A loan is a form of credit where a specific amount of money is given to someone with the agreement that it will be paid back later, generally with interest. The lender, usually a corporation, financial institution, or government, advances a sum of money to the borrower, who agrees to a set of terms, including finance charges, interest, repayment date, and other conditions. The borrower may be required to provide specific details such as the reason for the loan, their financial history, and other information. The lender reviews this information, along with the borrower's creditworthiness, before deciding to offer them a loan. The loan recipient refers to the eligible entity or individual that has received the loan, and this can vary depending on the loan program. Understanding the requirements and dynamics of loan agreements is crucial for both lenders and borrowers to ensure informed decision-making and compliance with relevant laws and regulations.

| Characteristics | Values |

|---|---|

| Definition of loan recipient | An eligible entity that has received a loan from any of the revolving loan funds |

| Who is a loan recipient? | A community water supply that has been provided a loan from the PWSLP under this Part |

| A Charter School or Chartering Authority that has applied on behalf of a Charter School for which the Authority has approved and issued a loan through the Program | |

| A state, local, or other governmental entity that owns diesel vehicles or equipment | |

| An entity or individual which has received a loan from the public bank | |

| The person or Business who has obtained a loan from the Board, or a representative of that person or Business | |

| The eligible organization that has applied for and received financial assistance under the LAP | |

| A Nondesignated Public Hospital that has been approved to receive a Program loan from the Program | |

| Requirements for a loan | The reason for the loan, financial history, Social Security number (SSN), and other information |

| Income, credit score, and debt levels | |

| Collateral | |

| Types of loans | Secured, unsecured, commercial, and personal loans |

| Revolving loans, term loans | |

| Interest-only payment loan, amortizing loan | |

| Bridge loan |

Explore related products

![]()

Lender requirements

Additionally, lenders are legally obligated to provide transparency around loan terms and costs. This includes disclosing relevant information such as interest rates, finance charges, repayment dates, and other conditions. In the United States, the Truth in Lending Act (TILA) protects consumers by requiring lenders to disclose the true cost of the loan, allowing borrowers to make informed decisions and compare loan options. Lenders must also adhere to usury laws, which govern the maximum interest rates that can be charged, with these rates varying by state.

When applying for a loan, borrowers may need to provide specific details and documentation. This can include the reason for the loan, financial history, Social Security number, and other identifying information. In some cases, such as with mortgage loans, a signed purchase contract may be necessary before a lender provides a Loan Estimate. It is worth noting that lenders cannot require additional information beyond what is legally mandated, but providing more details can lead to a more accurate Loan Estimate.

For intra-family loans, there are specific requirements mandated by the IRS. These loans must include a signed written agreement, a fixed repayment schedule, and a minimum interest rate based on Applicable Federal Rates (AFRs). Failing to meet these requirements may result in tax implications for the lender.

Lastly, lenders should outline the terms of the loan in a contract before any money or property is exchanged. This contract serves as a legally binding agreement between the lender and the borrower, detailing the rights and obligations of both parties.

Harvard's Guide: Understanding Plagiarism and Using Sources

You may want to see also

Explore related products

![]()

Loan types

Loans can be categorised into different types based on their purpose, function, and features.

Purpose

Loans can be used for various purposes, including:

- Education: Student loans help individuals pursue post-secondary education, including college and graduate school. These loans are available from the federal government or private lenders and can cover expenses such as tuition, room, and board.

- Vehicle Purchase: Auto loans enable individuals to purchase new or used vehicles, including trucks, cars, and RVs. These loans are typically secured by the vehicle being purchased.

- Home Purchase: Mortgage loans assist individuals in purchasing homes and building equity. The loan amount depends on factors such as background and income, and the loan term can range from 10 to 30 years or more.

- Debt Consolidation: These loans help individuals consolidate their existing debts into a single loan, potentially lowering their interest rates and monthly payments.

- Personal Use: Personal loans can be used for various purposes, including emergency expenses, weddings, or home improvement projects. They are typically unsecured and may have fixed or variable interest rates.

Function

Loans can function in different ways, including:

- Secured vs. Unsecured: A secured loan is backed by collateral, such as a mortgage, while an unsecured loan does not require collateral, such as a credit card.

- Fixed-Rate vs. Variable-Rate: Fixed-rate loans have a static interest rate throughout the loan term, while variable-rate loans' interest rates may change with the prime rate.

- Term Loans vs. Revolving Loans: Term loans are fixed-rate, fixed-payment loans with a set repayment schedule. In contrast, revolving loans or lines of credit can be spent, repaid, and spent again up to a specified limit.

Features

Loans can have different features, including:

- Interest-Only Payment Loans: In these loans, the lender receives interest during the term, and the principal is repaid in a lump sum at maturity.

- Amortization: This refers to loan payments made in equal periodic amounts, including accrued interest, to pay off the debt at the end of a fixed period.

- Loan Estimates: Lenders provide loan estimates to borrowers, outlining the expected loan terms before final approval.

Constitutional Court Cases: A Historical Overview

You may want to see also

Explore related products

![]()

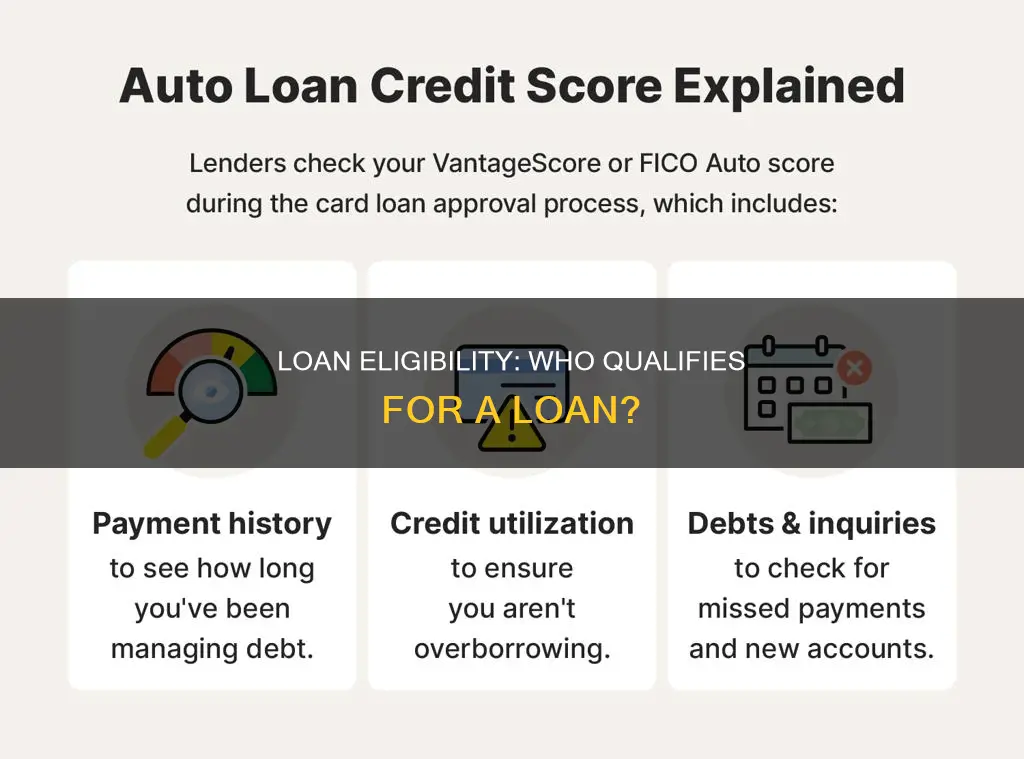

Loan eligibility

- Financial History and Creditworthiness: Lenders typically assess an applicant's financial history and creditworthiness. This includes reviewing income, credit score, debt levels, and debt-to-income (DTI) ratio. A strong credit score and stable financial history indicate higher creditworthiness, increasing the chances of loan approval.

- Collateral and Security: Some loans, like mortgages, are secured by collateral. This means that the borrower offers an asset as security for the loan. If the borrower defaults, the lender can seize the collateral to recover the loan amount. Unsecured loans, such as credit cards, do not require collateral but often carry higher interest rates.

- Loan Type and Purpose: Different types of loans have specific eligibility criteria. For example, a mortgage loan may require a down payment and a signed purchase contract. The purpose of the loan may also be considered, with some lenders requiring details on how the funds will be used.

- Income and Employment Status: Lenders often consider the borrower's income and employment status. A stable income demonstrates an enhanced ability to repay the loan. Employment details, such as job stability and income consistency, can play a role in determining eligibility.

- Credit History and Debt Service Coverage: Lenders review an applicant's credit history, including previous loans, repayment history, and any delinquencies or defaults. They also assess the borrower's ability to cover debt obligations, ensuring that income sufficiently covers existing debts and the proposed loan payments.

- Applicable Laws and Regulations: Loan eligibility must comply with relevant laws and regulations. For example, the Truth in Lending Act (TILA) mandates that lenders disclose the true cost and terms of a loan. Additionally, usury laws govern the maximum interest rates that lenders can charge, and these vary by state in the United States.

- Specific Program Requirements: Eligibility can also depend on the specific loan program or lender. For instance, certain loan programs may be tailored for specific entities, such as public hospitals, universities, or community water supply initiatives. These programs have unique eligibility criteria that align with their specific objectives.

It is important to note that providing comprehensive information and maintaining a good credit history enhances loan eligibility. Lenders may request additional details or documentation to make informed decisions about loan approval.

The Federal Judiciary: Upholding Constitutional Principles

You may want to see also

Explore related products

![]()

Loan approval

Lenders will typically consider the prospective borrower's income, credit score, and debt levels before deciding to offer them a loan. They may also require collateral, such as a mortgage, to secure the loan. The lender must provide a reason for denying a loan application, and if the application is approved, both parties will sign a contract outlining the terms of the loan, including any finance charges, interest, and repayment dates.

In the case of family loans, it is important to note that the IRS mandates that any loan between family members be made with a signed written agreement, a fixed repayment schedule, and a minimum interest rate. Failure to charge an adequate interest rate may result in the IRS treating the interest as a gift, which could have tax implications.

Overall, loan approval is a process that involves the borrower providing detailed information to the lender, who will then review and decide whether to approve the loan based on the borrower's financial situation and the terms of the loan.

Illinois Constitution: Environmental Provisions Explained

You may want to see also

Explore related products

![]()

Loan repayment

Interest is a critical component of loan repayment. It is a fee charged by the lender, calculated as a percentage of the principal amount. Interest can be paid in different ways depending on the type of loan. In an interest-only payment loan, the borrower pays only the interest during the loan term and repays the principal in full at the end of the loan period. In other cases, the interest is integrated into the periodic loan payments, with a portion of each payment going towards reducing the principal balance.

Lenders may also require collateral to secure the loan. Collateral is an asset, such as a house or vehicle, that the borrower pledges as a guarantee for the loan. If the borrower fails to repay the loan, the lender has the right to seize the collateral to recoup their losses. Collateral provides an incentive for the borrower to repay the loan and reduces the lender's risk.

When it comes to family loans, the IRS has specific requirements. Any loan between family members must have a signed written agreement, a fixed repayment schedule, and a minimum interest rate. Failing to meet these criteria may result in tax implications, and loans exceeding $10,000 or used for income-producing purposes may trigger additional considerations.

The Preamble: Why It's at the Start of the Constitution

You may want to see also

Frequently asked questions

A loan is a form of credit where a specific amount of money is lent to another party with the agreement that it will be paid back later, generally with interest.

A complete, quality set of business purpose loan documents provides a lender with peace of mind. It reflects all necessary and relevant terms and conditions of the loan, provides comprehensive protection to the lender, and covers a multitude of potentially detrimental scenarios that can arise during the life of the loan.

The borrower may be required to provide specific details such as the reason for the loan, their financial history, Social Security number (SSN), and other information. The lender reviews this information, along with the person's debt-to-income (DTI) ratio, to determine if the loan can be paid back.