizens' disposable incomes and spending power, as a portion of their income was now directed towards income tax.

Additionally, the 16th Amendment influenced the political landscape of the country. The amendment's ratification was supported by citizens in the West and South, who viewed it as a way to raise funds from those less well-off. It also gained backing from insurgent Republicans, who believed it would help finance the nation's growing political and military power. The amendment's impact on government funding and the distribution of economic power had repercussions for various political factions and ideologies.

Moreover, the 16th Amendment had long-term implications for the relationship between citizens and the federal government. It centralized power in the federal government by providing it with a direct source of income taxation. This shift in funding sources may have influenced citizens' perceptions of government intervention and their relationship with the state. The amendment's impact on income distribution and government finances could have also shaped public opinion and political participation among citizens.

Finally, the 16th Amendment's impact on citizens was felt through its influence on legal interpretations and challenges related to taxation. The amendment's focus on "taxes on incomes, from whatever source derived" led to debates about the definition of "income" and the scope of congressional taxation power. Citizens and legal scholars have engaged in discussions and court cases, such as Moore v. United States, to clarify and challenge the boundaries of taxation authority granted by the 16th Amendment. These legal discussions have had direct consequences for how citizens' incomes, properties, and investments are taxed.

Amendments: The Constitution's Living, Breathing Word

You may want to see also

Explore related products

![]()

The 1912 election's influence

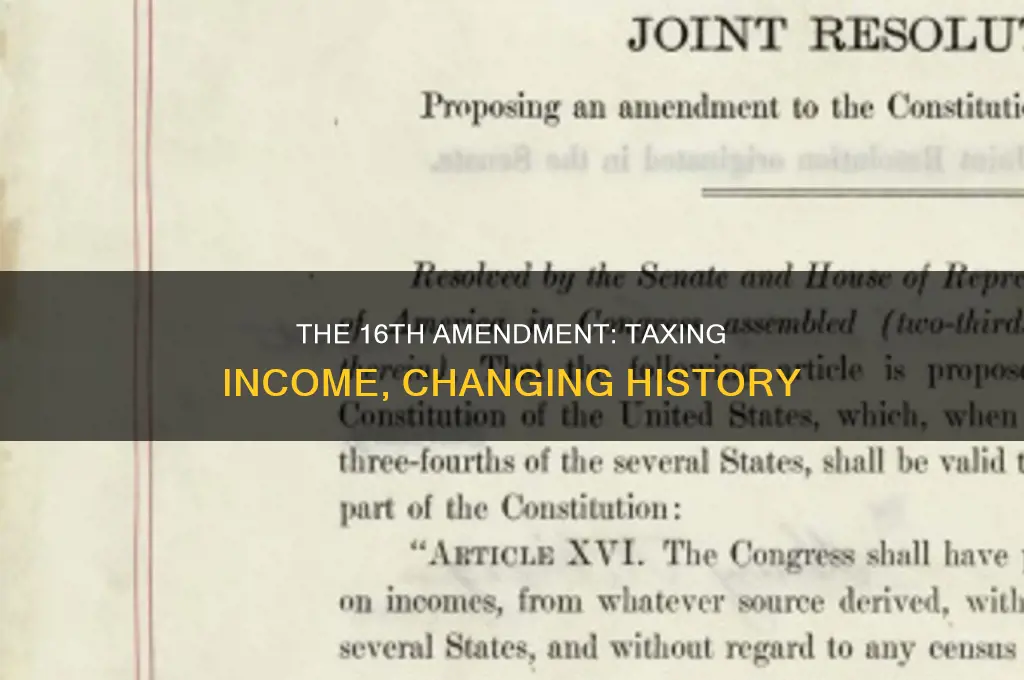

The 16th Amendment to the US Constitution, ratified in 1913, grants Congress the authority to issue an income tax without having to determine it based on population. The text of the amendment is as follows:

> The Congress shall have the power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.

The 1912 elections influenced the 16th Amendment in several ways. Firstly, three advocates of a federal income tax ran in the 1912 presidential election. The victory of the Democratic Party in the 1912 election also contributed to an easier ratification phase for the amendment.

The rise of the Progressive Party, which supported the direct election of senators, was another significant factor. The 1912 elections saw the election of 30 new senators, 14 of whom had been chosen through party primaries, reflecting the popular choice in their states. This trend towards direct election was further bolstered by the 1912 election results, with an increasing number of states adopting direct primaries or the \"Oregon System\", where state legislative candidates committed to respecting the outcome of a non-binding direct election for senator.

The Seventeenth Amendment, proposed by the 62nd Congress in 1912, established the direct election of senators by the people, rather than by state legislatures as originally outlined in the Constitution. This amendment was ratified by the required number of states in 1913, further reflecting the shift towards direct democracy and the influence of the 1912 election results.

In summary, the 1912 elections influenced the 16th Amendment by bringing the issue of taxation and income tax to the forefront, contributing to the ratification process, and shaping the broader political landscape with the rise of the Progressive Party and the shift towards direct elections for senators.

Amendments to the US Constitution: A Dynamic History

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![]()

The constitutional question

The 16th Amendment to the U.S. Constitution, ratified on February 3, 1913, resolved the constitutional question of how to tax income. The text of the amendment is as follows:

> The Congress shall have the power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.

Before the 16th Amendment, Congress already had the power to tax incomes. However, the Supreme Court case of Pollock v. Farmers' Loan & Trust Co. introduced an impediment, holding that taxes on incomes from certain sources were "direct taxes" and thus subject to the constitutional requirement of apportionment by population. This decision led to concerns that the consolidation of economic power by the wealthiest Americans would hinder the ability of incomes to contribute to the support of the national government.

The 16th Amendment removed this impediment by explicitly granting Congress the power to tax incomes from any source without regard to apportionment or population. This shift had far-reaching social and economic impacts, changing the way the federal government received funding and marking a departure from the previous reliance on tariffs on domestic and international goods.

The interpretation of the 16th Amendment has continued to be a subject of debate, with Supreme Court cases such as Moore v. United States in 2024 considering the scope of Congress's power to tax under the amendment.

Amending the Constitution: A Step-by-Step Guide

You may want to see also

Frequently asked questions

The 16th Amendment to the US Constitution, ratified on February 3, 1913, established Congress's right to impose a federal income tax without determining it based on population.

The 16th Amendment shifted the way the federal government received funding for its works. It also changed the American way of life, with the Revenue Act of 1913 greatly lowering tariffs and implementing a federal income tax.

The original meaning of the 16th Amendment was to overrule the Supreme Court case of Pollock v. Farmers’ Loan & Trust Co. and restore the “complete and plenary power of income taxation”.

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UY218_.jpg)