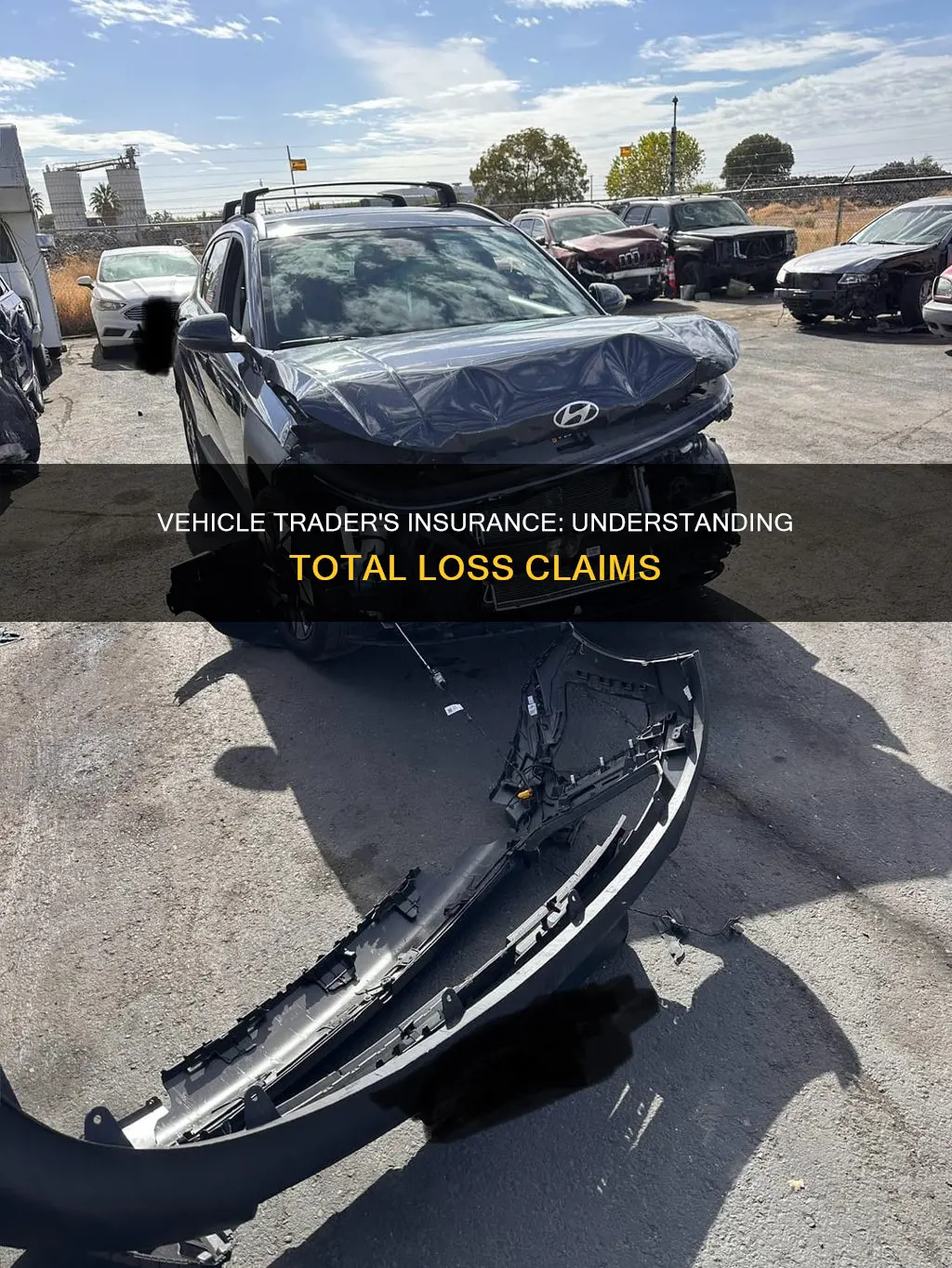

When a vehicle is damaged, insurance companies will decide whether to pay for repairs or declare the vehicle a total loss. A car is considered a total loss when the cost of repairing the damage exceeds the vehicle's value, or when it is deemed unsafe to drive even after repairs. In the event of a total loss, the insurer will reimburse the owner for the vehicle's actual cash value (ACV) or fair market value, minus any deductibles and fees. Each state has its own regulations and formulas for determining when a car is a total loss, and insurance companies may use different methods to calculate the ACV. Understanding these factors is crucial when dealing with vehicle traders insurance, as it involves higher stakes due to the nature of the business.

| Characteristics | Values |

|---|---|

| When a vehicle is deemed a total loss | When the cost to repair the damage exceeds the vehicle's book value at the time of the incident. Each state has its own threshold for declaring a vehicle a total loss. |

| What the insurance company pays | The pre-accident market value of the vehicle, adjusted for depreciation, mileage, and condition. |

| What happens to the vehicle after it's deemed a total loss | The insurance company may take the car and sell it to a shop to be repaired or rebuilt. The car will then receive a salvage title. |

| What happens if you want to keep the vehicle | You can keep the vehicle and repair it yourself if your state allows it. However, it may be harder to sell or insure the vehicle in the future. |

| How to calculate the total loss value | The total loss formula is the vehicle's fair market value less its salvage value. |

| Total loss coverage | Full coverage policies, including collision and comprehensive insurance, will help pay for damage to the vehicle and may cover the cost of a totaled car. |

Explore related products

What You'll Learn

![]()

Total loss threshold

The total loss threshold is the percentage of a car's market value that, when reached, results in a vehicle being declared a total loss. This threshold varies by state and insurance company.

When determining whether a vehicle is a total loss, insurance companies consider the cost to repair the damage relative to the vehicle's book value at the time of the incident. If the cost to repair exceeds the vehicle's value, the insurance company will declare it a total loss. This is referred to as the "total loss formula".

Insurers may also deem a vehicle a total loss if it would still be unsafe to drive even after repairs are made. In such cases, the insurer will reimburse the owner for the vehicle's actual cash value (ACV) or fair market value immediately before the loss occurred, minus any deductible and other fees.

To calculate the ACV, depreciation is subtracted from the cost to replace the car. Factors such as mileage, condition, and market demand can influence depreciation and, consequently, the ACV.

It is important to note that the rules and regulations covering total loss vehicles vary by insurance company and state.

Founders Who Shaped the Constitution

You may want to see also

Explore related products

$33.98 $49.99

$86.53 $119

$6.99

![]()

Total loss formula

A total loss vehicle is when the cost of repairing a damaged vehicle is more than the vehicle's worth. This is also referred to as "totaling" a car.

The total loss formula (TLF) is used to calculate the vehicle's fair market value less its salvage value. The formula is often abbreviated as TLF and is a calculation that insurers use to determine whether the cost of repairing a damaged vehicle is more than they are willing to take on. When the cost of repairs is higher than a certain percentage of the vehicle's actual cash value (ACV), it's typically determined to be a total loss.

The exact formula and percentage vary by insurance company and jurisdiction. Each state has its own total loss threshold, which could be a certain percentage or the total loss formula. The type of insurance coverage that applies in the event of a total loss depends on the circumstances of the loss.

The first step in calculating the total loss value of a vehicle is to appoint an adjuster to inspect the vehicle's condition. The adjuster assesses the mechanical and physical condition of the vehicle and determines whether to repair it or not. Following this inspection, the adjuster evaluates the ACV of the vehicle after considering factors such as depreciation and the car's market demand. The ACV is calculated by subtracting depreciation from the cost to replace the car. Factors like mileage, condition, and market demand can influence depreciation.

After a mechanic provides an estimate of the repair cost, the insurance company considers the data and compares the repair cost to the value of the car. If the repair cost is more than the value of the car, the insurance company will rule it a total loss.

Constitution Evolution: Versions of Pennsylvania's Constitution

You may want to see also

Explore related products

![]()

Actual cash value

When a vehicle is deemed a total loss, insurance companies will reimburse the owner for the vehicle's actual cash value (ACV) or its fair market value before the incident occurred. This value includes a deduction for depreciation and is usually less than the original cost of the vehicle, even if it is relatively new.

ACV is calculated by subtracting depreciation from the cost to replace the car. Factors such as mileage, condition, wear and tear, accident history, and market demand can influence depreciation. The make, model, year, and vehicle options can also affect how much a car depreciates, as some vehicles hold their value better than others.

The threshold for "total loss" varies by state and insurer, but it generally occurs when the cost of repairing the vehicle exceeds a certain percentage of its ACV. In some states, a vehicle is considered a total loss if the sum of repair costs and scrap value surpasses the vehicle's pre-accident market value.

If you disagree with the insurance company's valuation of your vehicle, you can negotiate a higher payout by presenting evidence of your car's value. An independent appraisal is recommended, as insurance appraisers may undervalue your car to reduce the payout.

Defining Bedrooms: Real Estate's Burning Question

You may want to see also

Explore related products

![Mortuary / Salvage / Memory [Blu-ray]](https://m.media-amazon.com/images/I/91jm0Smu0UL._AC_UL320_.jpg)

![]()

State-specific regulations

Each state has its own regulations and thresholds for determining when a car is considered a total loss. These thresholds are typically based on a specific percentage of the car's market value or a total loss formula (TLF). For example, in Iowa, state law requires that an insurance company declare a vehicle as "salvaged" or totalled if the repair costs exceed 50% of the vehicle's pre-crash value. Other states have higher thresholds, with many set at 75%.

Insurance companies will typically pay the pre-crash market value minus any deductible and fees when a vehicle is deemed a total loss. This is known as the Actual Cash Value (ACV) or fair market value, which takes into account depreciation, mileage, condition, and demand in the used car market. In some states, insurance companies may also be required to pay for sales tax, transfer fees, and title fees if you purchase a new vehicle within a certain time frame after receiving a cash settlement.

In certain states, such as Illinois, specific regulations may apply to total loss vehicles. For instance, the Illinois Vehicle Code does not permit vehicle owners to retain the salvage once the insurance company has deemed the vehicle a total loss, except in specific circumstances, such as hail damage that does not affect the vehicle's operational safety.

It is important to note that the rules and regulations covering totalled vehicles can vary not only by state but also by insurance company. Therefore, it is essential to carefully review your insurance policy and understand your rights and responsibilities in the event of a total loss claim.

If you disagree with your insurance company's valuation of your totalled vehicle, you may consider filing a complaint with your state's department of insurance. However, this process can be lengthy and complicated, and it may be wise to seek legal advice or consult with a car accident lawyer who is knowledgeable about the specific regulations in your state.

Trump's Radical Plan: End the Constitution?

You may want to see also

Explore related products

![]()

Total loss claims process

The total loss claims process can be daunting, but understanding the steps involved can help streamline the experience. Here is a detailed guide to help you navigate the process:

Understanding Total Loss Criteria

Before initiating the claims process, it's important to understand what constitutes a total loss. Insurance companies declare a vehicle a total loss when the cost to repair the damage exceeds the vehicle's book value or actual cash value (ACV) at the time of the incident. The ACV is calculated by considering factors such as depreciation, mileage, condition, and market demand. Each state has its own criteria and thresholds for declaring a vehicle a total loss, so be sure to familiarize yourself with the regulations in your specific state.

Initiating the Claims Process

In the unfortunate event of a total loss, the first step is to promptly report the incident to your insurance company. Depending on the situation, you may also need to report it to the police, such as in cases of theft or vandalism. Once reported, the insurance company will assign a claims adjuster to assess the vehicle's value, considering factors such as damages, depreciation, market value, and any relevant documentation you provide.

Understanding Your Options

After the insurance company has assessed the total loss, you have several options to consider:

- Accepting a Settlement: You can choose to accept a settlement from your insurance company, which will typically be the ACV of your vehicle. This may involve negotiating with the insurer if you believe your car was worth more than their assessed value.

- Keeping Your Vehicle: In some states, you may have the option to keep your vehicle and repair it yourself. However, it's important to note that a vehicle with a salvage title may be harder to sell or insure in the future.

- Receiving a Replacement Vehicle: Your insurance company may offer to replace your vehicle with a comparable make and model of similar or better condition. They are required to purchase the replacement vehicle through licensed dealers, and it must meet specific age and warranty requirements.

Finalizing the Settlement

Once you have agreed on a settlement amount, the insurance company will make the payment, taking into account any deductibles, fees, and applicable taxes. If you choose to purchase or lease a new vehicle within a certain timeframe (often specified in your insurance policy), the insurance company may also cover sales tax, transfer fees, and title fees associated with the new vehicle.

Understanding Deductions and Adjustments

Insurance companies may make deductions from the settlement amount for various factors, including the vehicle's salvage value, unrepaired collision damages, wear and tear, missing parts, and rust. These deductions are typically itemized and specified in dollar amounts. Additionally, if you have rental car reimbursement coverage as part of your policy, your insurer may help cover rental car costs during this process.

Remember, it's important to carefully review your insurance policy to understand your specific coverages, rights, and responsibilities during the total loss claims process. The process may vary depending on your insurance provider and the state in which you reside.

Organizing Principles: The Constitution's Foundation

You may want to see also

Frequently asked questions

A total loss vehicle is one that costs more to repair than its value, or cannot be repaired at all.

Insurance companies calculate the value of a total loss vehicle by determining its actual cash value (ACV). ACV is calculated by subtracting depreciation from the cost to replace the car. Factors like mileage, condition, and market demand can influence depreciation.

If your vehicle is declared a total loss, the insurance company will reimburse you for the fair market or book value of the vehicle before the loss occurred, minus your deductible and any other fees.

If you want to keep your total loss vehicle, you may be able to do so depending on your state's regulations. However, it may be harder to insure or sell the vehicle in the future.

If you have rental car reimbursement coverage as part of your policy, your insurer can help pay for rental car costs after your vehicle is declared a total loss.

![Exploring Third Spaces in [Discipline]: Definition and Examples](/images/resources/what-constitutes-a-third-space-in-the-discipline-you-teach_20250617073816.webp)