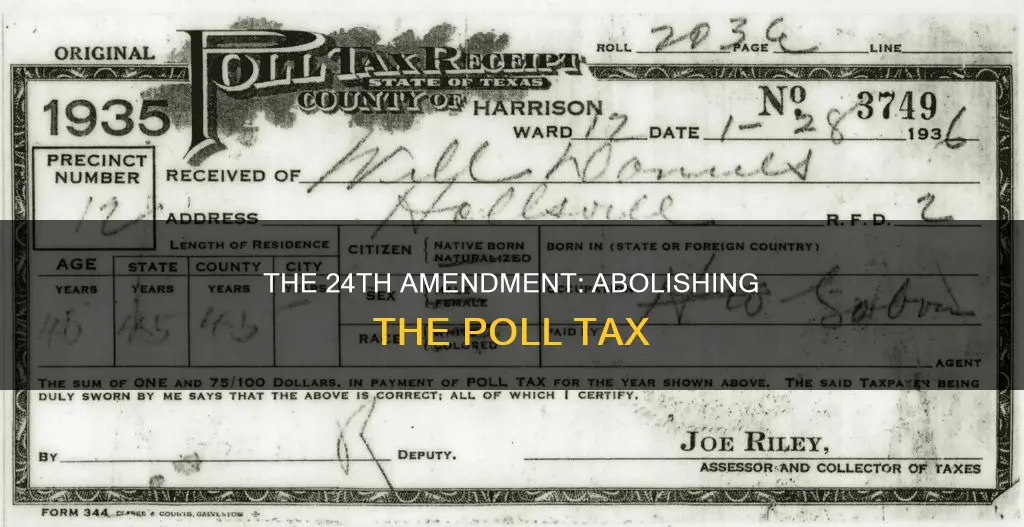

The Twenty-Fourth Amendment to the US Constitution, ratified in 1964, abolished poll taxes as a prerequisite for voting in federal elections. Before the amendment, many states restricted the right to vote to those who could afford to pay a poll tax, which was often used to prevent African Americans and poor whites from voting. The Twenty-Fourth Amendment was a significant step in expanding voting rights in America, though it should be noted that it only applied to federal elections, and some states continued to maintain poll taxes for state and local elections.

| Characteristics | Values |

|---|---|

| Date proposed by Congress | 27 August 1962 |

| Date submitted to states | 24 September 1962 |

| Date ratified by states | 23 January 1964 |

| Prohibited | Federal and state governments from imposing poll taxes before a citizen could participate in a federal election |

| Overruled | Breedlove v. Suttles |

| Extended to state elections | 1966, following Harper v. Virginia Board of Elections |

Explore related products

![The Rules of the Law Society of British Columbia, Taking Effect on the 4th Day of October, 1897 (with Amendments) and the Legal Professions Act, R.S. 1897, C. 24, and Amendments [microform]](https://m.media-amazon.com/images/I/61hceDvrf-L._AC_UY218_.jpg)

![]()

Poll tax abolition

The Twenty-fourth Amendment to the US Constitution abolished the use of poll taxes as a prerequisite for voting in federal elections. The amendment was proposed by Congress on 27 August 1962 and ratified by the states on 23 January 1964.

The concept of poll taxes as a method of taxation dates back centuries. In Colonial America, governments initially restricted the right to vote to property owners, but later transitioned to poll taxes. As the nation expanded, some states eliminated poll taxes and restricted voting rights exclusively to white men.

In the late 19th and early 20th centuries, following the Civil War and the Reconstruction Era, states across the former Confederacy imposed a series of laws that restricted the civil liberties of newly freed African Americans. This included the use of poll taxes, which were upheld by the Supreme Court in the 1937 case of Breedlove v. Suttles. The case tested the constitutionality of a Georgia poll tax statute, which imposed a one-dollar poll tax on voters between the ages of 21 and 60, with exceptions for blind people and women.

During the civil rights era of the 1950s, policies such as poll taxes were increasingly seen as barriers to voting rights, particularly for African Americans and the poor. The Twenty-fourth Amendment was proposed and ratified to eliminate this economic instrument that limited voter participation. The amendment prohibited both Congress and the states from requiring the payment of a poll tax or any other tax as a condition for voting in federal elections.

Despite the Twenty-fourth Amendment, some states continued to maintain their poll taxes in opposition to the new law. Poll taxes were completely eliminated after the 1966 Supreme Court decision in Harper v. Virginia Board of Elections, which ruled that poll taxes in all elections, federal, state, and local, were unconstitutional.

Amending the Constitution: Most Popular Methods

You may want to see also

Explore related products

![]()

Voting rights

The Twenty-Fourth Amendment to the US Constitution abolished poll taxes as a prerequisite for voting in federal elections. The right to vote in the US is conferred by the state, and in the late 19th and early 20th centuries, many states restricted voting rights to those who could afford a poll tax. This disproportionately affected African Americans and poor whites, effectively preventing them from voting.

The poll tax was a method of taxation that dates back centuries. In Colonial America, only property owners could vote, but this transitioned to poll taxes over time. After the Civil War, the Fifteenth Amendment was passed, which granted the right to vote to African American men. However, this was undermined by the poll tax, which was adopted by many Southern states, along with other discriminatory laws, to limit the political participation of African Americans.

The Twenty-Fourth Amendment was proposed by Senator Spessard Lindsey Holland of Florida and ratified in 1964 to address this issue and eliminate the economic barrier to voting. It states that the right of US citizens to vote in any election for President, Vice President, or Congress shall not be denied or abridged by the failure to pay any poll tax or other tax. The amendment overruled the 1937 Supreme Court decision in Breedlove v. Suttles, which had upheld the constitutionality of poll taxes.

While the Twenty-Fourth Amendment was a significant step forward, it only applied to federal elections. The Voting Rights Act of 1965 further strengthened voting rights by granting the US Attorney General the power to intervene in state and local elections where poll taxes were used to discriminate based on race. The Supreme Court also played a role in extending the prohibition of poll taxes to state elections in Harper v. Virginia Board of Electors in 1966.

The Fifth Amendment: Your Rights and Protections

You may want to see also

Explore related products

![]()

Federal elections

The Twenty-Fourth Amendment to the US Constitution abolished poll taxes as a prerequisite for voting in federal elections. The Amendment was ratified in 1964, and it effectively overruled the 1937 Breedlove v. Suttles case, in which the Supreme Court deemed poll taxes constitutional.

Poll taxes were a method of taxation that dates back centuries, and governments have used them to raise revenue. In Colonial America, only property owners had the right to vote, but this transitioned to include those who paid a poll tax. Over time, states eliminated poll taxes as a voting requirement and restricted voting rights to white men.

The Fifteenth Amendment, passed after the US Civil War, changed this dynamic by extending the right to vote to African American men. However, in the late 19th and early 20th centuries, southern states adopted poll taxes in their laws and constitutions to prevent African Americans and poor whites from voting. This was particularly an issue during the civil rights era of the 1950s, as poll taxes were seen as barriers to voting rights for African Americans and the poor.

The Twenty-Fourth Amendment was proposed to eliminate this economic barrier to voting in federal elections. It states that citizens' right to vote in any primary or other election for President, Vice President, or for members of Congress, shall not be denied or abridged by the United States or any State due to the failure to pay any poll tax or other tax.

While the Twenty-Fourth Amendment was a significant step forward, it is important to note that it only applied to federal elections. Additionally, some states continued to maintain their poll taxes in opposition to the new law, and there were still issues with literacy tests being used to discriminate against voters. It took further Supreme Court decisions and the Voting Rights Act of 1965 to address these issues and fully protect voting rights in the United States.

Amendment Story: 21st Amendment's Addition to the Constitution

You may want to see also

Explore related products

![]()

State elections

The Twenty-fourth Amendment to the US Constitution abolished poll taxes as a prerequisite for voting in federal elections. Before its ratification in 1964, many states restricted the right to vote to those who could afford to pay a poll tax, which was often used to prevent African Americans and poor whites from voting.

The concept of poll taxes as a method of taxation dates back centuries, with governments using them to raise revenue. In Colonial America, only those who owned property had the right to vote. Over time, this transitioned to poll taxes, and as the nation expanded, voting rights were restricted exclusively to white men. The Fifteenth Amendment, passed after the US Civil War, changed this by extending the right to vote to African American men.

Despite this, in the late 19th and early 20th centuries, several Southern states adopted poll taxes in their laws and constitutions. This trend was bolstered by the 1937 Supreme Court decision in Breedlove v. Suttles, which upheld the constitutionality of a Georgia poll tax. The case of Breedlove v. Suttles specifically challenged a Georgia statute that imposed a one-dollar poll tax on voters between the ages of 21 and 60, except for blind people or women.

The Twenty-fourth Amendment was proposed by Senator Spessard Lindsey Holland of Florida and ratified in 1964 to eliminate the economic barrier of poll taxes and expand voting rights. However, it only applied to federal elections. The Voting Rights Act of 1965 further strengthened voting rights by granting the US Attorney General the power to intervene in cases of racial discrimination in state and local elections.

While the Twenty-fourth Amendment was a significant step towards ensuring voting rights, it did not immediately eliminate poll taxes in all elections. Some states continued to maintain their poll taxes, and it was not until the 1966 Supreme Court decision in Harper v. Virginia Board of Elections that poll taxes were completely eliminated in federal, state, and local elections. This decision affirmed that poll taxes violated the Fourteenth Amendment's equal protection clause and were therefore unconstitutional.

Amendments on the Ballot: Understanding Your Vote's Impact

You may want to see also

Explore related products

![]()

Civil rights

The Twenty-fourth Amendment to the US Constitution, ratified in 1964, was a significant step forward for civil rights in the country. The amendment abolished poll taxes, which had been used to restrict voting rights, particularly for African Americans and the poor.

The concept of poll taxes has a long history, dating back centuries as a method of taxation. In Colonial America, the right to vote was initially restricted to property owners, but this later transitioned to poll taxes. As the nation expanded, some states eliminated poll taxes as a prerequisite for voting, but this right was still restricted to white men.

The Fifteenth Amendment, passed after the US Civil War during Reconstruction, changed this dynamic by extending the right to vote to African American men. However, in the late 19th and early 20th centuries, several Southern states adopted poll taxes in their laws and constitutions. The purpose of these poll taxes was to prevent African Americans and poor whites from voting.

The Twenty-fourth Amendment prohibited both Congress and the states from requiring the payment of a poll tax or any other tax as a condition for voting in federal elections. It was proposed by Congress in 1962 and ratified by the states in 1964, with President Lyndon B. Johnson hailing it as a "triumph of liberty over restriction".

The amendment overruled the 1937 Supreme Court decision in Breedlove v. Suttles, which had upheld the constitutionality of poll taxes. While the Twenty-fourth Amendment was a major step forward, it only applied to federal elections. It took further action, such as the Voting Rights Act of 1965, to address discrimination in state and local elections.

The Twenty-fourth Amendment was part of a broader civil rights movement in the 1950s and 1960s, which sought to address the long-standing disenfranchisement of African Americans and ensure equal voting rights for all citizens. This included the landmark Brown v. Board of Education decision in 1954, which helped to shift the perception of poll taxes as barriers to voting rights. The amendment was a crucial step in dismantling the legal framework that had been used to restrict the voting rights of racial minorities and the poor, contributing to the expansion of civil rights in the United States.

Recent Amendments: The Living Constitution

You may want to see also

Frequently asked questions

The Twenty-fourth Amendment abolished poll taxes, which previously prevented African Americans and poor whites from voting.

Poll taxes were a method of taxation that dates back centuries. Governments used poll taxes to raise revenue. In Colonial America, only those who owned property had the right to vote. Later, this transitioned to poll taxes, where voters had to pay a fee to enter polling places to cast their ballots.

The Twenty-fourth Amendment was ratified on January 23, 1964, when South Dakota became the final state to ratify it.

The Twenty-fourth Amendment changed the landscape of voting rights in America. It effectively overruled the 1937 Breedlove v. Suttles case, in which the Supreme Court deemed poll taxes constitutional. The Amendment prohibited federal and state governments from imposing poll taxes before a citizen could vote in federal elections.

No, the Twenty-fourth Amendment only applied to federal elections. However, the Voting Rights Act of 1965 gave the U.S. Attorney General the authority to pursue injunctive relief when states used poll taxes to discriminate in state and local elections.