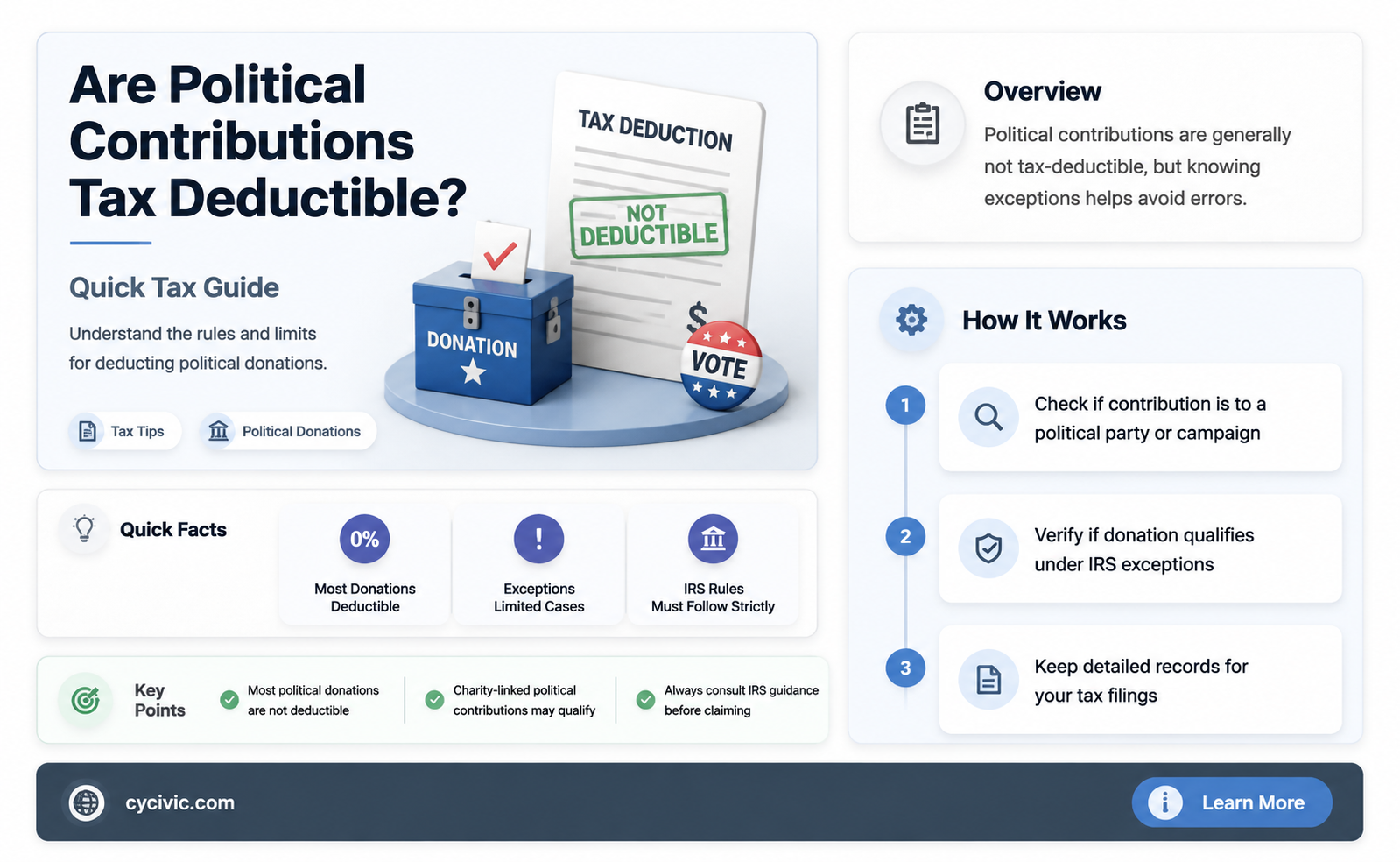

Political contributions often raise questions about their tax implications, particularly whether they can be written off as deductions. In the United States, individual contributions to political campaigns or parties are generally not tax-deductible, as the IRS classifies them as personal expenses rather than charitable donations. However, businesses may deduct certain political contributions made to political action committees (PACs) or other organizations as ordinary and necessary business expenses, though these deductions are subject to strict regulations and limits. Understanding the rules surrounding political contributions and tax write-offs is crucial for both individuals and organizations to ensure compliance with tax laws and avoid potential penalties.

| Characteristics | Values |

|---|---|

| Tax Deductibility (U.S.) | Political contributions to candidates, parties, or PACs are not tax-deductible as charitable donations. |

| Business Contributions | Corporations cannot deduct political contributions as business expenses. |

| Charitable Donations | Donations to 501(c)(3) organizations (e.g., charities) are tax-deductible, but political contributions do not qualify. |

| 527 Organizations | Contributions to 527 organizations (political groups) may be deductible as business expenses in rare cases, but not as charitable donations. |

| State Tax Laws | Some states may allow deductions for political contributions, but this varies by state. |

| IRS Guidelines | The IRS explicitly states that political contributions are not deductible on federal tax returns. |

| Alternative Benefits | While not tax-deductible, political contributions may offer indirect benefits, such as influence or access. |

| Transparency Requirements | Political contributions are subject to disclosure laws, regardless of tax deductibility. |

| Individual vs. Corporate Rules | Both individuals and corporations face the same restrictions on deducting political contributions. |

| Recent Changes (as of 2023) | No recent federal changes have made political contributions tax-deductible. |

Explore related products

What You'll Learn

![]()

Tax Deduction Limits

Political contributions, while a cornerstone of democratic participation, come with specific tax implications that donors must navigate carefully. One critical aspect is understanding the tax deduction limits imposed on these contributions. Unlike charitable donations, which often qualify for deductions up to 60% of adjusted gross income (AGI), political contributions are generally not tax-deductible at the federal level. This distinction is rooted in the Internal Revenue Code, which treats political donations as personal expenses rather than charitable acts. However, some states offer limited deductions or credits for contributions to state or local campaigns, creating a patchwork of rules that donors must research based on their location.

For instance, in California, taxpayers can claim a tax credit for contributions to qualified political campaigns, but the credit is capped at $100 for joint filers and $50 for individual filers. This example highlights how state-level incentives can offset the federal non-deductibility of political contributions, though the benefits are often modest and subject to strict eligibility criteria. Donors should consult state tax guidelines or a tax professional to determine if such opportunities exist in their jurisdiction.

Despite the general rule against federal deductions, there’s a notable exception for unincorporated business contributions. Sole proprietors, partnerships, or LLCs taxed as partnerships may deduct political contributions as a business expense, provided the donation is ordinary and necessary for the business. For example, a small business owner might contribute to a local candidate whose policies directly impact their industry. However, this deduction is limited to $100 per election per candidate or committee, and meticulous record-keeping is essential to substantiate the expense.

A cautionary note: mixing personal and business finances can complicate tax reporting. If a business owner contributes more than the $100 limit, the excess is considered a personal expense and remains non-deductible. Additionally, contributions made through a corporation (C-corp or S-corp) are not deductible under any circumstances, as corporations are prohibited from making direct political donations under federal law.

In conclusion, while political contributions are generally not tax-deductible at the federal level, understanding the nuances of state incentives and business-related exceptions can help donors maximize their financial strategies. Careful planning, adherence to limits, and consultation with tax experts are essential to avoid pitfalls and ensure compliance with complex regulations.

Mastering Political Philosophy: Essential Strategies for Engaging Critical Texts

You may want to see also

Explore related products

![]()

Individual vs. Corporate Rules

In the realm of political contributions, the tax treatment for individuals and corporations diverges significantly, reflecting broader policy goals and economic realities. For individuals, political donations to qualified candidates, parties, or political action committees (PACs) are generally not tax-deductible. This rule, codified in the Internal Revenue Code, ensures that personal political spending does not reduce taxable income, aligning with the principle that civic participation should be voluntary rather than incentivized through tax breaks. For example, if an individual donates $5,000 to a federal candidate, that amount cannot be claimed as a deduction on their federal tax return, meaning their taxable income remains unchanged.

Corporations, however, operate under a different set of rules, though not in the way one might assume. Direct corporate contributions to federal candidates are illegal under the Bipartisan Campaign Reform Act of 2002, often referred to as the McCain-Feingold Act. Instead, corporations can contribute to PACs, which are subject to strict limits and disclosure requirements. Critically, these corporate contributions are not tax-deductible as charitable donations but are treated as ordinary business expenses. This distinction is crucial: while such expenses reduce taxable income, they are not considered charitable write-offs, which are subject to stricter limitations. For instance, a corporation donating $10,000 to a PAC can deduct this amount as a business expense, effectively lowering its taxable income by that sum.

The rationale behind these differing rules lies in the balance between free speech and the prevention of undue influence. Individual contributions are viewed as an expression of personal political agency, while corporate spending is scrutinized to avoid the appearance of buying access or favor. However, this framework has been challenged by Supreme Court decisions like *Citizens United v. FEC* (2010), which allowed corporations and unions to spend unlimited amounts on independent political expenditures, though not direct contributions. These expenditures, often made through super PACs, are not tax-deductible but highlight the evolving landscape of corporate political involvement.

Practical considerations for individuals and corporations further underscore these differences. Individuals must carefully track their contributions to ensure compliance with contribution limits (e.g., $3,300 per candidate per election as of 2023) and avoid any expectation of a tax benefit. Corporations, meanwhile, must navigate complex regulations, including the prohibition on direct contributions and the need to disclose PAC donations. For example, a corporation contributing to a PAC must ensure the funds are not earmarked for a specific candidate, as this could violate federal law.

In conclusion, the tax treatment of political contributions for individuals and corporations is a nuanced reflection of policy priorities and legal constraints. While individuals cannot deduct donations, corporations can treat PAC contributions as business expenses, albeit with strict limitations. Understanding these rules is essential for compliance and underscores the broader debate over the role of money in politics. Whether an individual donor or corporate entity, clarity on these distinctions ensures participation in the political process remains both legal and transparent.

Mastering Polite Company: A Guide to Gracious Social Interactions

You may want to see also

Explore related products

$19.58 $36.99

![]()

Disclosure Requirements

Political contributions, when claimed as deductions, trigger a complex web of disclosure requirements designed to balance transparency with privacy. These mandates vary significantly depending on the jurisdiction, the type of contribution, and the entity making the donation. For instance, in the United States, individuals donating over $200 to a federal candidate or committee must disclose their name, address, occupation, and employer. This information is then made publicly available through the Federal Election Commission (FEC), ensuring voters can track the financial influences behind political campaigns.

For organizations, the stakes are higher. Corporations, unions, and other groups contributing to political action committees (PACs) face stricter scrutiny. They must not only disclose the amount and recipient of their contributions but also detail the source of funds used for such donations. This dual-layer transparency aims to prevent the misuse of pooled resources and maintain accountability. For example, a corporation donating $10,000 to a PAC must file a report with the FEC, specifying whether the funds came from general treasury, a separate segregated fund, or another source.

Nonprofits, particularly those with 501(c)(4) status, operate in a gray area. While they can engage in political activity, their donors often remain anonymous under current IRS regulations. This lack of disclosure has sparked debates about "dark money" in politics, where substantial contributions influence elections without public scrutiny. Critics argue this undermines democratic principles, while proponents defend it as a protection of free speech. The tension highlights the need for clearer, more uniform disclosure rules across all entities.

Internationally, disclosure requirements differ widely. In Canada, for instance, political contributions are not tax-deductible, simplifying the disclosure process. Conversely, countries like Germany require detailed reporting for donations exceeding €10,000, with penalties for non-compliance. These variations underscore the importance of understanding local laws when navigating political contributions. For individuals and organizations alike, staying informed about disclosure thresholds and reporting deadlines is crucial to avoid legal repercussions and maintain public trust.

Practical tips for compliance include maintaining meticulous records of all contributions, regardless of size, and consulting legal experts to interpret complex regulations. Automated tools and software can streamline reporting, reducing the risk of errors. Ultimately, while disclosure requirements may seem burdensome, they serve as a cornerstone of ethical political engagement, ensuring that financial support for candidates and causes is both transparent and accountable.

Intelligence Agencies and Politics: Unraveling the Complex Relationship

You may want to see also

Explore related products

![]()

State vs. Federal Laws

Political contributions often come with the question: can they be written off on taxes? The answer hinges on a critical distinction: state versus federal laws. While federal tax rules explicitly prohibit deductions for political donations, state laws vary widely, creating a patchwork of opportunities and restrictions for contributors.

Consider the federal landscape first. The Internal Revenue Service (IRS) classifies political contributions as neither charitable nor business expenses, making them ineligible for deductions on federal tax returns. This rule applies universally, regardless of the donor’s income, the candidate’s party, or the election’s scale. For instance, a $5,000 donation to a presidential campaign cannot reduce your federal taxable income by that amount. However, federal law does allow deductions for certain related expenses, such as travel costs incurred while volunteering for a campaign, provided they are unreimbursed and properly documented.

In contrast, state tax laws offer a more nuanced picture. Some states, like California and New York, align with federal guidelines, disallowing deductions for political contributions. Others, such as Texas and Florida, permit limited write-offs under specific conditions. For example, in Texas, contributions to state political action committees (PACs) may be deductible up to $100 for individual filers and $200 for joint filers. Meanwhile, in Minnesota, donors can claim a refundable credit for contributions to political parties or candidates, effectively reducing their state tax liability. These variations underscore the importance of consulting state-specific tax codes or a local tax professional before assuming eligibility for deductions.

A comparative analysis reveals strategic implications for donors. In states with favorable write-off policies, contributors can maximize their financial impact by timing donations to align with state tax filing deadlines. For instance, a donor in Minnesota might contribute in December to claim the credit on their upcoming state return. Conversely, in states with no deductions, donors may opt to redirect funds to federally deductible causes, such as 501(c)(3) organizations, to achieve tax benefits. This duality highlights the need for donors to weigh their political and financial goals against the legal frameworks governing their contributions.

Ultimately, navigating the state vs. federal divide requires vigilance and planning. While federal law remains steadfast in its prohibition, state laws offer a spectrum of possibilities that can significantly influence a donor’s strategy. By understanding these distinctions, contributors can make informed decisions that align with both their political aspirations and financial objectives. Always verify current laws, as tax codes evolve, and what holds true today may change tomorrow.

How Book Sales Secretly Fuel Political Campaigns and Influence Elections

You may want to see also

Explore related products

![]()

Non-Profit Contributions Rules

Political contributions and charitable donations often intertwine in public perception, but their tax implications diverge sharply. While political donations to candidates, parties, or PACs are generally not tax-deductible, contributions to qualified non-profits fall under a different set of rules. The IRS classifies eligible non-profits as 501(c)(3) organizations, which include charities, religious groups, and educational institutions. Donations to these entities can be tax-deductible, but only if the donor itemizes deductions and adheres to specific guidelines. This distinction is critical for taxpayers seeking to maximize their financial impact while minimizing liabilities.

To claim a deduction for non-profit contributions, donors must retain proper documentation. For cash donations under $250, a bank record or receipt from the organization suffices. However, contributions exceeding $250 require a written acknowledgment from the non-profit, detailing the donation amount and whether any goods or services were provided in exchange. For instance, if a donor gives $500 to a charity gala and receives a $100 dinner, only $400 is deductible. Failure to secure this acknowledgment can disqualify the deduction, underscoring the importance of meticulous record-keeping.

Non-cash donations, such as clothing, furniture, or vehicles, introduce additional complexities. Items must be in "good used condition or better" to qualify, and deductions are generally limited to the item’s fair market value. For donations valued over $5,000, a qualified appraisal is required, and Form 8283 must be filed with the tax return. For example, donating a car valued at $7,000 necessitates both an appraisal and detailed documentation to substantiate the claim. These rules aim to prevent inflated valuations while encouraging charitable giving.

One often-overlooked aspect is the deduction limit for non-profit contributions. Typically, cash donations are capped at 60% of the donor’s adjusted gross income (AGI), though this was temporarily increased to 100% for tax years 2020 and 2021 due to pandemic-related legislation. Excess contributions can be carried forward for up to five years. For instance, a taxpayer with an AGI of $100,000 who donates $70,000 can deduct $60,000 in the current year and carry forward the remaining $10,000. Understanding these limits ensures donors optimize their tax benefits without triggering penalties.

Finally, it’s crucial to distinguish between non-profit contributions and political donations. While both may align with a donor’s values, only the former offers potential tax advantages. For example, a donation to a political campaign is not deductible, whereas a contribution to a non-profit advocacy group might be. This clarity helps donors make informed decisions, aligning their financial strategies with their philanthropic and political goals. By navigating these rules thoughtfully, individuals can support causes they care about while leveraging available tax benefits.

Mastering Indian Politics: A Comprehensive Guide for Beginners and Enthusiasts

You may want to see also

Frequently asked questions

No, political contributions are not tax deductible. They are considered personal expenses and cannot be claimed as a write-off on your federal tax return.

No, donations to political campaigns, candidates, or political parties are not eligible for tax deductions. They are treated as personal gifts, not charitable contributions.

No, contributions to PACs are not tax deductible. They fall under the same rules as donations to political campaigns and cannot be written off on your taxes.

Donations to 501(c)(4) organizations, which can engage in political activities, are not tax deductible. Only donations to qualified 501(c)(3) charities are eligible for deductions.

No, there is no tax benefit for political contributions. They are strictly personal expenses and do not qualify for deductions or credits on your tax return.