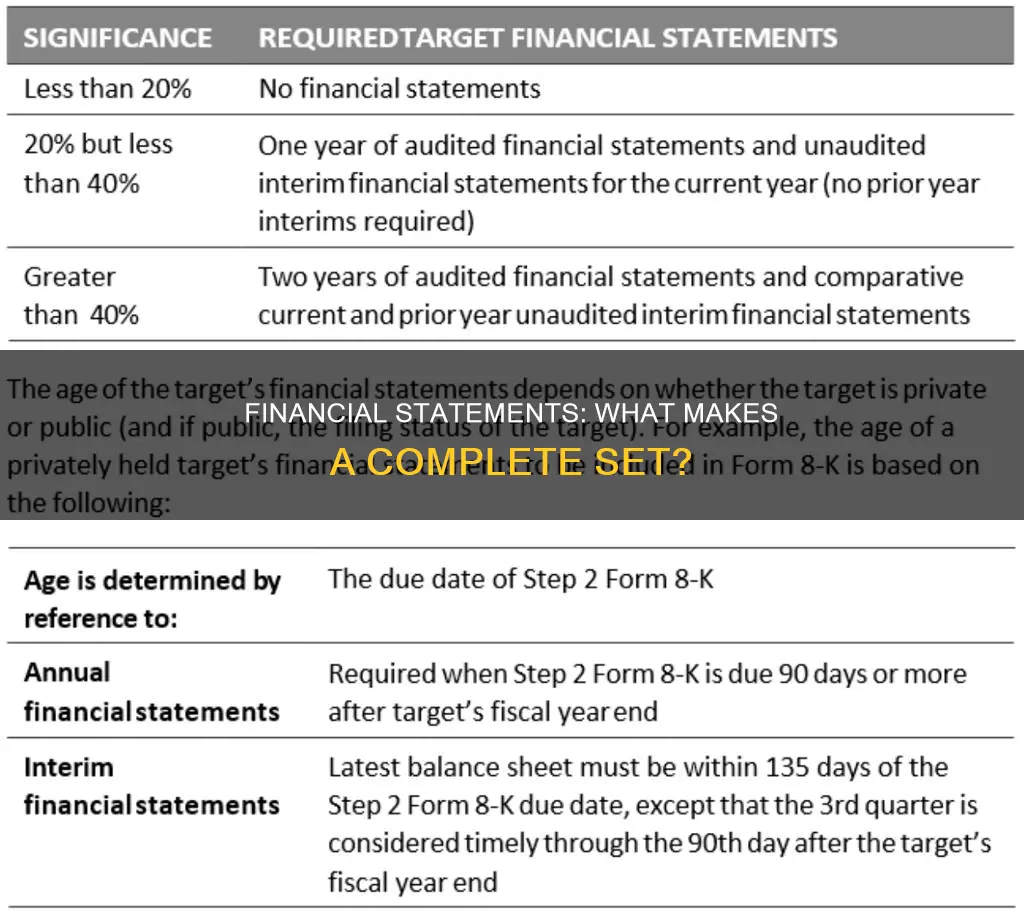

Financial statements are formal records that provide an overview of a company's financial health. They are specific reports generated by an entity's accounting system, which summarize a company's financial performance and position. There are four primary types of financial statements: balance sheet, income statement, cash flow statement, and statement of shareholders' equity. These statements are prepared by accountants following specific accounting rules, such as the Generally Accepted Accounting Principles (GAAP) or the International Financial Reporting Standards (IFRS). A complete set of financial statements typically includes components such as a statement of comprehensive income, statement of changes in equity, balance sheet, statement of cash flows, and notes to the financial statements. These statements provide valuable insights into a company's financial position, operations, and performance, allowing stakeholders to make informed decisions about the company's stability and future potential.

| Characteristics | Values |

|---|---|

| Number of primary types of financial statements | 4 |

| Types of financial statements | Balance sheet, Income statement, Cash flow statement, Statement of shareholders' equity |

| Purpose of financial statements | To provide an overview of a company's financial health to stakeholders |

| What do financial statements show | Where a company's money came from, where it went, and where it is now |

| What does a balance sheet show | What a company owns and owes at a fixed point in time |

| What does an income statement show | How much money a company made and spent over a period of time |

| What does a cash flow statement show | The exchange of money between a company and the outside world over a period of time |

| What does a statement of shareholders' equity show | Changes in the interests of the company's shareholders over time |

| What does a statement of comprehensive income show | A subtotal of items recognised in determining profit or loss followed by other items of comprehensive income |

| What does a statement of changes in equity show | The balance of the capital account at the beginning of the period, the changes that occurred during the period, and the ending balance as a result of such changes |

| What does a statement of cash flows show | The beginning balance of cash, the changes that occurred during the period, and the cash balance at the end of the period as a result of the changes |

Explore related products

What You'll Learn

![]()

Balance sheet

A balance sheet is a financial statement that provides a snapshot of a company's financial position at a specific point in time, usually at the end of the reporting period. It lists a company's assets, liabilities, and shareholder equity, adhering to the accounting equation: Assets = Liabilities + Equity. Assets are what a company owns and are categorised as either current or non-current assets. Liabilities are financial and legal obligations to pay an amount to a debtor and are typically tallied as negatives (-) in a balance sheet. They are categorised as current or non-current liabilities, with the former referring to any liability due within a year. Non-current liabilities, or long-term liabilities, include long-term debt, future tax payments, employee retirement benefit obligations, and long-term lease commitments.

The balance sheet is an invaluable piece of information for investors, analysts, and business owners, as it provides critical insight into the health of a company. It helps determine risk and is used to secure capital, such as business loans or private equity funding. It also serves as the basis for computing rates of return for investors and evaluating a company's capital structure.

However, the balance sheet has its limitations. Its narrow scope in time, capturing only a specific day, can make it challenging to determine a company's performance without additional context or comparative points. To overcome this, the balance sheet should be compared with other statements and sheets from previous periods. For example, the income statement and statement of cash flows provide valuable context for assessing a company's finances.

Overall, the balance sheet is a crucial component of financial statements, offering a summary of a company's financial position by breaking it down into assets, liabilities, and shareholder equity. It is a valuable tool for assessing a company's financial health, risk, and capital structure.

Constitution's Civil War Setup: Understanding the Conflict's Roots

You may want to see also

Explore related products

![]()

Income statement

An income statement, also known as a profit and loss (P&L) statement, is a vital tool in financial reporting and one of the most common and critical statements encountered by investors and business owners. It is one of a company's core financial statements that show their profit and loss over a period of time. Income statements are often shared as quarterly and annual reports, showing financial trends and comparisons over time.

An income statement summarizes all income and expenses over a given period, including the cumulative impact of revenue, gain, expense, and loss transactions. It answers the question: "Did the company make money?" It provides a glimpse into which business activities brought in revenue and which cost the organization money. It also helps determine a company's current financial health, predict future opportunities, decide on business strategy, and create meaningful team goals.

Within an income statement, you’ll find all revenue and expense accounts for a set period. Accountants create income statements using trial balances from any two points in time. The statement displays the company’s revenue, costs, gross profit, selling and administrative expenses, other expenses and income, taxes paid, and net profit in a coherent and logical manner.

The income statement is divided into time periods that logically follow the company’s operations. The most common periodic division is monthly (for internal reporting), although certain companies may use a thirteen-period cycle. These periodic statements are aggregated into total values for quarterly and annual results.

The income statement may have minor variations between different companies, as expenses and income will be dependent on the type of operations or business conducted. However, there are several generic line items that are commonly seen in any income statement.

Why India's Constitution is the Lengthiest

You may want to see also

Explore related products

$13.77 $22.95

![]()

Cash flow statement

A cash flow statement is one of the four primary types of financial statements, the others being the balance sheet, income statement, and statement of shareholders' equity. It is a financial report that details how cash entered and exited a business during a reporting period. This statement is different from a balance sheet, which shows the assets and liabilities a business owns and owes, respectively.

The cash flow statement is a crucial financial statement that provides an overview of a company's financial health to stakeholders, including board members, investors, shareholders, creditors, employees, customers, and analysts. It is a valuable tool for business owners, managers, and company stakeholders to understand their company's value, overall health, and financial position, and to guide financial decision-making.

A typical cash flow statement is divided into three sections: cash flow from operating activities, cash flow from investing activities, and cash flow from financing activities. The first section, cash flow from operating activities, covers the company's net income and reconciles all non-cash items to cash items involving operational activities. It includes cash inflows and outflows directly related to the company's main business activities, such as buying and selling inventory and supplies, paying employee salaries, and accounts payable.

The second section of the cash flow statement examines cash inflows and outflows related to investing activities. This includes cash flows from the sale or purchase of long-term assets, such as property, buildings, or equipment. The third section focuses on cash inflows and outflows related to financing activities, including cash flows from debt and equity financing. This section also includes dividends paid, interest paid, and payments made to investors and creditors.

There are two main methods for calculating cash flow: the direct method and the indirect method. The direct method involves recording cash as it enters and leaves the business, and then using that information to prepare a statement of cash flow at the end of the month. This method is more time-consuming and requires more legwork as it necessitates producing and tracking cash receipts for every cash transaction. The indirect method, on the other hand, starts with net income from the income statement and makes adjustments to "undo" the impact of accruals during the reporting period. This method is generally preferred by small businesses as it is faster and more closely linked to the balance sheet. Both methods are accepted by Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

A President's Term: Time in Office Explored

You may want to see also

Explore related products

![]()

Statement of shareholders' equity

A complete set of financial statements is made up of five components: the Statement of Comprehensive Income, Statement of Changes in Equity (also known as the Statement of Shareholders' Equity), Balance Sheet, Statement of Cash Flows, and Notes to Financial Statements.

The Statement of Shareholders' Equity is one of the primary types of financial statements. It provides a detailed breakdown of the changes in a company's ownership stake over a specific period. It is an essential tool for assessing the financial health of a business. Shareholders' equity is the value of a company's assets left for shareholders after the company pays all of its liabilities. It is the total amount of assets that a company would retain if it paid all of its debts.

The four primary components of a Statement of Shareholders' Equity are:

- Share capital: The total amount of money a company has raised by issuing shares of stock, including common stock and preferred stock.

- Net income: The profit or loss generated by the company's operations during a specific period, representing additional earnings retained by the company.

- Dividends: Payments made to shareholders from the company's profits, representing a distribution of earnings.

- Retained earnings: The portion of a company's net income that is retained and not distributed as dividends, which is then reinvested into the business to fund growth and future projects.

To create a Statement of Shareholders' Equity, you must first gather financial information, including the company's beginning equity balance, new investments, net income/loss, dividends paid, and other adjustments. Next, add new equity contributions, including any additional investments made by shareholders or owners. Then, add net income or subtract net loss based on the company's profitability. Reduce the balance by the amount of dividends paid to shareholders. Finally, add or subtract other adjustments, accounting for other non-routine transactions like stock repurchases or issuances.

Texas Constitution: What are its Major Flaws?

You may want to see also

Explore related products

![]()

Statement of comprehensive income

A complete set of financial statements is made up of five components: the Statement of Comprehensive Income, Statement of Changes in Equity, Balance Sheet, Statement of Cash Flows, and Notes to Financial Statements.

The Statement of Comprehensive Income is a financial statement that summarises both standard net income and other comprehensive income (OCI). The net income is the result obtained by preparing an income statement. Net income accounts for a company's total revenues and expenses. It is calculated by subtracting the cost of goods sold (COGS), general expenses, taxes, and interest from total revenue.

Other comprehensive income, on the other hand, includes all unrealised gains and losses on assets that are not reflected in the income statement. These unrealised gains and losses can include those from available-for-sale investments, cash flow hedges, debt securities, and foreign currency translation adjustments.

The statement of comprehensive income is particularly useful for company management and investors as it provides a fuller, more accurate idea of income. It is also important for investors who can use it to help make decisions about the feasibility of potential investments. The statement can be presented in a single statement or two consecutive statements.

The US Constitution: A Global Perspective

You may want to see also

Frequently asked questions

Financial statements are formal records that summarise a company's financial performance and position, providing a clear picture of its financial health. They are reports compiled to record financial performance and health.

A complete set of financial statements is made up of 5 components: Statement of Comprehensive Income, Statement of Changes in Equity (or Capital), Balance Sheet, Statement of Cash Flows, and Notes to Financial Statements.

The Balance Sheet provides a snapshot of a company's assets, liabilities, and shareholder equity at a specific point in time. The Income Statement shows revenues, expenses, net income, and earnings per share over a specified period. The Cash Flow Statement shows the exchange of money between a company and the outside world over a period of time, divided into operating, investing, and financing activities. The Statement of Shareholders' Equity shows changes in the interests of shareholders over time.