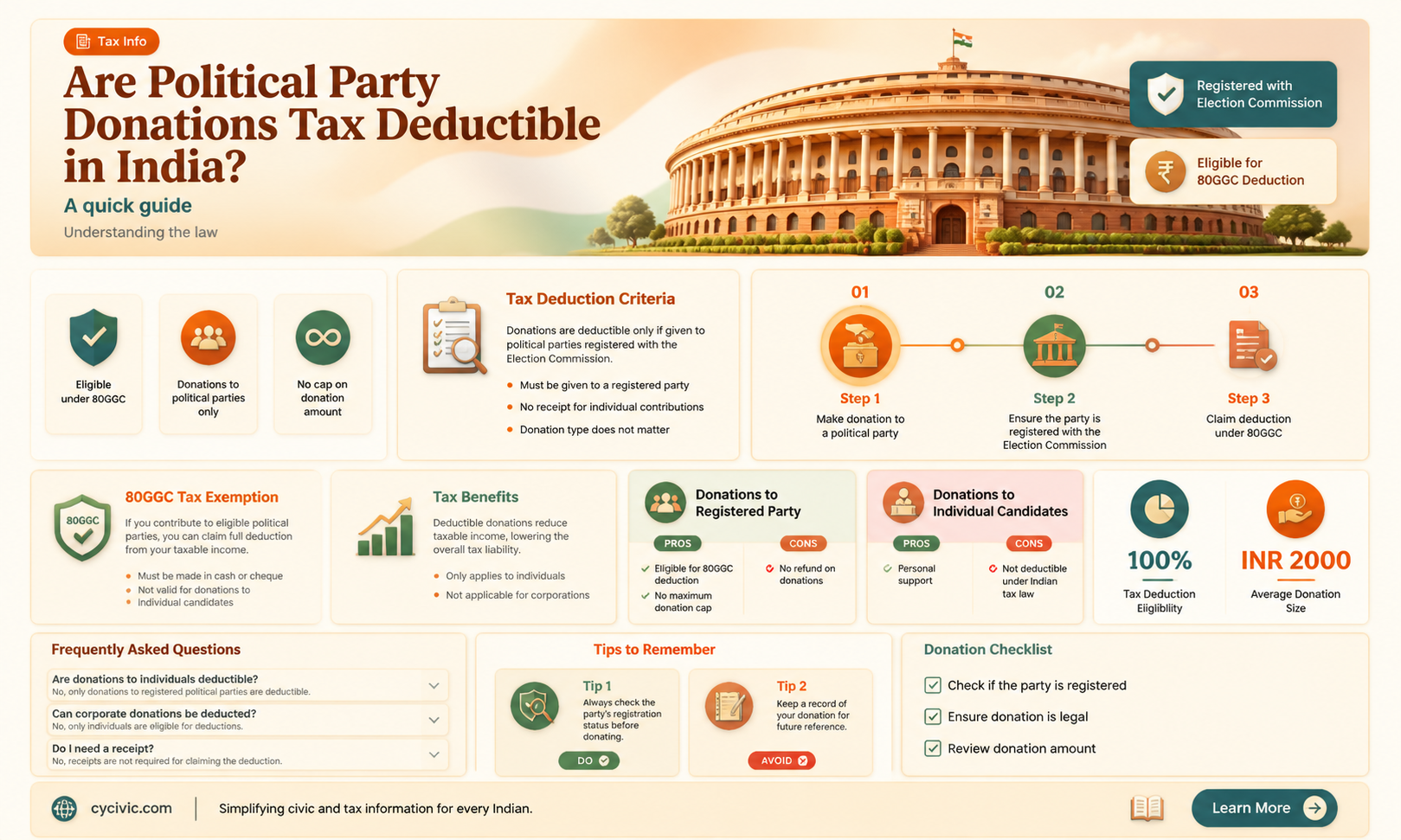

In India, donations to political parties are a subject of significant interest, particularly regarding their tax implications. Many individuals and organizations contribute financially to political parties to support their ideologies and agendas, but the question often arises whether these donations qualify for tax deductions. Under the current Indian tax laws, donations made to political parties are eligible for tax benefits under Section 80GGB (for corporates) and Section 80GGC (for individuals) of the Income Tax Act, 1961. These provisions allow donors to claim deductions from their taxable income, thereby reducing their overall tax liability. However, it is crucial to ensure that the political party receiving the donation is registered and recognized by the Election Commission of India, as only contributions to such parties are eligible for these tax benefits. This framework aims to encourage transparency and accountability in political funding while providing donors with financial incentives to support democratic processes.

| Characteristics | Values |

|---|---|

| Tax Deductibility | No, donations to political parties are not tax deductible in India. |

| Relevant Law | Income Tax Act, 1961 (Section 80G specifically excludes political parties from eligible donee institutions) |

| Reason for Exclusion | To prevent potential misuse of tax benefits for political funding and maintain transparency in political donations. |

| Alternative Tax Benefits | None specifically for political donations. |

| Reporting Requirements | Political parties must report donations above a certain threshold to the Election Commission of India. |

| Donation Limits | No specific limits on individual donations, but cash donations above ₹2,000 are prohibited. |

| Electoral Bonds | Previously allowed anonymous donations through electoral bonds, but the scheme was struck down by the Supreme Court in 2024. |

| Current Status (as of 2023) | Donations remain non-tax deductible, with increased scrutiny on funding sources. |

Explore related products

What You'll Learn

- Legal Framework: Understanding the Income Tax Act and its provisions on political donations

- Eligibility Criteria: Which political parties qualify for tax-deductible donations in India

- Donation Limits: Maximum amounts eligible for tax deductions under Section 80GGB/80GGC

- Documentation Required: Proof and receipts needed to claim tax benefits for political donations

- Corporate vs. Individual: Differences in tax deductions for corporate and individual donors

![]()

Legal Framework: Understanding the Income Tax Act and its provisions on political donations

In India, the legal framework governing the tax treatment of donations to political parties is primarily outlined in the Income Tax Act, 1961. Section 80GGB and Section 80GGC of the Act specifically address the deductibility of such donations. These provisions are designed to encourage transparency and accountability in political funding while offering tax benefits to donors. Under Section 80GGB, companies are allowed to claim a deduction for contributions made to registered political parties. This deduction is available from the taxable income of the company, thereby reducing its tax liability. However, it is important to note that donations made in cash exceeding ₹2,000 are not eligible for this deduction, emphasizing the need for transparent and traceable transactions.

For individuals and Hindu Undivided Families (HUFs), Section 80GGC provides a similar deduction for donations to political parties. Like companies, individuals and HUFs can claim a deduction from their taxable income for contributions made to registered political parties. The same restriction on cash donations applies here as well—donations exceeding ₹2,000 in cash are not eligible for the deduction. This provision ensures that individual donors also contribute to political funding in a manner that is accountable and traceable. It is crucial for donors to obtain a receipt from the political party as proof of donation, which must be submitted while filing income tax returns to claim the deduction.

The Income Tax Act also mandates that political parties maintain proper records of donations received. This includes details such as the name and address of the donor, the amount donated, and the mode of payment. Political parties are required to report these details to the Election Commission of India and the Income Tax Department, ensuring compliance with legal requirements. This transparency is essential to prevent misuse of funds and to maintain the integrity of the political funding process. Donors must ensure that the political party to which they are contributing is registered under Section 29A of the Representation of the People Act, 1951, as deductions are only available for donations to such parties.

Another critical aspect of the legal framework is the prohibition of anonymous donations above ₹20,000. Political parties are not allowed to accept contributions exceeding this amount without recording the donor’s details. This rule, combined with the tax deduction provisions, aims to curb the flow of unaccounted money into politics. While the tax deductions under Section 80GGB and 80GGC provide an incentive for legitimate donations, they also serve as a tool for monitoring and regulating political funding. It is important for donors to be aware of these rules to ensure compliance and to maximize the benefits of their contributions.

In summary, the Income Tax Act, 1961, through Sections 80GGB and 80GGC, provides a clear legal framework for the tax treatment of donations to political parties in India. These provisions allow companies, individuals, and HUFs to claim deductions for their contributions, subject to certain conditions such as the mode of payment and the registration status of the political party. The Act also imposes stringent reporting requirements on political parties to ensure transparency and accountability. By understanding these provisions, donors can make informed decisions while contributing to political parties, ensuring both compliance with the law and the optimization of tax benefits.

Joseph McCarthy's Political Party: Uncovering His Affiliation and Legacy

You may want to see also

Explore related products

$13.9 $25

![]()

Eligibility Criteria: Which political parties qualify for tax-deductible donations in India

In India, not all political parties qualify for tax-deductible donations under the Income Tax Act, 1961. The eligibility criteria are stringent and designed to ensure that only recognized and established political entities benefit from this provision. According to Section 80GGB and 80GGC of the Income Tax Act, donations made to recognized political parties are eligible for tax deductions. The recognition of a political party is determined by the Election Commission of India (ECI) under the provisions of the Representation of the People Act, 1951. This means that only those parties registered with the ECI and meeting its criteria for recognition can receive tax-deductible donations.

The ECI grants recognition to political parties at two levels: national and state. A party is recognized as a national party if it meets specific criteria, such as securing at least 6% of the valid votes polled in any four or more states in the last Lok Sabha or State Legislative Assembly elections and has at least four members in the Lok Sabha. Similarly, a party is recognized as a state party if it fulfills conditions like securing 6% of the valid votes polled in the last State Legislative Assembly election and has at least two members in the State Assembly. Only donations to parties with such recognition qualify for tax deductions.

It is important to note that donations to unregistered or unrecognized political parties do not qualify for tax deductions. Donors must ensure that the party they are contributing to is officially recognized by the ECI. The list of recognized political parties is periodically updated by the ECI and can be verified on its official website or through the Income Tax Department’s portal. This verification step is crucial to ensure compliance with tax laws and to avail of the deduction benefits.

Additionally, the mode of donation plays a role in eligibility for tax deductions. Donations made in cash exceeding ₹2,000 are not eligible for deductions under Section 80GGB and 80GGC. Donors must contribute through traceable methods such as cheques, demand drafts, or electronic transfers to qualify for the tax benefit. This requirement is intended to promote transparency and accountability in political funding.

Lastly, the eligibility criteria also extend to the type of donor. Under Section 80GGB, companies (other than those having a turnover exceeding ₹100 crore) can claim deductions for donations to recognized political parties. Under Section 80GGC, individuals and Hindu Undivided Families (HUFs) can avail of this benefit. It is essential for donors to fall within these categories to claim the tax deduction, further narrowing the scope of eligibility for this provision.

Does Target Donate to Political Parties? Uncovering Corporate Contributions

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-One]: Start & Grow Your Business While Saving on Taxes – Insider Strategies, Bookkeeping Hacks & Smart Accounting Tips](https://m.media-amazon.com/images/I/61QksxYPu+L._AC_UL320_.jpg)

![]()

Donation Limits: Maximum amounts eligible for tax deductions under Section 80GGB/80GGC

In India, donations to political parties can indeed be tax deductible, but the rules and limits are specific and governed by the Income Tax Act, 1961. The relevant sections for tax deductions on political donations are Section 80GGB and Section 80GGC. These sections allow certain taxpayers to claim deductions for contributions made to registered political parties, but the eligibility and limits vary depending on the type of taxpayer. Understanding these limits is crucial for individuals and companies looking to optimize their tax liabilities while supporting political causes.

Section 80GGB applies to companies, including Indian companies and foreign companies with a presence in India. Under this section, any contribution made by a company to a registered political party is eligible for a tax deduction. The key point here is that there is no upper limit on the amount that can be claimed as a deduction. This means companies can donate any amount to political parties and claim the entire sum as a deduction from their taxable income. However, the donation must be made via a traceable method such as a cheque, bank draft, or electronic transfer; cash donations are not eligible for this deduction.

Section 80GGC, on the other hand, is applicable to individuals and Hindu Undivided Families (HUFs). Unlike Section 80GGB, this section imposes a cap on the deduction amount. The deduction is limited to the amount donated, but it cannot exceed the taxable income of the individual or HUF. For example, if an individual donates ₹1 lakh to a political party but their taxable income is only ₹80,000, the maximum deduction they can claim is ₹80,000. Similar to Section 80GGB, donations under Section 80GGC must also be made through traceable modes, and cash donations are not allowed.

It is important to note that both sections require the political party to be registered under Section 29A of the Representation of the People Act, 1951. Donations to unregistered parties or independent candidates do not qualify for these deductions. Additionally, the taxpayer must obtain a receipt from the political party as proof of donation, which must be submitted when filing income tax returns. These receipts should include details such as the name and address of the party, the amount donated, and the mode of payment.

While these sections provide tax benefits for political donations, taxpayers should exercise caution and ensure compliance with all legal requirements. Misreporting or claiming deductions for ineligible donations can lead to penalties and legal consequences. By adhering to the guidelines under Section 80GGB and Section 80GGC, both companies and individuals can contribute to political parties while enjoying tax benefits within the prescribed limits.

How to Legally Verify Someone's Political Party Affiliation

You may want to see also

Explore related products

![]()

Documentation Required: Proof and receipts needed to claim tax benefits for political donations

In India, donations to political parties can be claimed as tax deductions under Section 80GGC of the Income Tax Act, 1961, but only for individuals and Hindu Undivided Families (HUFs). To avail of this benefit, it is crucial to maintain proper documentation, including proof and receipts of the donations made. The first and most essential document required is the official receipt issued by the political party. This receipt must clearly mention the name of the donor, the amount donated, the date of donation, and the name and address of the political party. Without this receipt, the donation cannot be considered valid for tax deduction purposes.

Additionally, the receipt should also bear the registration number of the political party under Section 29A of the Representation of the People Act, 1951. This ensures that the donation has been made to a recognized political party eligible for receiving tax-deductible contributions. It is the donor's responsibility to verify this information before making the donation to avoid any discrepancies during tax filing. Along with the receipt, donors should also maintain a bank statement or other financial records that show the transaction. This could include a cheque number, transaction ID for online payments, or any other proof that confirms the payment has been made from the donor's account.

For donations made in cash, the rules are more stringent. Cash donations exceeding ₹2,000 are not eligible for tax deductions. Therefore, donors must ensure that any cash donations are within this limit and properly documented with a receipt. However, it is advisable to make donations through traceable modes like cheques, demand drafts, or electronic transfers to ensure transparency and ease of verification during tax assessments. Donors should also retain copies of their PAN card and other identification documents, as these may be required to establish the donor's identity and eligibility for claiming the deduction.

Another important aspect is the timing of the donation. The donation must be made during the financial year for which the tax deduction is being claimed. Donors should ensure that the receipt and other documents clearly reflect the financial year in which the donation was made. This is particularly important for donations made close to the end or beginning of a financial year. Maintaining a personal record of all political donations, including the date, amount, and mode of payment, can also be helpful in case of any discrepancies or queries from tax authorities.

Lastly, while filing the income tax return, donors must declare the donation in the appropriate section of the ITR form. For individuals and HUFs, this is typically done under Section 80GGC. It is essential to ensure that the amount declared matches exactly with the amount mentioned in the receipt and other supporting documents. Any mismatch can lead to the disallowance of the deduction or further scrutiny by the tax department. By keeping all these documents organized and readily available, donors can smoothly claim tax benefits for their political donations while remaining compliant with the legal requirements.

Understanding Criticisms of the Democratic Party: Key Issues and Perspectives

You may want to see also

Explore related products

![]()

Corporate vs. Individual: Differences in tax deductions for corporate and individual donors

In India, the tax treatment of donations to political parties differs significantly between corporate and individual donors, reflecting distinct legal and financial frameworks. For individual donors, contributions to registered political parties are eligible for tax deductions under Section 80GGC of the Income Tax Act. This provision allows individuals to claim a deduction for the amount donated, thereby reducing their taxable income. However, it is important to note that this deduction is only applicable if the donation is made via specific modes such as cheque, demand draft, or digital payment—cash donations are not eligible. This rule ensures transparency and traceability in political funding.

In contrast, corporate donors are governed by Section 80GGB of the Income Tax Act. Similar to individual donors, companies can claim a deduction for donations made to registered political parties, but the scope and implications differ. Corporate donations are not subject to the 7.5% cap on corporate social responsibility (CSR) spending, allowing businesses to contribute beyond their CSR obligations. However, the donation must be made through traceable methods like cheques or digital transfers, mirroring the requirements for individuals. This provision encourages corporate participation in political funding while maintaining accountability.

A key difference lies in the reporting and compliance requirements. Individual donors typically report their contributions in their annual income tax returns, with no additional documentation needed beyond proof of payment. Corporate donors, however, must disclose political donations in their financial statements and annual reports, ensuring transparency to stakeholders. Additionally, companies are required to maintain detailed records of such transactions for scrutiny by tax authorities, adding a layer of complexity to their compliance obligations.

Another critical distinction is the absence of donation limits for both corporate and individual donors. Unlike some countries, India does not impose a cap on the amount an individual or corporation can donate to political parties. This lack of restriction allows both entities to contribute significantly, though it also raises concerns about the influence of large donors on political processes. Despite this, the tax deductions remain a consistent benefit, irrespective of the donation size.

Lastly, the impact on taxable income varies based on the donor type. For individuals, the deduction under Section 80GGC directly reduces their taxable income, potentially lowering their tax liability. For corporations, the deduction under Section 80GGB reduces their taxable profits, leading to lower corporate tax outgo. This distinction highlights how the tax benefits are tailored to the financial structures of individuals and companies, ensuring relevance across donor categories.

In summary, while both corporate and individual donors in India enjoy tax deductions for political contributions, the rules governing these deductions differ in terms of eligibility, reporting, and compliance. Understanding these nuances is essential for donors to maximize their tax benefits while adhering to legal requirements, ensuring a transparent and accountable political funding ecosystem.

Are Political Party Donations Tax Exempt? Understanding the Rules

You may want to see also

Frequently asked questions

No, donations to political parties are not tax deductible in India under the Income Tax Act, 1961.

No, contributions to political parties do not qualify for any tax deductions or benefits in India.

No, there is no provision in the Income Tax Act, 1961, that allows tax deductions for donations made to political parties.

No, corporate donations to political parties are also not eligible for tax deductions in India.