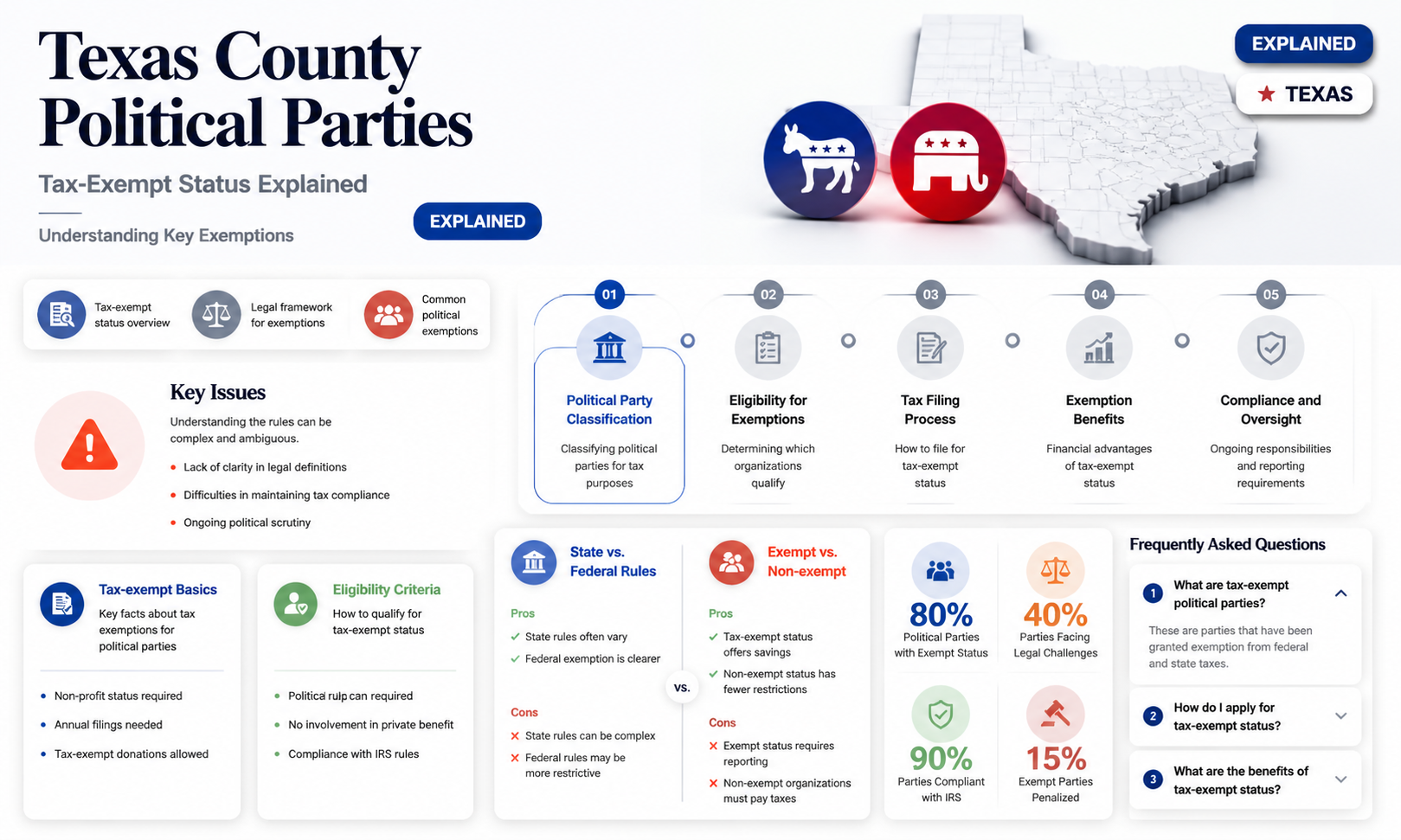

In Texas, county political parties often seek tax-exempt status to manage their finances more effectively, but whether they qualify depends on specific criteria outlined by the Internal Revenue Service (IRS) and state laws. Generally, political organizations, including county parties, may be eligible for tax exemption under Section 527 of the Internal Revenue Code if their primary purpose is to influence the selection, nomination, election, or appointment of individuals to public office. However, to achieve broader tax-exempt status, such as under Section 501(c)(4) as a social welfare organization, they must meet additional requirements, including operating primarily for the promotion of social welfare and not primarily for political campaign intervention. Texas county parties must carefully navigate these regulations, ensuring compliance with both federal and state tax laws to maintain their tax-exempt status while engaging in political activities.

Explore related products

$29.95 $29.95

$8.1 $14.95

What You'll Learn

- IRS 501(c)(4) Status: Do Texas county political parties qualify for social welfare organization tax exemption

- State vs. Federal Laws: How do Texas laws impact federal tax-exempt status for county parties

- Political Activity Limits: Are county parties exempt if they engage in substantial political campaigning

- Filing Requirements: What forms must county parties submit to maintain tax-exempt status

- Donation Rules: Are contributions to tax-exempt county parties considered deductible for donors

![]()

IRS 501(c)(4) Status: Do Texas county political parties qualify for social welfare organization tax exemption?

Texas county political parties, like many political organizations, often seek tax-exempt status to optimize their financial operations. One potential avenue for this exemption is under IRS Section 501(c)(4), which applies to social welfare organizations. However, the qualification criteria for 501(c)(4) status are stringent and may not align with the primary functions of county political parties in Texas. Section 501(c)(4) organizations are primarily formed to promote social welfare, which the IRS defines as benefiting the community as a whole rather than private interests. While political activities are permitted, they cannot be the organization’s primary activity. This distinction is crucial because county political parties in Texas are inherently focused on partisan political activities, such as candidate endorsements, voter mobilization, and campaign support, which may disqualify them from 501(c)(4) status.

To qualify for 501(c)(4) status, an organization must demonstrate that its primary purpose is the promotion of social welfare. This includes activities like community improvement, education, or charitable work. County political parties in Texas, however, are typically structured to advance the interests of a specific political party, which does not inherently qualify as social welfare under IRS guidelines. While these parties may engage in some community-oriented activities, such as voter registration drives or local advocacy, their core mission remains political in nature. The IRS requires that social welfare activities be the organization’s primary focus, and the political nature of county parties often places them outside this framework.

Another critical factor is the IRS’s treatment of political campaign intervention. Under 501(c)(4) rules, organizations can engage in political activities, including lobbying and supporting candidates, but these activities cannot constitute their primary purpose. For county political parties in Texas, whose primary function is to support candidates and advance party agendas, this presents a significant hurdle. The IRS scrutinizes organizations to ensure they are not primarily engaged in political campaigns, and county parties may struggle to meet this standard. While some parties may attempt to structure their activities to comply with 501(c)(4) requirements, the inherent political focus of their operations often makes this difficult.

Despite these challenges, some Texas county political parties may explore alternative tax-exempt statuses, such as 527 organizations, which are specifically designed for political organizations. Unlike 501(c)(4) organizations, 527s are taxed on their political expenditures but are not subject to the same restrictions on political activities. This status may be more suitable for county parties, as it allows them to openly engage in political campaigning without violating IRS rules. However, 527 organizations do not enjoy the same broad tax exemptions as 501(c)(4) organizations, which may influence a party’s decision.

In conclusion, while IRS 501(c)(4) status offers tax exemption for social welfare organizations, Texas county political parties are unlikely to qualify due to their primary focus on partisan political activities. The IRS’s requirement that social welfare be the organization’s main purpose, coupled with restrictions on political campaign intervention, makes 501(c)(4) status a poor fit for these entities. Instead, county parties may find more flexibility under 527 organization status, which aligns better with their political objectives. Parties considering tax-exempt status should carefully evaluate their activities and consult legal or tax professionals to determine the most appropriate classification.

Is the Alternative for Germany a Neo-Nazi Political Party?

You may want to see also

Explore related products

$34.59 $40.95

![]()

State vs. Federal Laws: How do Texas laws impact federal tax-exempt status for county parties?

In the United States, the tax-exempt status of political organizations, including county political parties in Texas, is primarily governed by federal law, specifically the Internal Revenue Code (IRC). Under federal law, political organizations can qualify for tax exemption under Section 527 of the IRC, which allows them to be exempt from federal income tax on certain types of income. However, this federal exemption does not automatically grant exemption from state taxes, and the interplay between state and federal laws can significantly impact the overall tax status of these organizations. Texas, like other states, has its own tax laws and regulations that may differ from federal provisions, creating a layered compliance requirement for county political parties.

Texas law does not directly grant or deny tax-exempt status to county political parties; instead, it defers to federal classifications for most tax purposes. This means that if a county political party in Texas qualifies as a tax-exempt organization under federal law (e.g., Section 527), it will generally be treated as tax-exempt for Texas state tax purposes as well. However, Texas imposes additional reporting and compliance requirements that federal law does not. For instance, political organizations in Texas must file specific reports with the Texas Ethics Commission and adhere to state campaign finance laws, which can indirectly affect their federal tax-exempt status if violations occur. These state-level obligations underscore the importance of understanding both federal and state laws to maintain tax-exempt status.

One critical area where Texas laws impact federal tax-exempt status is in the regulation of political activities. While federal law allows Section 527 organizations to engage in political campaign activities, Texas imposes stricter rules on how county parties can operate. For example, Texas law prohibits certain types of coordination between county parties and candidate campaigns, and violations of these rules can lead to penalties or loss of state tax benefits. If such violations are severe enough, they could also jeopardize the organization's federal tax-exempt status, as the IRS may view non-compliance with state laws as evidence of improper political activity under federal regulations.

Another key difference lies in the treatment of fundraising and expenditures. Federal law permits Section 527 organizations to raise and spend funds for political purposes, but Texas law adds layers of transparency and reporting requirements. County parties in Texas must disclose detailed financial information to state authorities, and failure to comply can result in state penalties. While these state requirements do not directly revoke federal tax-exempt status, they create an additional compliance burden that organizations must navigate to avoid indirect consequences. For example, inconsistent reporting between state and federal filings could trigger IRS scrutiny, potentially endangering the organization's federal tax exemption.

Finally, Texas laws can impact federal tax-exempt status through their influence on an organization's structure and governance. Federal law requires tax-exempt political organizations to operate exclusively for political purposes and avoid prohibited activities like lobbying or excessive private benefits. Texas law, however, may impose additional restrictions on how county parties are organized and managed. If a county party fails to meet these state-specific requirements, it could face state penalties that, in turn, raise red flags for federal regulators. Thus, while federal law sets the baseline for tax exemption, Texas laws create a parallel framework that county parties must carefully navigate to maintain their tax-exempt status at both levels.

In summary, while federal law governs the tax-exempt status of county political parties in Texas, state laws play a significant role in shaping their compliance obligations and overall tax treatment. Texas imposes additional reporting, transparency, and operational requirements that, if not met, can indirectly threaten federal tax-exempt status. County parties must therefore be diligent in adhering to both federal and state regulations to ensure they remain in good standing and avoid penalties that could compromise their tax exemption. Understanding this interplay between state and federal laws is essential for effectively managing the tax status of county political parties in Texas.

Gerrymandering: A Bipartisan Practice Shaping America's Political Landscape

You may want to see also

Explore related products

$24.96 $49.99

$14.99 $24.95

![]()

Political Activity Limits: Are county parties exempt if they engage in substantial political campaigning?

In Texas, county political parties often seek tax-exempt status under Section 527 of the Internal Revenue Code, which applies to political organizations. However, the question of whether they remain exempt when engaging in substantial political campaigning is critical. The IRS defines a Section 527 organization as one primarily involved in influencing or attempting to influence the selection, nomination, election, or appointment of any individual to public office. While this classification allows for tax exemption, it also imposes limitations on the types of activities these organizations can undertake without jeopardizing their status.

When county political parties in Texas engage in substantial political campaigning, they must navigate strict guidelines to maintain their tax-exempt status. The IRS allows Section 527 organizations to participate in political campaigns, but such activities must not constitute their primary function. For county parties, this means balancing campaign efforts with other permissible activities, such as voter education, candidate recruitment, and party building. If campaigning becomes the dominant focus, the organization risks losing its tax-exempt status, as it would no longer meet the IRS’s criteria for a political organization under Section 527.

Another key consideration is the source and use of funds. Tax-exempt county parties must ensure that funds are not used exclusively for political campaigns, as this could trigger taxable treatment. Instead, they should allocate resources to a mix of activities, including those that support the party’s broader mission. For instance, funds can be directed toward training volunteers, organizing community events, or conducting voter registration drives. By diversifying their activities, county parties can demonstrate compliance with IRS regulations and maintain their tax-exempt status.

Additionally, Texas law aligns with federal regulations in requiring transparency and accountability from political organizations. County parties must file regular reports with the IRS, detailing their income, expenditures, and activities. These filings help ensure that substantial political campaigning does not overshadow other permissible functions. Failure to comply with reporting requirements can result in penalties or loss of tax-exempt status, underscoring the importance of meticulous record-keeping and adherence to both state and federal guidelines.

In conclusion, while county political parties in Texas can engage in substantial political campaigning, they must do so judiciously to preserve their tax-exempt status. By balancing campaign activities with other party-building efforts, maintaining diverse funding sources, and adhering to reporting requirements, these organizations can remain compliant with IRS regulations. Understanding and respecting these political activity limits is essential for county parties to continue operating as tax-exempt entities while effectively supporting their candidates and causes.

Do Political Parties in India Pay Taxes? Exploring the Legal Framework

You may want to see also

Explore related products

![]()

Filing Requirements: What forms must county parties submit to maintain tax-exempt status?

In Texas, county political parties that seek to maintain their tax-exempt status must adhere to specific filing requirements outlined by both state and federal regulations. These organizations are typically classified under Section 527 of the Internal Revenue Code, which governs political organizations. To remain tax-exempt, county parties must file Form 8871, Political Organization Notice of Section 527 Status, with the IRS. This form is required for any political organization that anticipates raising or spending more than $25,000 in a taxable year. Filing Form 8871 ensures compliance with federal tax laws and provides transparency regarding the organization's financial activities.

Additionally, county political parties in Texas must file Form 8872, Political Organization Report of Contributions and Expenditures, on a periodic basis. This form details the contributions received and expenditures made by the organization. The frequency of filing—whether monthly, quarterly, or annually—depends on the organization's activity level and the thresholds set by the IRS. Accurate and timely submission of Form 8872 is critical to maintaining tax-exempt status and avoiding penalties for non-compliance.

At the state level, county parties must also comply with Texas Ethics Commission (TEC) requirements. This includes filing Campaign Finance Reports to disclose contributions and expenditures. While these reports are primarily for state compliance, they often align with federal reporting requirements, ensuring consistency across jurisdictions. Failure to file these reports can result in fines, loss of tax-exempt status, or other legal consequences.

Another key filing requirement is the Annual Return (Form 990 series) with the IRS, depending on the organization's income. While some smaller political organizations may be exempt from filing Form 990, those with gross receipts exceeding $200,000 or total assets exceeding $500,000 must file either Form 990, Form 990-EZ, or Form 990-N (e-Postcard). This annual return provides a comprehensive overview of the organization's financial health and ensures continued compliance with tax-exempt regulations.

Lastly, county parties must maintain detailed records of their financial transactions, including contributions, expenditures, and fundraising activities. These records must be retained for at least four years and made available for inspection by the IRS or state authorities upon request. Proper record-keeping is essential not only for filing accurate reports but also for demonstrating compliance during audits or investigations. By adhering to these filing requirements, county political parties in Texas can maintain their tax-exempt status and operate within the bounds of the law.

Vijay's Political Move: Has the Actor Launched a New Party?

You may want to see also

Explore related products

![]()

Donation Rules: Are contributions to tax-exempt county parties considered deductible for donors?

In Texas, county political parties often operate under specific tax-exempt statuses, which can significantly impact the deductibility of contributions made by donors. Generally, political organizations, including county parties, are classified under Section 527 of the Internal Revenue Code (IRC). However, for contributions to be tax-deductible, the organization must qualify under Section 501(c)(3) or another provision that allows for charitable deductions. County political parties in Texas typically do not fall under 501(c)(3) status, as they are primarily engaged in political activities rather than charitable, educational, or religious purposes.

Donors should be aware that contributions to county political parties in Texas are generally not tax-deductible. The IRS clearly states that donations to political parties, candidates, or campaign committees are not eligible for charitable deductions. This is because these contributions are considered political in nature and do not meet the criteria for charitable contributions as defined by the IRS. Therefore, individuals or businesses making donations to county political parties should not expect to claim these contributions as deductions on their federal tax returns.

While federal tax rules are clear on the non-deductibility of political contributions, it’s important to note that Texas state tax laws may have different provisions. However, Texas follows federal guidelines for charitable deductions, meaning contributions to county political parties are also not deductible on state tax returns. Donors should consult with a tax professional to understand any state-specific nuances, but the general rule remains consistent: political donations are not tax-deductible.

For donors interested in supporting county political parties, it’s crucial to understand the nature of their contributions. These donations are considered voluntary investments in political activities rather than charitable gifts. Donors may still choose to contribute for ideological or personal reasons, but they should not anticipate any tax benefits. Transparency in fundraising practices is essential for county parties to ensure donors are fully informed about the non-deductible nature of their contributions.

In summary, contributions to tax-exempt county political parties in Texas are not considered deductible for donors under federal or state tax laws. These donations are classified as political contributions, which do not qualify for charitable deductions. Donors should approach such contributions with the understanding that they are supporting political activities without any tax advantages. Always consult a tax advisor for personalized guidance on the implications of political donations.

Are Political Party Donations Tax-Deductible? What You Need to Know

You may want to see also

Frequently asked questions

Yes, county political parties in Texas are generally tax exempt under Section 527 of the Internal Revenue Code, which applies to political organizations.

County political parties in Texas are exempt from federal income tax and may also qualify for state sales tax exemptions on certain purchases related to their political activities.

Yes, county political parties must file IRS Form 8872 annually to report their financial activities and maintain their tax-exempt status under Section 527.

![[3-Pack] Disco Ball DJ Party Lights Sound Activated with Remote Control Strobe Lamp 7 Modes Stage Light for Home Room Dance Parties Karaoke Halloween Christmas Birthday Decorations](https://m.media-amazon.com/images/I/71CXY4TVTCL._AC_UY218_.jpg)