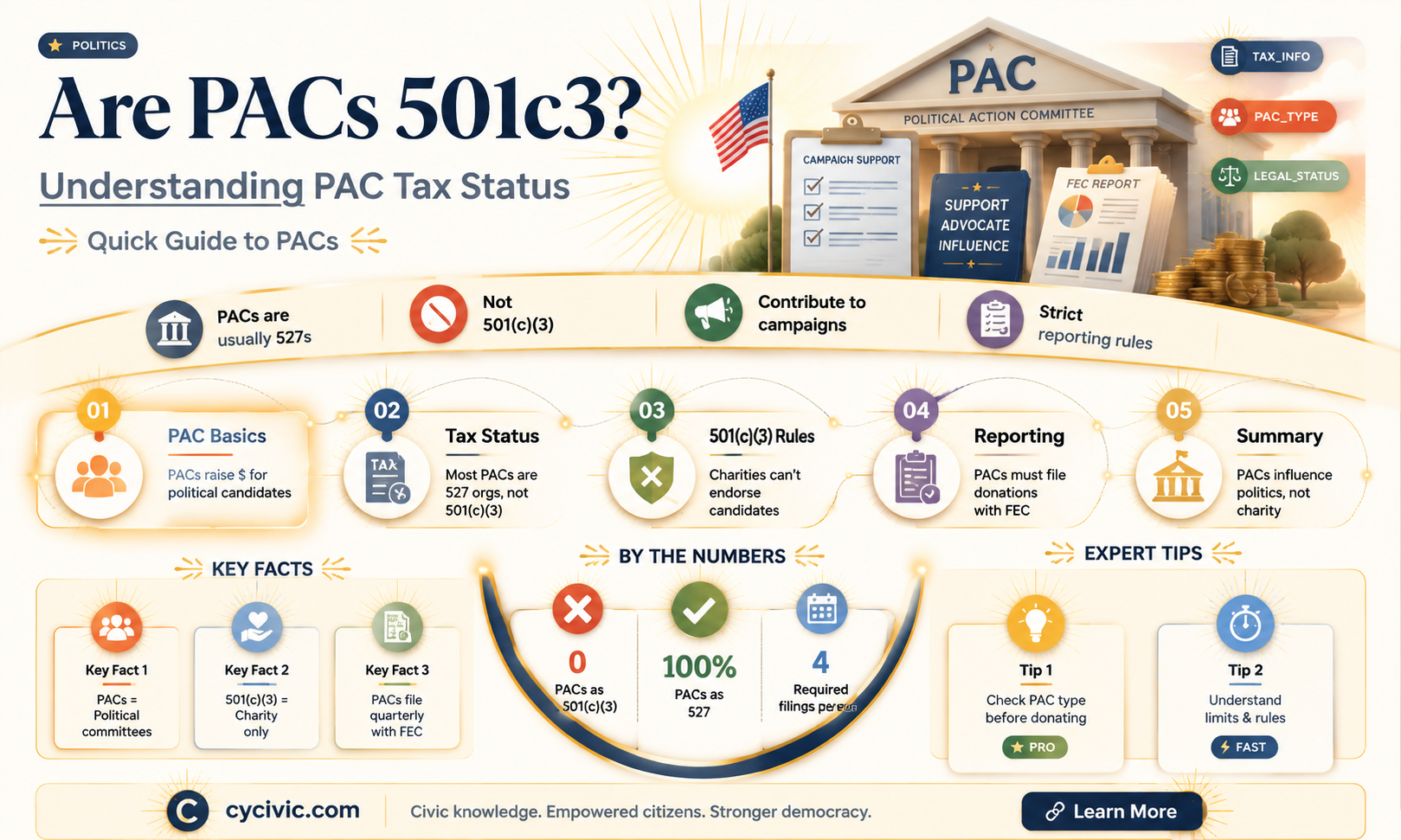

Political Action Committees (PACs) and 501(c)(3) organizations are distinct entities with different purposes and legal frameworks. While PACs are primarily formed to raise and spend money to influence elections and support political candidates, 501(c)(3) organizations are nonprofit entities focused on charitable, educational, religious, or other tax-exempt purposes. A key distinction lies in their tax treatment and political involvement: 501(c)(3) organizations are strictly prohibited from engaging in partisan political activities, such as endorsing candidates or contributing to campaigns, whereas PACs are explicitly designed for political advocacy and fundraising. Understanding these differences is crucial for organizations navigating the legal and ethical boundaries of political participation and nonprofit status.

| Characteristics | Values |

|---|---|

| Tax Status | Political Action Committees (PACs) are not 501(c)(3) organizations. |

| Primary Purpose | PACs are formed to raise and spend money to influence elections. |

| 501(c)(3) Eligibility | 501(c)(3) organizations are charitable, religious, or educational entities prohibited from substantial political activity. |

| Political Activity Allowed | PACs can engage in unlimited political activity, including endorsing candidates and making campaign contributions. |

| Donation Limits | PACs have contribution limits for individuals and organizations. |

| Tax Deductibility of Donations | Donations to PACs are not tax-deductible. |

| Reporting Requirements | PACs must register with the FEC and disclose donors and expenditures. |

| 501(c)(3) Restrictions | 501(c)(3) organizations cannot endorse candidates or engage in partisan political activity. |

| Funding Sources | PACs can accept funds from individuals, corporations, unions, and other organizations. |

| Legal Structure | PACs are typically organized as separate entities from 501(c)(3) organizations. |

| Lobbying Allowed | PACs can lobby for specific legislation or policies. |

| Public Perception | PACs are often associated with political advocacy, while 501(c)(3) organizations are seen as non-partisan and charitable. |

Explore related products

What You'll Learn

![]()

Definition of PACs vs. 501(c)(3)

Political Action Committees (PACs) and 501(c)(3) organizations are distinct entities with fundamentally different purposes, structures, and legal constraints. PACs are formed to raise and spend money to elect or defeat political candidates, making them inherently partisan and focused on influencing elections. In contrast, 501(c)(3) organizations, often nonprofits, are primarily dedicated to charitable, educational, or religious purposes and are strictly prohibited from engaging in partisan political activity. This core distinction shapes their operations, funding sources, and public perception.

Consider the legal framework governing these entities. PACs are regulated by the Federal Election Commission (FEC) and must adhere to strict reporting requirements, including disclosing donors and expenditures. They can accept contributions from individuals, corporations, and unions, though individual donations are capped. Conversely, 501(c)(3) organizations are overseen by the Internal Revenue Service (IRS) and enjoy tax-exempt status, but they cannot endorse candidates or engage in substantial lobbying. Their funding typically comes from grants, donations, and fundraising, with donors receiving tax deductions for their contributions.

A practical example illustrates the difference: A PAC might raise $500,000 to support a candidate’s campaign, openly advocating for their election and running ads to sway voters. A 501(c)(3) organization, however, could raise the same amount to fund a voter education program, provided it remains nonpartisan and does not endorse any candidate. The PAC’s activities are explicitly political, while the 501(c)(3)’s focus is on education, not advocacy.

For those considering forming or supporting such entities, understanding these differences is critical. If your goal is to directly influence elections, a PAC is the appropriate vehicle, but be prepared for transparency and regulatory scrutiny. If your aim is to address broader societal issues without partisan involvement, a 501(c)(3) offers tax benefits and flexibility, but political neutrality is non-negotiable. Missteps in classification or activity can lead to legal penalties, loss of tax-exempt status, or damage to reputation.

In summary, while both PACs and 501(c)(3)s play roles in civic engagement, their definitions and constraints are mutually exclusive. PACs are tools for political advocacy, while 501(c)(3)s are vehicles for charitable or educational work. Choosing between them requires clarity of purpose and a commitment to adhering to their distinct legal boundaries.

Dennis Quaid's Political Views: Uncovering His Stance and Activism

You may want to see also

Explore related products

$24.18 $45

![]()

Legal restrictions on 501(c)(3) political activities

C)(3) organizations, often referred to as charities, face strict legal restrictions on their political activities to maintain their tax-exempt status. The IRS prohibits these entities from engaging in any form of political campaigning, including endorsing or opposing candidates for public office. This restriction is rooted in the Johnson Amendment of 1954, which ensures that charitable donations remain focused on public welfare rather than partisan politics. Violating this rule can result in penalties, fines, or even the loss of tax-exempt status, making compliance critical for these organizations.

While 501(c)(3)s cannot directly support candidates, they are permitted to engage in limited political activities under specific conditions. For instance, they can participate in non-partisan voter education, such as hosting candidate forums or distributing voter guides, as long as these activities do not favor one candidate over another. Additionally, they can advocate for or against legislation, a practice known as lobbying, but only if it constitutes a small portion of their overall activities. The IRS employs a facts-and-circumstances test to determine whether an organization’s lobbying efforts are substantial, with no specific percentage cap but a clear expectation of moderation.

A common misconception is that 501(c)(3)s cannot mention politicians or political issues at all. In reality, they can address public policy matters and even criticize or praise elected officials, as long as these actions are issue-based and not tied to an election campaign. For example, a charity focused on environmental conservation can advocate for stricter pollution laws and commend lawmakers who support such measures, but it cannot call for the election or defeat of those lawmakers. This distinction requires careful navigation to avoid crossing legal boundaries.

Practical tips for 501(c)(3)s include maintaining clear records of all political activities to demonstrate compliance during IRS audits. Organizations should also establish internal policies that define acceptable political engagement and train staff and volunteers accordingly. Consulting legal counsel or tax experts can provide additional safeguards, especially when planning high-profile advocacy campaigns. By adhering to these guidelines, charities can effectively contribute to public discourse without jeopardizing their tax-exempt status.

In contrast to 501(c)(3)s, political action committees (PACs) operate under entirely different rules, as they are 527 organizations designed specifically for political activities. This comparison highlights the unique constraints placed on charities, which must balance their mission-driven work with legal limitations on political involvement. Understanding these restrictions is essential for 501(c)(3) leaders to maximize their impact while staying within the bounds of the law.

Is Greece Politically Stable? Analyzing Current Governance and Future Prospects

You may want to see also

Explore related products

![]()

Consequences of violating 501(c)(3) rules

Political Action Committees (PACs) are fundamentally different from 501(c)(3) organizations. While 501(c)(3)s are tax-exempt nonprofits primarily focused on charitable, educational, or religious purposes, PACs are political entities formed to raise and spend money to influence elections. This distinction is critical because 501(c)(3)s face strict limitations on political activity, and violating these rules can have severe consequences.

One immediate consequence of violating 501(c)(3) rules is the potential loss of tax-exempt status. The IRS scrutinizes organizations to ensure they operate within the boundaries of their tax classification. If a 501(c)(3) engages in substantial lobbying or endorses political candidates, it risks revocation of its tax exemption. This means the organization would owe taxes on its income, face penalties, and lose its ability to accept tax-deductible donations, effectively crippling its financial stability.

Beyond financial penalties, violating 501(c)(3) rules can damage an organization’s reputation. Donors, supporters, and the public generally expect nonprofits to remain nonpartisan and focus on their mission. If an organization is perceived as politically biased, it may alienate its donor base and lose public trust. For example, a charity that publicly endorses a candidate might see a significant drop in donations from individuals who support the opposing party.

Legal repercussions are another serious concern. The IRS can impose excise taxes on the organization and its managers for excessive political intervention. Additionally, if the violation involves illegal campaign contributions or coordination with candidates, the organization and its leaders could face civil or criminal charges under campaign finance laws. These legal battles are costly and time-consuming, diverting resources away from the organization’s core mission.

To avoid these consequences, 501(c)(3) organizations must adhere to strict guidelines. They can engage in limited lobbying if it aligns with their mission and does not constitute a substantial part of their activities. However, they must never endorse or oppose candidates. Establishing clear policies, providing staff training, and seeking legal counsel when in doubt are practical steps to ensure compliance. By staying within the bounds of the law, nonprofits can protect their status, reputation, and ability to serve their communities effectively.

Is ASEAN a Political Union? Exploring Its Structure and Limitations

You may want to see also

Explore related products

$26.6 $28

$26.36 $28

$14.5 $28

![]()

Differences between 501(c)(3) and 501(c)(4)

Political Action Committees (PACs) are often associated with 501(c)(4) organizations, not 501(c)(3)s. This distinction is critical because it determines how an organization can engage in political activities, fundraising, and advocacy. While both are tax-exempt under the Internal Revenue Code, their purposes, limitations, and reporting requirements differ significantly. Understanding these differences is essential for anyone involved in nonprofit or political work.

Purpose and Activities: A 501(c)(3) organization is primarily charitable, religious, educational, or scientific in nature. Its activities must further a public benefit, and it is strictly prohibited from engaging in partisan political campaigning. For example, a 501(c)(3) can educate voters on issues but cannot endorse or oppose candidates. In contrast, a 501(c)(4) is a social welfare organization, allowed to promote the common good and social welfare through advocacy, lobbying, and even direct political campaigning. However, political activities cannot be its *primary* purpose—a vague line that often requires careful legal navigation.

Donor Disclosure and Fundraising: One of the most significant differences lies in donor disclosure. 501(c)(3)s must disclose substantial donors to the IRS but keep this information private from the public. Conversely, 501(c)(4)s are not required to disclose donor identities to the IRS or the public, making them attractive for anonymous political spending. Fundraising for a 501(c)(3) often involves grants, individual donations, and foundation support, while 501(c)(4)s can accept unlimited contributions from individuals, corporations, and unions, often used for political ads or lobbying efforts.

Lobbying and Political Expenditures: 501(c)(3)s face strict limits on lobbying, with the "substantial part test" prohibiting excessive legislative advocacy. While the IRS doesn’t define "substantial," organizations typically limit lobbying to 20% of their activities to stay safe. Political expenditures are entirely off-limits. In contrast, 501(c)(4)s can spend a substantial portion of their resources on lobbying and political campaigns, though they must report these activities to the IRS. For instance, a 501(c)(4) can run ads supporting a candidate, while a 501(c)(3) cannot.

Practical Takeaway: If your goal is to engage in direct political action, such as endorsing candidates or running issue ads, a 501(c)(4) is the appropriate vehicle. However, if your focus is on nonpartisan charitable work, education, or research, a 501(c)(3) provides tax benefits and donor incentives but restricts political involvement. Organizations often create both entities to separate charitable and political activities, ensuring compliance while maximizing impact. Always consult legal counsel to navigate these complex rules effectively.

Unsubscribe Kindle Politico: Quick Steps to Cancel Your Subscription

You may want to see also

Explore related products

![]()

Examples of permissible 501(c)(3) advocacy

C)(3) organizations, often nonprofits, are prohibited from engaging in partisan political activities, but they can still advocate for issues and policies that align with their mission. This advocacy must be nonpartisan, meaning it cannot support or oppose specific candidates or political parties. Instead, it focuses on educating the public, influencing legislation, and promoting systemic change. For example, a 501(c)(3) dedicated to environmental conservation can lobby for stricter emissions regulations without endorsing a candidate who supports those policies. The key is to frame advocacy around issues, not individuals or parties.

One permissible form of advocacy is public education campaigns. A 501(c)(3) can create and distribute materials that raise awareness about a specific issue, such as climate change or healthcare access. For instance, a nonprofit focused on education reform might publish reports, host webinars, or launch social media campaigns highlighting the need for equitable school funding. These efforts must be factual and unbiased, avoiding any language that could be construed as political campaigning. The goal is to inform the public and policymakers, not to sway votes in favor of a particular candidate.

Lobbying is another allowable activity, but with strict limits. The IRS allows 501(c)(3)s to engage in lobbying as long as it is not a substantial part of their overall activities. This is often referred to as the "no substantial part" test. For example, a nonprofit advocating for affordable housing can meet with legislators to discuss policy changes, draft model legislation, or testify at hearings. However, they must track their lobbying expenses and ensure they do not exceed the IRS-defined thresholds, which are based on the organization’s total expenditures. Exceeding these limits could jeopardize their tax-exempt status.

Nonpartisan voter engagement is also a permissible advocacy activity. A 501(c)(3) can encourage people to register to vote, provide voter education materials, and host candidate forums, as long as these efforts are unbiased. For instance, a nonprofit focused on civic engagement might organize voter registration drives or distribute guides comparing candidates’ positions on key issues without endorsing any one candidate. The emphasis must be on participation, not persuasion. This type of advocacy strengthens democracy while adhering to IRS guidelines.

Finally, coalition building and collaboration can amplify a 501(c)(3)’s advocacy efforts. By partnering with other nonprofits, community groups, or businesses, organizations can pool resources and expertise to advocate for systemic change. For example, a nonprofit working on criminal justice reform might join forces with legal aid organizations, faith-based groups, and formerly incarcerated individuals to push for sentencing reform. These partnerships must remain nonpartisan, focusing on shared policy goals rather than political affiliations. This collaborative approach not only increases impact but also demonstrates the collective power of issue-based advocacy.

Masculinity in Power: Deconstructing the Gendered Landscape of Formal Politics

You may want to see also

Frequently asked questions

No, a 501(c)(3) organization cannot form or operate a PAC. Engaging in political campaign activities, including forming a PAC, can jeopardize its tax-exempt status.

No, PACs are not 501(c)(3) organizations. PACs are typically registered under Section 527 of the Internal Revenue Code and are primarily focused on political activities, while 501(c)(3) organizations are charitable and prohibited from substantial political campaigning.

No, 501(c)(3) organizations are strictly prohibited from endorsing political candidates or contributing to PACs. Such actions violate IRS rules and can result in loss of tax-exempt status.