The Federal Reserve System, created in 1913, oversees the nation's money supply and dictates the amount of cash, or the reserve ratio, that each bank must maintain. The Federal Reserve obliges banks to hold a certain amount of cash in reserve so that they never run short and have to refuse a customer's withdrawal, possibly triggering a bank run. The reserve requirement is one of the three main tools of monetary policy, and it can be used to control liquidity in the financial system. The Federal Reserve's Board of Governors sets the requirement as well as the interest rate banks get paid on excess reserves.

| Characteristics | Values |

|---|---|

| Definition | Bank reserves are the cash minimums that financial institutions must have on hand to meet central bank requirements. |

| Purpose | To ensure that banks can meet any large and unexpected demand for withdrawals and to prevent bank runs. |

| History | The reserve rate for American banks has historically been set at between 0% and 10%. The Federal Reserve System was created in 1913 and reserve requirements have changed over time. |

| Current Rate | 0% as of March 26, 2020, in response to the COVID-19 pandemic. |

| Flexibility | The Federal Reserve can adjust the reserve requirement to influence monetary policy. Lowering the requirement allows banks to make more loans and increase economic activity, while raising it slows economic growth. |

| Interest | The Federal Reserve pays banks interest on their reserves. |

| Legal Status | The Federal Reserve Banks have an intermediate legal status, with features of both private corporations and public federal agencies. |

Explore related products

What You'll Learn

![]()

Banks must keep reserves to prevent panic and bank runs

The Federal Reserve obliges banks to hold a certain amount of cash in reserve to prevent them from running short and having to refuse a customer's withdrawal, which could trigger a bank run. Bank runs can lead to a multitude of social and economic problems. The Federal Reserve System was designed to prevent or minimize the occurrence of bank runs and to act as a lender of last resort when they do occur.

The Federal Reserve can use bank reserve levels as a tool in monetary policy. It can lower the reserve requirement to allow banks to make new loans and increase economic activity, or it can require banks to increase their reserves to slow economic growth. For example, in response to the 2008 financial crisis, the Federal Reserve began paying banks interest on their reserves and cut interest rates to boost demand for loans and stimulate the economy.

The practice of holding reserves started with the first commercial banks during the early 19th century. The creation of the Federal Reserve and its constituent banks in 1913 further eliminated the risks and costs of maintaining reserves and reduced reserve requirements from their earlier high levels. For example, in 1917, reserve requirements for three types of banks under the Federal Reserve were set at 13%, 10%, and 7%.

Constitutional Debates: Shaping Reconstruction's Destiny

You may want to see also

Explore related products

![]()

The Federal Reserve dictates the reserve ratio

The Federal Reserve System was created in 1913 to oversee the nation's money supply and prevent bank runs. Bank reserves are the cash minimums that financial institutions must have on hand to meet central bank requirements. The Federal Reserve dictates the reserve ratio, or the amount of cash that each bank must maintain as a percentage of its deposits. This reserve ratio has historically ranged from zero to 10% of bank deposits.

The Federal Reserve Act authorises the Board to establish reserve requirements within specified ranges for certain types of deposits and other liabilities of depository institutions. The Board of Governors sets the reserve requirement, which is one of the three main tools of monetary policy. The other two tools are open market operations and the discount rate. By adjusting the reserve requirement, the Federal Reserve can influence the liquidity in the financial system and, consequently, the level of economic activity.

For example, reducing the reserve requirement allows banks to make more loans and increase economic activity, while increasing the reserve requirement slows economic growth by reducing the amount of money available for lending. The Federal Reserve may also require banks to increase their reserves to prevent bank runs and ensure they can meet customer withdrawal demands.

The reserve requirement has changed over time, with revisions made to the regulations in 1972, 1960, 1962, and 1959. In 1977, Congress expanded the Federal Reserve's role by defining price stability as a national policy goal. In 2006, the Financial Services Regulatory Relief Act gave the Federal Reserve the right to pay interest on excess reserves. During the 2008 financial crisis, the Federal Reserve began paying interest on required and excess reserve balances, and in 2020, the reserve requirement ratio was reduced to zero in response to the COVID-19 pandemic.

Slavery's Constitutional Treatment in 1787: Examining the Past

You may want to see also

Explore related products

![]()

Reserve requirements are a tool for monetary policy

The Federal Reserve System, established in 1913, oversees the nation's money supply and provides the country with a safe, flexible, and stable monetary and financial system. One of the three main tools of monetary policy at the disposal of the Federal Reserve is the reserve requirement. This is the amount of cash that financial institutions must have in their vaults or at the closest Federal Reserve bank, in line with deposits made by their customers. The reserve requirement is set by the Federal Reserve Board, also known as the Board of Governors, and is based on a formula set by Federal Reserve Board regulations.

The reserve requirement is a crucial tool for maintaining liquidity in the financial system. By reducing the reserve requirement, the Federal Reserve executes an expansionary monetary policy, allowing banks to make new loans and increase economic activity. Conversely, by increasing the reserve requirement, the Federal Reserve exercises a contractionary monetary policy, slowing economic growth by reducing the amount of money available for lending. This causes a decrease in liquidity and a subsequent cooling of the economy.

Historically, the reserve rate for American banks has ranged from zero to 10%. However, in response to the COVID-19 pandemic, the Federal Reserve reduced the reserve requirement ratio to zero across all deposit tiers, effective March 26, 2020. This action eliminated reserve requirements for all depository institutions, including banks, credit unions, and savings and loan associations.

Prior to this change, the reserve requirement ratios on net transaction accounts differed based on the amount of net transaction accounts at the institution. For example, effective November 9, 1972, Regulations D and J were revised to adopt a system of reserve requirements against demand deposits of all member banks based on the amount of such deposits held by a member bank. This change reduced required reserves by approximately $2.5 billion.

The Federal Reserve's ability to adjust the reserve requirement allows it to effectively manage the country's monetary policy and maintain a stable financial system.

FISA's Legality: Is It Constitutional?

You may want to see also

Explore related products

![]()

Banks can borrow from the Fed's discount window

There are three types of discount window credit available to depository institutions from their regional Federal Reserve Bank: primary credit, secondary credit, and seasonal credit. Each type of credit has its own interest rate, or "discount rate", which is established by each Reserve Bank's board of directors and is subject to review and determination by the Board of Governors of the Federal Reserve System.

Primary credit serves as the principal safety valve for ensuring adequate liquidity in the banking system. It is available to depository institutions that are in generally sound financial condition, and there are no restrictions on the use of funds borrowed under primary credit. Secondary credit is available to institutions that are not eligible for primary credit and is typically extended on a very short-term basis, usually overnight, and at a higher rate than the primary credit rate. There are restrictions on the use of secondary credit extensions, and it is available to meet backup liquidity needs when its use is consistent with a timely return to market sources of funding.

Despite the benefits of the discount window, there has been a long-standing stigma that discourages banks from borrowing from the Fed. The label of "lender of last resort" conveys desperation, and banks fear that borrowing from the discount window will make them look weak. This stigma has persisted despite efforts by the Fed to encourage borrowing, such as lowering interest rates and providing other avenues for banks to borrow.

In conclusion, while the Fed's discount window is meant to provide stability to the banking system, banks often try to avoid borrowing from it due to the negative perception associated with it. This has led to calls for reform to make the discount window a more effective tool for ensuring financial stability.

Understanding White Blood Cells in Our Blood

You may want to see also

Explore related products

![]()

Banks earn interest on excess reserves

Banks are required to hold reserves equal to a percentage of their net transactions. These reserves are kept in case of unexpected demands, such as large withdrawals, and to prevent panic. In the US, the Federal Reserve dictates the amount of cash, called the reserve ratio, that each bank must maintain. The reserve ratio has historically ranged from 0% to 10% of bank deposits.

The Federal Reserve started paying interest on excess reserves in 2008. This was part of the Emergency Economic Stabilization Act of 2008, which aimed to boost demand for loans and stimulate the economy. The interest rate on excess reserves is called the IOER rate. The IOER rate and the primary credit rate (the rate at which the Fed lends to banks) create a corridor in which the funds rate trades. This minimises the chances of deviations between the actual and target funds rates.

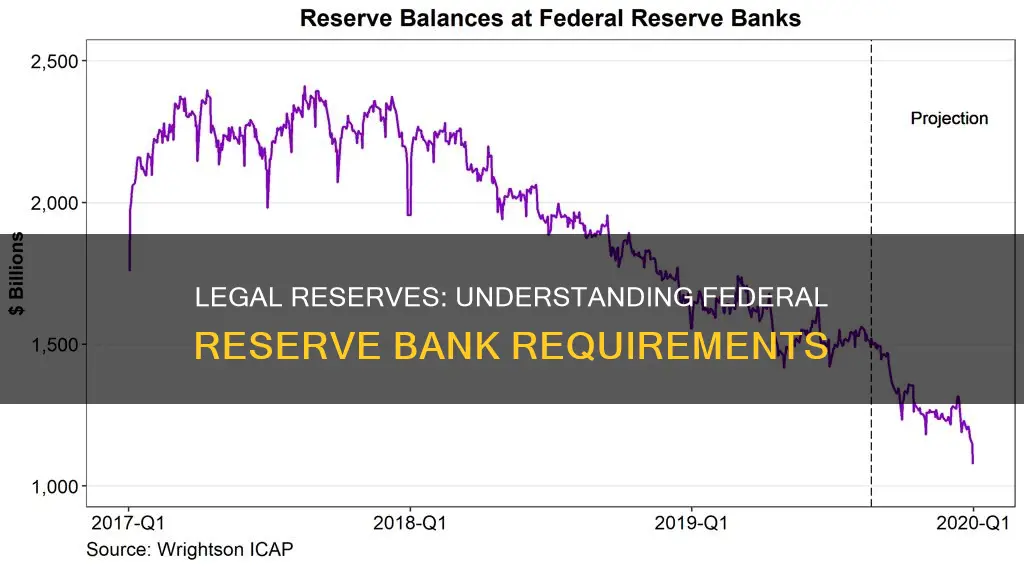

The amount of excess reserves held by banks has varied over time. In 2008, the opportunity cost of holding excess reserves was eliminated as banks could not earn anything by lending them out. This, along with the increased demand for liquidity, led banks to start accumulating excess reserves, which rose to over $800 billion by the end of 2008. Excess reserves hit a record $2.7 trillion in August 2014 due to quantitative easing (QE) payouts. Between January 2019 and February 2020, excess reserves ranged between $1.3 trillion and $1.6 trillion. In March 2020, the Federal Reserve eliminated requirements for US banks to hold reserves, dropping the required reserve ratio to zero.

Understanding the Constitution's Intent

You may want to see also

Frequently asked questions

Bank reserves are the cash minimums that financial institutions must have on hand to meet central bank requirements. They are kept to prevent panic in the event that customers discover that a bank doesn't have enough cash to meet immediate demands.

The reserve requirement is the percentage of cash that banks must keep in reserve and are not allowed to lend. It is one of the tools the Fed has to control liquidity in the financial system. By reducing the reserve requirement, the Fed is executing an expansionary monetary policy, and when it raises the requirement, it's exercising a contractionary monetary policy.

The reserve requirement is currently set at 0% as a response to the COVID-19 pandemic. Prior to the pandemic, the reserve requirement ranged from 0-10%.

The Federal Reserve System was designed to prevent or minimize the occurrence of bank runs and possibly act as a lender of last resort when a bank run does occur. By obliging banks to hold a certain amount of cash in reserve, the Federal Reserve ensures that banks never run short and have to refuse a customer's withdrawal, possibly triggering a bank run.