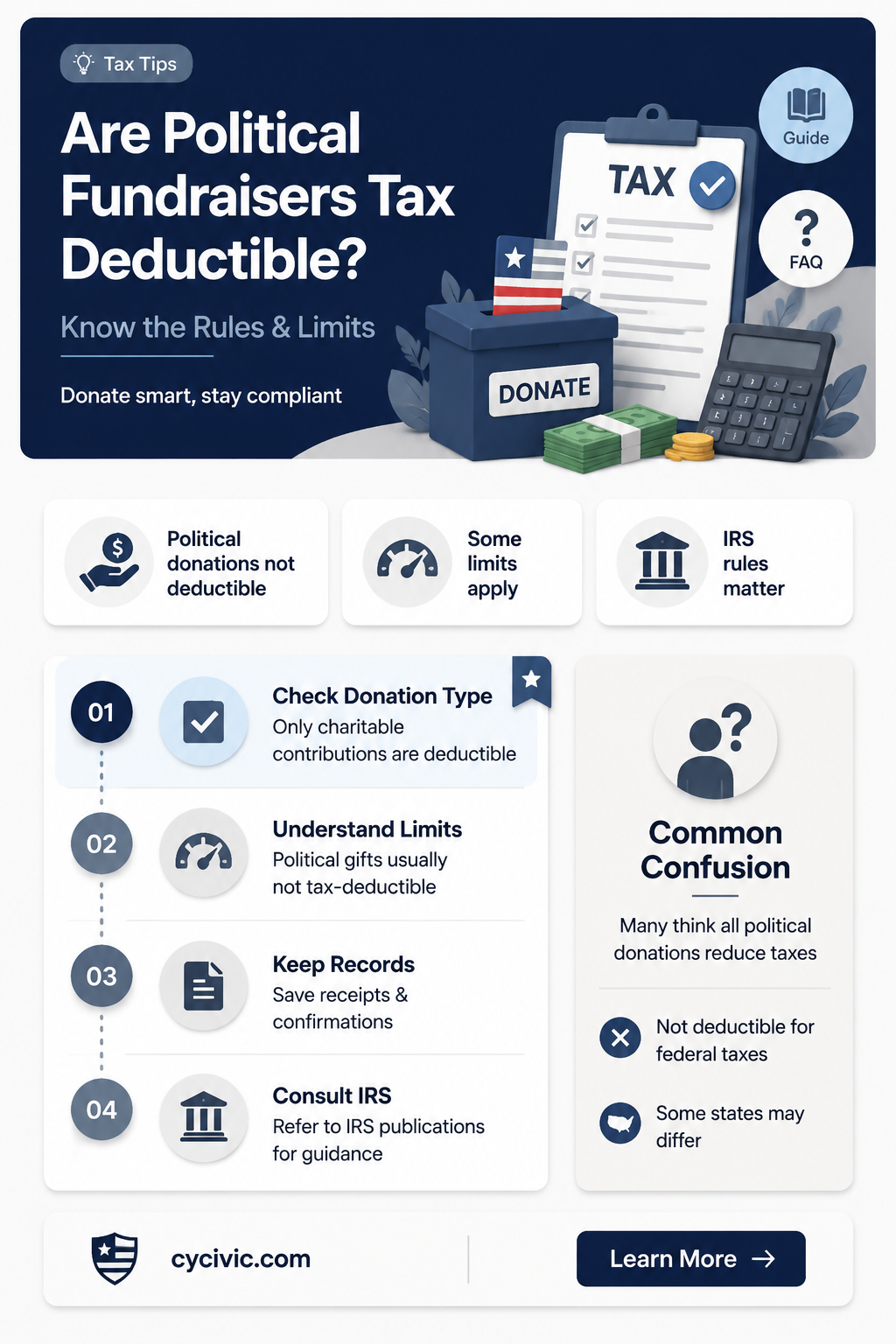

Political fundraisers are a common aspect of the political landscape, often serving as a means for candidates and organizations to gather financial support for their campaigns. A frequently asked question among donors is whether contributions made to these fundraisers are tax deductible. In general, donations to political campaigns, parties, or candidates are not tax deductible under U.S. federal tax laws, as they are considered personal expenses rather than charitable contributions. However, certain exceptions may apply, such as donations to political organizations with a charitable arm or contributions to educational or research-focused political groups that qualify as tax-exempt under section 501(c)(3) of the Internal Revenue Code. Understanding the tax implications of political donations is crucial for donors to ensure compliance with tax regulations and to manage their financial contributions effectively.

| Characteristics | Values |

|---|---|

| Tax Deductibility | No, contributions to political parties, candidates, or PACs are not tax-deductible. |

| Applicable Law | IRS regulations under the U.S. Tax Code (26 U.S. Code § 162). |

| Reason for Non-Deductibility | Political contributions are considered personal expenses, not charitable donations. |

| Exceptions | None for direct political donations; however, donations to 501(c)(3) organizations (e.g., charities) may be deductible if not tied to political campaigns. |

| Related Expenses | Business-related lobbying expenses may be deductible under specific conditions, but not individual political donations. |

| State-Level Variations | Some states may allow deductions for political contributions, but federal tax rules do not. |

| Documentation Required | None, as political contributions are not eligible for tax deductions. |

| Impact on Tax Return | Political donations do not reduce taxable income or provide tax benefits. |

| Alternative Benefits | Donors may receive non-tax benefits, such as access to events or recognition, but no financial tax advantage. |

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

What You'll Learn

- IRS Rules on Political Donations: Understand IRS guidelines for tax-deductible political contributions

- (c)(3) vs. 501(c)(4): Differentiate tax-deductible charities from non-deductible political organizations

- Campaign Contributions: Direct candidate donations are not tax-deductible

- Political Action Committees (PACs): PAC donations are generally not tax-deductible

- Charitable Political Groups: Some political-related charities may offer tax deductions

![]()

IRS Rules on Political Donations: Understand IRS guidelines for tax-deductible political contributions

Political donations often feel like a civic duty, but can they also benefit your tax return? The IRS has clear guidelines on what qualifies as a tax-deductible political contribution, and understanding these rules is crucial to avoid surprises during tax season. Unlike charitable donations, which are generally tax-deductible, political contributions to candidates, parties, or political action committees (PACs) are not tax-deductible. This distinction is rooted in the IRS’s classification of political organizations, which are typically structured as 527 organizations or political committees, neither of which qualify for tax-deductible donations.

However, there’s a nuanced exception: donations to certain 501(c)(4) social welfare organizations or 501(c)(3) charitable organizations that engage in political activity *may* be tax-deductible, but only if the donation is used for non-political purposes. For example, a donation to a 501(c)(3) organization that supports voter education or civic engagement could be deductible, provided the funds are not earmarked for political campaigns or lobbying efforts. The key is to ensure the donation aligns with the organization’s charitable mission, not its political agenda.

To navigate this complexity, donors should request documentation from the organization confirming how their contribution will be used. If the funds are directed toward political activities, such as campaign advertising or candidate support, the donation is not deductible. Conversely, if the funds support non-political initiatives, such as community outreach or educational programs, the donor may claim a deduction. This requires diligence and clarity from both the donor and the organization.

A practical tip for donors is to review the IRS’s guidelines on Publication 526 (Charitable Contributions) and Publication 1828 (Tax Guide for Political Organizations) to ensure compliance. Additionally, donors should retain receipts and acknowledgment letters from the organization, clearly stating the purpose of the donation. While political contributions are a vital part of civic engagement, they should not be conflated with charitable giving for tax purposes. Understanding these distinctions ensures both financial prudence and legal compliance.

Troubleshooting Politico Notifications: Quick Fixes for Common Alert Issues

You may want to see also

Explore related products

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UL320_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UL320_.jpg)

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UL320_.jpg)

![]()

501(c)(3) vs. 501(c)(4): Differentiate tax-deductible charities from non-deductible political organizations

In the United States, the tax code distinguishes between organizations based on their purpose and activities, particularly when it comes to political involvement and tax-deductible donations. The key players in this distinction are 501(c)(3) and 501(c)(4) organizations, each with unique rules governing their operations and the tax benefits they offer to donors. Understanding these differences is crucial for both donors and organizations to ensure compliance and maximize financial benefits.

The 501(c)(3) Advantage: Tax-Deductible Charities

A 501(c)(3) organization is primarily charitable, religious, educational, or scientific in nature. These entities are prohibited from engaging in substantial lobbying or political campaign activities. Donations to 501(c)(3)s are tax-deductible for the donor, subject to certain limits (generally up to 60% of the donor’s adjusted gross income for cash contributions). For example, a donation to a food bank or a university qualifies for this deduction. However, if a 501(c)(3) crosses the line into political campaigning, it risks losing its tax-exempt status. Practical tip: Always verify an organization’s 501(c)(3) status using the IRS’s Tax Exempt Organization Search tool before claiming a deduction.

The 501(c)(4) Reality: Non-Deductible Political Organizations

In contrast, a 501(c)(4) organization is a social welfare group allowed to engage in political activities, including lobbying and campaign advocacy. Donations to 501(c)(4)s are not tax-deductible. These organizations often serve as vehicles for political fundraising, such as supporting a specific candidate or issue. For instance, contributions to a political action committee (PAC) or a grassroots advocacy group typically fall under this category. While 501(c)(4)s can promote social welfare, their primary focus on politics disqualifies them from offering tax benefits to donors. Caution: Donors should be aware that contributions to these groups, even if they align with their values, do not reduce their taxable income.

Key Differences in Action

Consider a scenario where two organizations advocate for environmental policy. A 501(c)(3) environmental nonprofit educates the public and conducts research, while a 501(c)(4) group lobbies Congress and campaigns for specific legislation. A donor contributing $1,000 to the 501(c)(3) can deduct the donation, but the same amount given to the 501(c)(4) provides no tax benefit. This distinction highlights the trade-off between political influence and financial incentives for donors.

Practical Takeaway

For donors, the choice between supporting a 501(c)(3) or a 501(c)(4) depends on their priorities: tax savings or political impact. Organizations must carefully structure their activities to maintain compliance with IRS rules. For example, a 501(c)(3) can create a separate 501(c)(4) arm to handle political work, ensuring the parent organization retains its tax-deductible status. By understanding these nuances, both parties can navigate the tax code effectively and align their financial decisions with their goals.

The Evolution of Political Systems: A Historical Journey and Transformation

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)

![]()

Campaign Contributions: Direct candidate donations are not tax-deductible

Direct candidate donations, a cornerstone of political campaigns, come with a critical tax implication: they are not tax-deductible. This means that when you contribute to a candidate’s campaign, whether it’s $50 or $2,900 (the federal limit for individual contributions per election cycle as of 2023), you cannot claim this amount as a deduction on your federal income tax return. The IRS categorizes these donations as personal gifts rather than charitable contributions, making them ineligible for tax benefits. This distinction is crucial for donors who may mistakenly assume their political generosity aligns with the tax advantages of charitable giving.

The rationale behind this rule lies in the nature of political campaigns. Unlike donations to 501(c)(3) organizations, which are tax-exempt and serve public welfare, campaign contributions directly support a candidate’s efforts to win office. The IRS views this as participation in the political process rather than a charitable act. For instance, if you donate to a food bank, your contribution alleviates hunger and qualifies for a deduction. But if you donate to a mayoral candidate, your contribution advances their political agenda, which does not qualify. This separation ensures that taxpayers are not indirectly subsidizing political campaigns through deductions.

Practical tip: Always verify the tax status of the organization or candidate before donating. While direct candidate donations are not deductible, contributions to certain political organizations, like 527 groups or political action committees (PACs), may have different tax treatments. However, these are rare exceptions, and most political contributions fall outside the scope of tax deductions. Keep detailed records of your donations, including receipts, to avoid confusion during tax season.

A common misconception is that bundling donations—pooling contributions from multiple individuals—changes their tax status. This is false. Whether you donate $100 directly or contribute to a bundle totaling $1,000, the tax treatment remains the same: non-deductible. Bundlers may gain influence or recognition within a campaign, but they do not gain tax advantages. This underscores the importance of donating with clarity about the financial implications.

In conclusion, understanding the non-deductible nature of direct candidate donations is essential for informed giving. While these contributions are vital to the democratic process, they do not offer tax benefits. Donors should align their financial planning with this reality, ensuring their political participation does not lead to unexpected tax complications. By separating political contributions from charitable donations, individuals can engage in the political process while maintaining fiscal responsibility.

Is Brian Kilmeade Politically Biased? Analyzing His Media Influence

You may want to see also

Explore related products

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UL320_.jpg)

![TurboTax Desktop Business 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71UL+5xLOeL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

Political Action Committees (PACs): PAC donations are generally not tax-deductible

Donations to Political Action Committees (PACs) are a common way for individuals and organizations to support political candidates or causes. However, it’s crucial to understand that these contributions are generally not tax-deductible. Unlike charitable donations to 501(c)(3) organizations, which qualify for deductions, PAC donations fall under a different tax classification. The IRS categorizes PACs as 527 organizations, which are taxed as political entities rather than charities. This distinction means donors cannot claim these contributions as deductions on their federal tax returns, regardless of the amount given.

The rationale behind this rule is rooted in the purpose of PACs. These committees exist to influence elections and political outcomes, not to provide public services or charitable benefits. Allowing tax deductions for such donations could be seen as subsidizing political activity with taxpayer money, a practice the IRS and Congress have chosen to avoid. For example, if you donate $500 to a PAC supporting a congressional candidate, that $500 remains a personal expense and does not reduce your taxable income. This clarity is essential for donors to avoid misunderstandings during tax season.

Despite the lack of tax benefits, PAC donations remain a popular tool for political engagement. Individuals and corporations often contribute to PACs to amplify their voices in the political arena. However, donors should approach these contributions with a clear understanding of the financial implications. To maximize the impact of your political giving, consider aligning your donations with PACs that share your values and priorities. Additionally, keep detailed records of your contributions, as these may be subject to reporting requirements under federal campaign finance laws.

One practical tip for donors is to explore alternative ways to support political causes without relying on tax deductions. For instance, volunteering time, attending fundraising events, or engaging in grassroots advocacy can be equally effective. Another strategy is to diversify your giving by supporting both PACs and tax-deductible charitable organizations, ensuring a balanced approach to civic participation. By understanding the tax rules surrounding PAC donations, you can make informed decisions that align with your financial and political goals.

In conclusion, while PAC donations are a powerful means of political involvement, they do not offer tax advantages. Donors should view these contributions as investments in their preferred candidates or issues rather than financial write-offs. By staying informed and strategic, individuals can navigate the complexities of political giving and contribute meaningfully to the democratic process.

The Art of Polite Thinking: Cultivating Kindness in Every Thought

You may want to see also

Explore related products

![The Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS Penalties](https://m.media-amazon.com/images/I/617DYgupSxL._AC_UL320_.jpg)

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![]()

Charitable Political Groups: Some political-related charities may offer tax deductions

Political contributions and charitable donations often occupy separate spheres in the minds of taxpayers, but there’s a gray area where they intersect: charitable political groups. Unlike direct campaign donations, which are never tax-deductible, certain organizations with political ties can qualify as charities under IRS guidelines. For instance, 501(c)(3) nonprofits focused on voter education, civic engagement, or policy research may accept tax-deductible donations, provided their activities remain nonpartisan and primarily charitable. This distinction hinges on the organization’s mission and operations, not its political proximity. Donors must scrutinize whether the group’s work aligns with IRS criteria for deductibility, as even a hint of lobbying or candidate endorsement can void eligibility.

Consider the League of Women Voters, a classic example of a charitable political group. While it engages in politically charged issues like voting rights, its educational and nonpartisan approach allows donors to claim deductions. Conversely, a 501(c)(4) social welfare organization, which can engage in lobbying and political campaigns, cannot offer tax benefits for contributions. The key lies in the organization’s tax classification and adherence to IRS rules. Donors should verify a group’s 501(c)(3) status using the IRS’s Tax Exempt Organization Search tool before assuming deductibility. Missteps here can lead to disallowed deductions and potential audits.

For those seeking to support political causes while maximizing tax benefits, strategic giving is essential. Start by identifying 501(c)(3) organizations whose missions align with your values but operate within charitable boundaries. For example, donating to a nonpartisan think tank researching climate policy is deductible, whereas funding a political action committee (PAC) is not. Additionally, bundling donations through donor-advised funds can streamline giving while preserving deductibility. However, beware of groups that blur the lines—some organizations may have both 501(c)(3) and 501(c)(4) arms, requiring donors to specify which entity receives their tax-deductible contribution.

A cautionary note: the IRS scrutinizes political-adjacent charities closely. Donors must retain detailed records, including acknowledgment letters from the organization, to substantiate deductions. Contributions exceeding $250 require written confirmation from the charity, detailing the donation amount and any goods or services received in return. Failure to comply can result in denied deductions or penalties. While charitable political groups offer a pathway to align philanthropy with political ideals, due diligence is non-negotiable. By understanding the rules and vetting organizations carefully, donors can support their causes while reaping tax benefits—a win-win for the politically engaged philanthropist.

Hamilton's Legacy: Shaping American Politics and Economic Foundations

You may want to see also

Frequently asked questions

No, donations to political fundraisers, including contributions to candidates, political parties, or PACs (Political Action Committees), are not tax deductible.

No, sponsorships or expenses related to political events or fundraisers are not eligible for tax deductions, as they are considered political contributions.

Only if the donation is solely for the charitable purpose and not earmarked for political activities. The portion of the donation used for political purposes is not tax deductible.