In New Zealand, the question of whether donations to political parties are tax-deductible is a topic of interest for both individuals and organizations looking to support political causes. Unlike some countries where such donations may qualify for tax deductions, New Zealand’s tax laws do not allow individuals or businesses to claim tax deductions for contributions made to political parties. This is because political donations are considered private gifts rather than charitable contributions, which are the primary type of donations eligible for tax relief. As a result, donors should be aware that their financial support to political parties will not reduce their taxable income, and they must comply with the strict regulations governing political donations, including disclosure requirements for amounts over certain thresholds.

| Characteristics | Values |

|---|---|

| Tax Deductibility | Donations to political parties in New Zealand are not tax-deductible. |

| Relevant Legislation | Inland Revenue Department (IRD) guidelines and the Income Tax Act 2007. |

| Purpose of Donations | Political donations are considered personal contributions, not charitable. |

| Charitable Status | Political parties do not qualify as charitable organizations under NZ law. |

| Alternative Benefits | Donors may receive acknowledgments or party-specific perks, but no tax benefits. |

| Transparency Requirements | Donations over NZD 15,000 must be disclosed to the Electoral Commission. |

| Recent Updates (as of 2023) | No changes to tax deductibility status for political donations. |

| Comparison to Charities | Donations to registered charities in NZ are tax-deductible. |

Explore related products

$13.9 $25

What You'll Learn

- Eligibility Criteria: Conditions for donations to qualify as tax-deductible in New Zealand

- Political Party Requirements: Which parties are eligible to receive tax-deductible donations

- Donation Limits: Maximum amounts individuals or entities can donate with tax benefits

- Claiming Process: Steps to claim tax deductions for political party donations

- Legal Restrictions: Rules and prohibitions on tax-deductible political donations in NZ

![]()

Eligibility Criteria: Conditions for donations to qualify as tax-deductible in New Zealand

In New Zealand, donations to political parties are generally not tax-deductible. The Inland Revenue Department (IRD) clearly states that contributions to political parties or candidates do not qualify for tax deductions. This is because political donations are considered a personal choice rather than a charitable contribution. The tax system in New Zealand is designed to provide deductions for donations made to approved donee organizations, which typically include charities, educational institutions, and certain cultural or religious bodies. Political parties do not fall under this category, as their primary purpose is not charitable or public benefit in the eyes of the tax law.

To qualify for a tax deduction in New Zealand, donations must meet specific eligibility criteria. First, the recipient organization must be an approved donee organization as listed by the IRD. These organizations are typically registered charities, public art galleries, museums, or other entities that serve a public good. Second, the donation must be made voluntarily and without any expectation of material benefit in return. For example, if a donor receives goods, services, or other advantages in exchange for their donation, it may not qualify for a tax deduction. This principle ensures that only genuine charitable contributions are eligible for tax relief.

Another critical condition is that the donation must be in the form of money or property. Cash donations are the most straightforward, but donations of assets like shares, land, or artwork may also qualify, provided they are valued appropriately. The donor must retain proper documentation, such as receipts or acknowledgment letters from the recipient organization, to claim the deduction. Additionally, the donation must be made during the tax year for which the deduction is being claimed, and the donor must declare it accurately in their tax return.

It is important to note that there are limits to how much can be claimed as a tax deduction for donations. As of the latest guidelines, individuals can claim up to the lesser of 33.33% of their taxable income or the total amount donated. For example, if an individual donates $1,000 and their taxable income is $30,000, they can claim a maximum deduction of $1,000. However, if they donate $2,000, the maximum deduction remains capped at 33.33% of their taxable income, which would be $10,000 in this case. This ensures that tax deductions for donations do not disproportionately reduce an individual's tax liability.

Lastly, donors should be aware that the rules around tax-deductible donations can change, and it is essential to consult the latest IRD guidelines or seek professional advice. While political party donations do not qualify, understanding the eligibility criteria for tax-deductible donations can help individuals and businesses maximize their contributions to approved organizations while benefiting from tax relief. Always ensure that the recipient organization is eligible and that all documentation is in order to avoid complications during the tax filing process.

Explore related products

![]()

Political Party Requirements: Which parties are eligible to receive tax-deductible donations

In New Zealand, not all political parties are eligible to receive tax-deductible donations. The eligibility criteria are strictly defined by the Electoral Act 1993 and the Income Tax Act 2007. To qualify, a political party must be registered with the Electoral Commission, which is the independent body responsible for overseeing New Zealand’s electoral system. Registration requires the party to meet specific conditions, such as having a minimum of 500 financial members, adhering to democratic principles, and complying with financial reporting obligations. These requirements ensure that only parties with a genuine and substantial presence in the political landscape can receive tax-deductible donations.

Registered political parties must also maintain transparency in their financial dealings. This includes submitting annual returns to the Electoral Commission, detailing income, expenses, and donations. Parties that fail to meet these reporting requirements risk losing their registered status, thereby disqualifying them from receiving tax-deductible donations. Additionally, parties must not engage in activities that contravene electoral laws, such as accepting anonymous donations above the legal threshold or failing to disclose donor information. Compliance with these rules is essential for maintaining eligibility.

Another critical factor is the party’s representation in Parliament. While registration is the primary requirement, parties with parliamentary representation often have a higher public profile and are more likely to attract donations. However, parliamentary presence alone does not automatically qualify a party for tax-deductible donations; registration remains the key criterion. This ensures that even smaller parties, provided they meet the registration requirements, can compete for donor support on a more level playing field.

Donors must also be aware of the limits on tax-deductible contributions. As of the latest regulations, individuals and organizations can claim tax deductions for donations up to a certain capped amount per year. Donations exceeding this cap are not eligible for tax relief. This rule applies uniformly to all registered parties, regardless of their size or influence, ensuring fairness in the political donation system.

In summary, eligibility for tax-deductible donations in New Zealand hinges on a political party’s registered status with the Electoral Commission. Parties must meet membership, transparency, and compliance requirements to qualify. Donors should verify a party’s registration before making contributions to ensure their donations are tax-deductible. This system aims to balance financial support for political participation with accountability and fairness in the democratic process.

Explore related products

![]()

Donation Limits: Maximum amounts individuals or entities can donate with tax benefits

In New Zealand, donations to political parties are not tax-deductible for individuals or entities. This means that regardless of the amount donated, contributors cannot claim a tax deduction on their income tax returns. The Inland Revenue Department (IRD) clearly states that donations to political parties do not qualify for tax relief, unlike charitable donations, which may be eligible under specific conditions. This distinction is crucial for donors to understand, as it directly impacts their financial planning and tax obligations.

Despite the lack of tax deductibility, there are still limits on how much individuals or entities can donate to political parties in New Zealand. Under the Electoral Act 1993, individuals are permitted to donate up to NZ$1,500 per year to a single political party without disclosing their identity. However, any donation exceeding this amount must be reported to the Electoral Commission, and the donor’s details will be made public. This transparency measure aims to prevent undue influence and ensure accountability in political funding.

For entities, such as companies or organizations, the donation limit is significantly higher. Entities can donate up to NZ$30,000 per year to a single political party. Similar to individual donations, any amount above this threshold must be disclosed to the Electoral Commission. These limits apply to both monetary donations and the value of non-monetary contributions, such as goods or services provided to a political party. It is essential for entities to carefully track their donations to remain compliant with legal requirements.

While these donation limits exist, it is important to reiterate that none of these contributions offer tax benefits. Donors should not confuse the legal donation caps with tax-deductible opportunities, as the two are entirely separate. The primary purpose of these limits is to regulate political funding and maintain fairness in the electoral process, rather than to provide financial incentives for donors.

In summary, individuals and entities in New Zealand face specific limits on how much they can donate to political parties, but these donations do not come with tax benefits. Individuals can donate up to NZ$1,500 anonymously, while entities can contribute up to NZ$30,000 annually. All donations above these thresholds must be disclosed to the Electoral Commission. Donors should be aware of these regulations to ensure compliance and avoid misconceptions about tax deductibility.

Explore related products

![]()

Claiming Process: Steps to claim tax deductions for political party donations

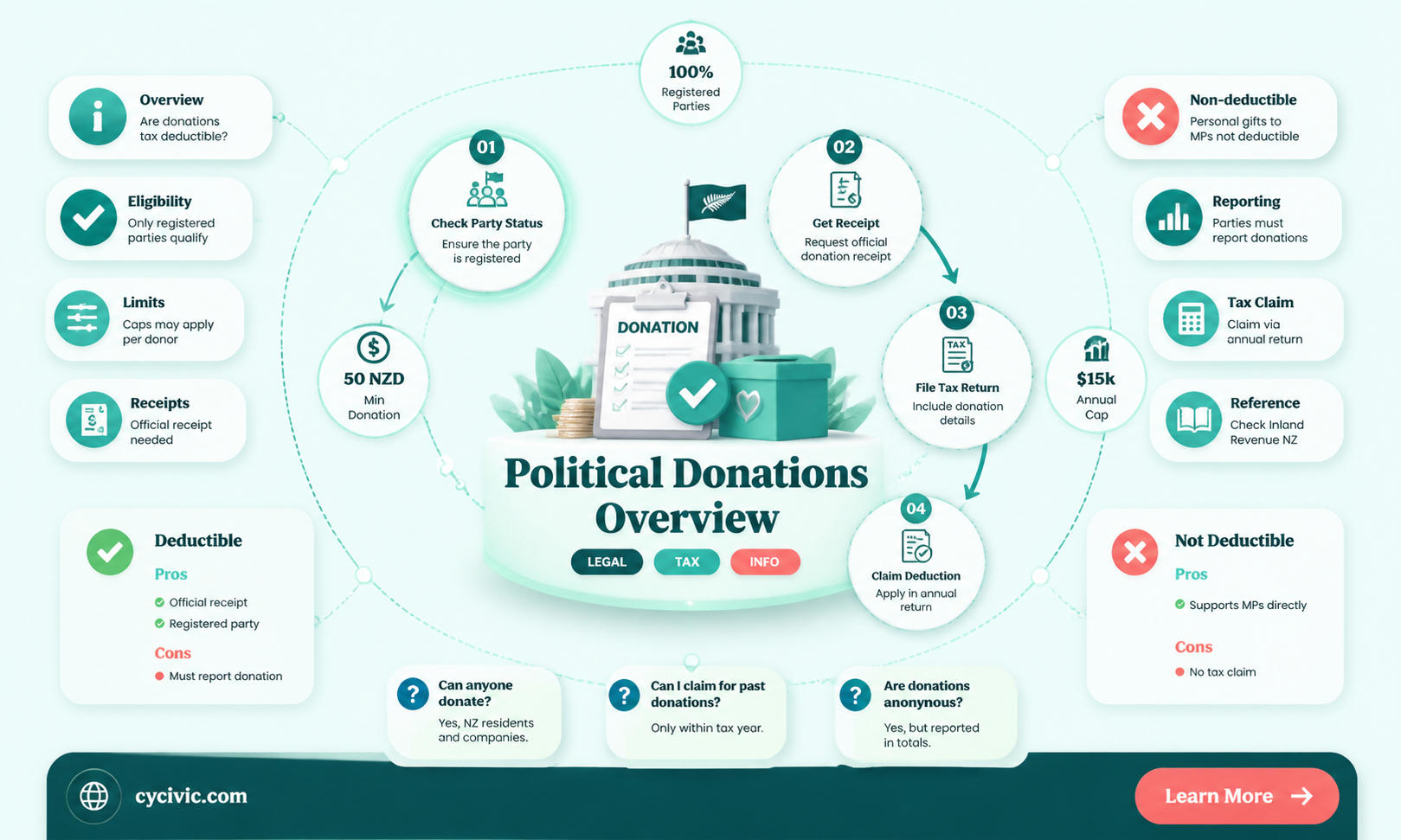

In New Zealand, donations to registered political parties can be eligible for a tax credit, which is effectively a tax deduction. To claim this tax credit, donors must follow a specific process outlined by the Inland Revenue Department (IRD). The first step is to ensure that the donation is made to a registered political party, as only these parties qualify for the tax credit scheme. Donors should verify the party’s registration status on the Electoral Commission’s website or directly with the party itself. Once confirmed, the donor can proceed with the donation, ensuring they receive a receipt from the political party. This receipt is a crucial document, as it serves as proof of the donation and is required for the tax credit claim.

After making the donation and obtaining the receipt, the next step is to complete the necessary tax credit claim form. This form, known as the "Political Donation Tax Credit Claim Form," is available on the IRD website. Donors must fill out the form accurately, providing details such as their name, IRD number, the amount donated, and the date of the donation. The receipt from the political party should be attached to the form as supporting evidence. It is important to ensure all information is correct, as errors may delay the processing of the claim. Once the form is completed, it should be submitted to the IRD either online or by mail, depending on the donor’s preference and the IRD’s current submission guidelines.

The timing of the claim is also a critical aspect of the process. Donors can claim the tax credit in the same tax year the donation was made or in the following tax year. For example, if a donation is made in March 2023, the donor can claim the tax credit in their 2023 tax return or wait until their 2024 tax return. However, it is advisable to claim the tax credit as soon as possible to benefit from the reduction in tax liability earlier. Donors should also be aware of the annual limit for tax credits on political donations, which is currently set at NZ$1,500 per tax year. Any amount exceeding this limit is not eligible for the tax credit.

Once the claim is submitted, the IRD will process it and apply the tax credit to the donor’s tax account. This typically results in a reduction of the donor’s tax liability or, in some cases, a refund if the donor has overpaid their taxes. Donors should monitor their tax account through the IRD’s online services or by contacting the IRD directly to confirm that the tax credit has been applied correctly. If there are any issues or discrepancies, donors should promptly communicate with the IRD to resolve them.

Finally, it is essential for donors to keep records of all donations and related correspondence for at least seven years. This includes receipts from the political party, copies of the tax credit claim form, and any communication with the IRD regarding the claim. Maintaining thorough records ensures compliance with IRD requirements and provides a reference in case of any future inquiries or audits. By following these steps, donors can successfully claim tax credits for their political party donations in New Zealand, supporting their chosen party while benefiting from a reduction in their tax liability.

Explore related products

![]()

Legal Restrictions: Rules and prohibitions on tax-deductible political donations in NZ

In New Zealand, the rules surrounding tax-deductible political donations are stringent and clearly defined to maintain transparency and fairness in the political process. Unlike some countries where donations to political parties or candidates may qualify for tax deductions, New Zealand’s tax laws explicitly prohibit such deductions. The Inland Revenue Department (IRD) states that donations to political parties, candidates, or related entities are not eligible for tax deductions under the Income Tax Act 2007. This prohibition ensures that political contributions are made voluntarily without the incentive of reducing taxable income, thereby preventing potential misuse of the tax system for political gain.

One of the key legal restrictions is the prohibition on claiming tax deductions for donations made to political parties, parliamentary candidates, or entities closely associated with them. This includes donations in cash, goods, or services. The rationale behind this rule is to maintain the integrity of the electoral system and prevent wealthy individuals or corporations from disproportionately influencing political outcomes through tax-advantaged donations. Additionally, this restriction aligns with New Zealand’s broader commitment to transparency in political funding, as outlined in the Electoral Act 1993, which requires detailed disclosure of donations above a certain threshold.

Another important restriction is the ban on indirect tax benefits for political donations. For instance, businesses or individuals cannot structure transactions in a way that allows them to claim tax deductions for expenses that effectively fund political activities. This includes scenarios where donations are disguised as payments for services or goods that are not provided at fair market value. The IRD closely monitors such arrangements to ensure compliance with tax laws and to prevent the circumvention of the prohibition on tax-deductible political donations.

Furthermore, New Zealand’s legal framework imposes strict limits on the size and source of political donations. While these limits are not directly related to tax deductibility, they work in tandem with the prohibition on tax deductions to regulate political funding. For example, anonymous donations above a certain threshold are prohibited, and all donations above NZ$1,500 (as of recent regulations) must be disclosed to the Electoral Commission. These measures, combined with the tax restrictions, create a robust system to prevent undue influence and ensure accountability in political financing.

Lastly, it is important for donors to be aware of the consequences of attempting to claim tax deductions for political donations. Such actions can result in penalties, including fines and potential legal action by the IRD. Donors are advised to consult with tax professionals or refer to official IRD guidelines to ensure compliance with the law. In summary, New Zealand’s legal restrictions on tax-deductible political donations are designed to uphold the principles of fairness, transparency, and accountability in the political process, leaving no room for tax incentives in this critical area of civic engagement.

Frequently asked questions

No, donations to political parties are not tax deductible in New Zealand. The Inland Revenue Department (IRD) does not allow tax deductions for political donations.

No, there are no tax credits available for donations to political parties in New Zealand. Such donations are considered private contributions and do not qualify for tax benefits.

No, there are no exceptions. Donations to political parties, candidates, or related organizations are not eligible for tax deductions or credits under New Zealand tax laws.