In a perfectly competitive market, firms are direct competitors, selling identical products and operating with low barriers to entry and exit. In the short run, firms aim to cover variable costs with revenue, and the market supply curve is derived from the sum of individual firms' marginal cost curves. However, in the long run, firms earn zero economic profit as price equals average total cost, resulting in a perfectly elastic supply curve. This equilibrium ensures that firms enter or exit the market based on profitability, maintaining a balance between supply and demand. The long-run supply curve of a competitive firm is the portion of the marginal cost curve that lies above the average total cost, indicating the output level at which the firm can maximise profit given the market price.

| Characteristics | Values |

|---|---|

| Market supply curve | Sum of individual firms' marginal cost curves |

| Long-run supply curve | A flat horizontal line in a constant-cost industry |

| Long-run supply curve | Downward-sloping in a decreasing-cost industry |

| Long-run | A period where firms enter and exit the market |

| Short-run | A period where supply can be changed by changing variable factors |

| Long-run | Firms can vary all their input factors |

| Short-run | Firms aim to cover variable costs with revenue |

| Long-run | Firms aim to cover average total costs with revenue |

| Long-run | Firms earn zero economic profit |

| Short-run | Firms earn positive economic profit |

| Long-run | Firms produce only if the price is more than the average total cost |

| Long-run | Firms produce at the output level to maximise profit |

Explore related products

What You'll Learn

- The long-run supply curve of a competitive firm is the portion of the marginal cost curve that lies above the average total cost

- Firms in a perfectly competitive market are price takers

- The long-run is a period where many firms enter and exit the market

- The long-run supply curve is a diagram that helps us understand the long-run price of a product or service

- The long-run supply curve is found by examining the responsiveness of short-run market supply to a change in market demand

![]()

The long-run supply curve of a competitive firm is the portion of the marginal cost curve that lies above the average total cost

A competitive firm's long-run supply curve is a critical concept in economics, and it is defined by the portion of the marginal cost curve that exceeds the average total cost. This concept is integral to understanding a firm's decision-making process regarding production and pricing in a competitive market.

The marginal cost curve represents the additional cost incurred by a firm when producing one more unit of output. In other words, it shows how much a firm's total costs increase as they produce more. Typically, the marginal cost curve rises as output increases, reflecting the principle of increasing marginal costs.

On the other hand, the average total cost (ATC) refers to the total cost per unit of output. In the long run, firms aim to set their prices higher than the ATC to ensure they make a normal profit. If the price is less than the ATC, firms will incur losses, and they may choose to exit the industry or adjust their production methods to reduce costs.

In a perfectly competitive market, firms are direct competitors, sell identical products, and face low barriers to entering and exiting the market. The long run is a period when numerous firms can enter or exit the market. During this time, firms can vary all their input factors, including fixed ones, which can cause fluctuations in market prices.

The long-run supply curve of a competitive firm, therefore, represents the portion of the marginal cost curve that is above the ATC. This ensures that firms are making a normal profit and covers their total costs. If the marginal cost is below the ATC, firms may choose not to produce or supply that particular good or service.

Crafting a Preamble: Constitution Edition

You may want to see also

Explore related products

![]()

Firms in a perfectly competitive market are price takers

A perfectly competitive market is one where firms are direct competitors, selling identical products, and operating in a market with low entry and exit barriers. In such a market, firms are price takers, meaning they have no power to influence the market price of their product or service.

Price takers are individuals or companies that must accept prevailing market prices, lacking the market share to influence prices on their own. In a perfectly competitive market, all participants are price takers. This is because, in a perfectly competitive market, there are many sellers, and products are identical. If a firm in a perfectly competitive market is unhappy with the price and raises it, even by a small amount, it will lose all its sales to competitors.

For example, in agricultural markets, the same crops that different farmers grow are largely interchangeable. A corn farmer who attempted to sell at a higher price than the market rate would not find any buyers.

In the long run, firms in a perfectly competitive market earn zero economic profit as price equals average total cost, leading to a perfectly elastic supply curve. This equilibrium ensures that firms enter or exit the market based on profitability, maintaining a balance where demand is met without excess supply or demand.

Montesquieu's Influence: US Constitution's Foundation

You may want to see also

Explore related products

![]()

The long-run is a period where many firms enter and exit the market

In a perfectly competitive market, firms are direct competitors, sell identical products, and operate with low entry and exit barriers. This means that in the long run, numerous firms can enter and exit the market.

In the short run, firms aim to cover their variable costs with earned revenue. They will supply commodities until the price is greater than or equal to the average variable cost. In the long run, however, firms can vary all of their input factors, including fixed ones. This allows for the possibility of new firms entering the market and existing firms exiting.

For example, if existing firms are earning positive economic profits, new firms will be tempted to enter the market. Conversely, if existing firms are earning losses, they may choose to leave. Therefore, the number of firms in a perfectly competitive market is unlikely to remain unchanged in the long run.

The long-run supply curve of a competitive firm is the portion of the marginal cost curve that lies above the average variable cost. This ensures that firms only produce when they can cover their variable costs and make a profit. In the long run, firms will earn zero economic profit as price equals average total cost (P = ATC), leading to a perfectly elastic supply curve.

Hamilton's Role: Did He Help Write the US Constitution?

You may want to see also

Explore related products

![]()

The long-run supply curve is a diagram that helps us understand the long-run price of a product or service

In economics, the long-run supply curve is a diagram that helps illustrate and understand the long-run price of a product or service in a particular industry. It is a useful tool for understanding market structures and competition.

The long-run supply curve is a representation of the relationship between price and quantity supplied. It shows the quantities that a seller is willing to sell at different prices. In a perfectly competitive market, firms are price takers, meaning they cannot influence the market price of a product or service. Therefore, the price is given by the intersection of the market demand and supply curves.

The long-run supply curve of a competitive firm is defined by the portion of the marginal cost curve that lies above the average total cost. Firms will only produce if the price is more than the average total cost, allowing them to earn a normal profit. If the price is less than the average total cost, firms will incur losses and may choose to leave the industry or adjust their production to reduce costs.

In the long run, firms can vary all their input factors, and new firms can enter the market, while some existing firms may exit. This dynamic nature of the market makes it challenging to determine the shape of the long-run supply curve in a perfectly competitive market.

The long-run supply curve is found by examining the responsiveness of short-run market supply to changes in market demand. It is important to note that the long-run supply curve is not a simple lateral summation of the short-run supply curves. Instead, it depends on the change in the optimum size of firms and the number of firms in the market.

Flesh Sacrifice: Permanent Solution to Constitution Issues?

You may want to see also

Explore related products

![]()

The long-run supply curve is found by examining the responsiveness of short-run market supply to a change in market demand

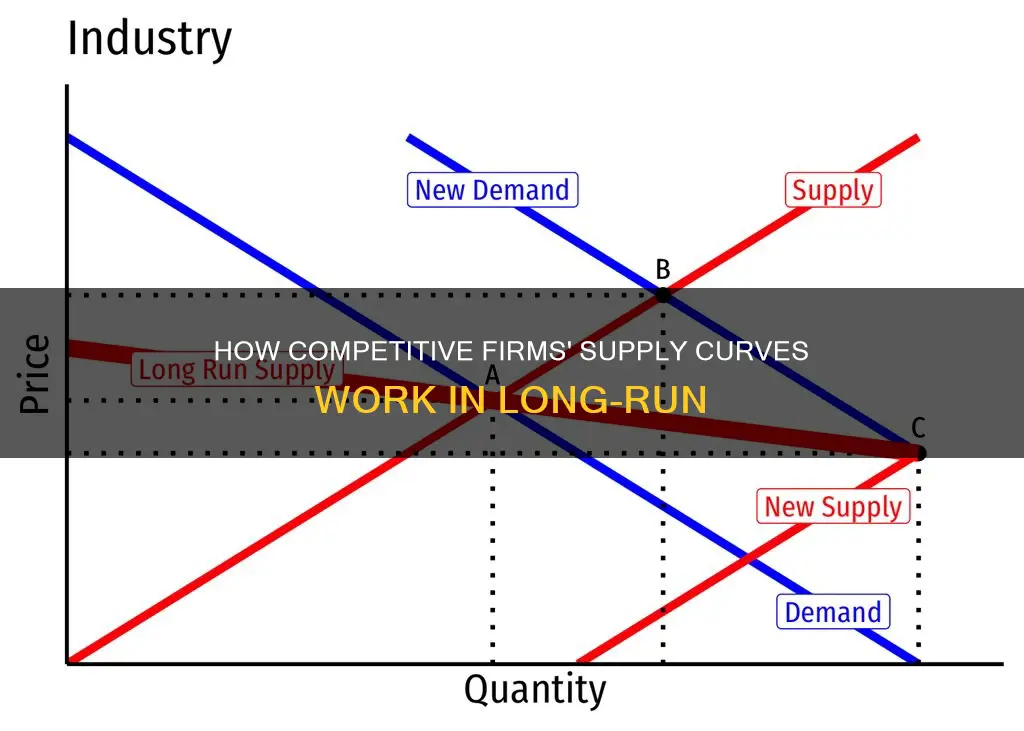

In a perfectly competitive market, firms are direct competitors, sell identical products, and operate in a market with low entry and exit barriers. In the short run, the market supply curve is derived from the sum of individual firms' marginal cost curves, reflecting their willingness to supply at various prices.

The short-run market supply curve is the horizontal summation of all individual firms' supply curves. It is similar to the supply and demand concept, where the marginal cost curve is the supply curve when there is a supply. For example, at a price of $5, a firm may supply 100 units, and at a price of $10, it may supply 200 units.

The long-run market supply curve is found by examining the responsiveness of short-run market supply to a change in market demand. In the long run, firms can vary all their input factors, and new firms can enter the market, causing the short-run market supply to shift and the market price to adjust. For instance, an increase in demand from D1 to D2 results in a new, higher market price of P2. In the short run, existing firms will earn positive economic profits, but in the long run, new firms will enter, shifting the supply curve and driving the market price back down to P1.

In the long run, firms earn zero economic profit as price equals average total cost (P = ATC), leading to a perfectly elastic supply curve. This equilibrium ensures that firms enter or exit the market based on profitability, maintaining a balance where demand is met without excess supply or demand.

Jefferson's Influence: French Constitution Co-Author?

You may want to see also

Frequently asked questions

A supply curve shows the relationship between price and quantity supplied. It indicates the quantities that a seller is willing to sell at different prices.

In the short run, supply can be changed by changing variable factors, while fixed factors remain the same. In the long run, firms can vary all of their input factors.

In a competitive market, firms are price-takers, meaning they cannot influence the market price of a product or service. The long-run supply curve of a competitive firm is the portion of the marginal cost curve that lies above the average total cost. This ensures that firms only produce when they can cover their variable costs and make a profit.

The long-run supply curve in a perfectly competitive market is influenced by fluctuations in the market price, which are caused by the entry and exit of firms. In the long run, firms can vary all their input factors, including fixed ones, which leads to changes in the market price.