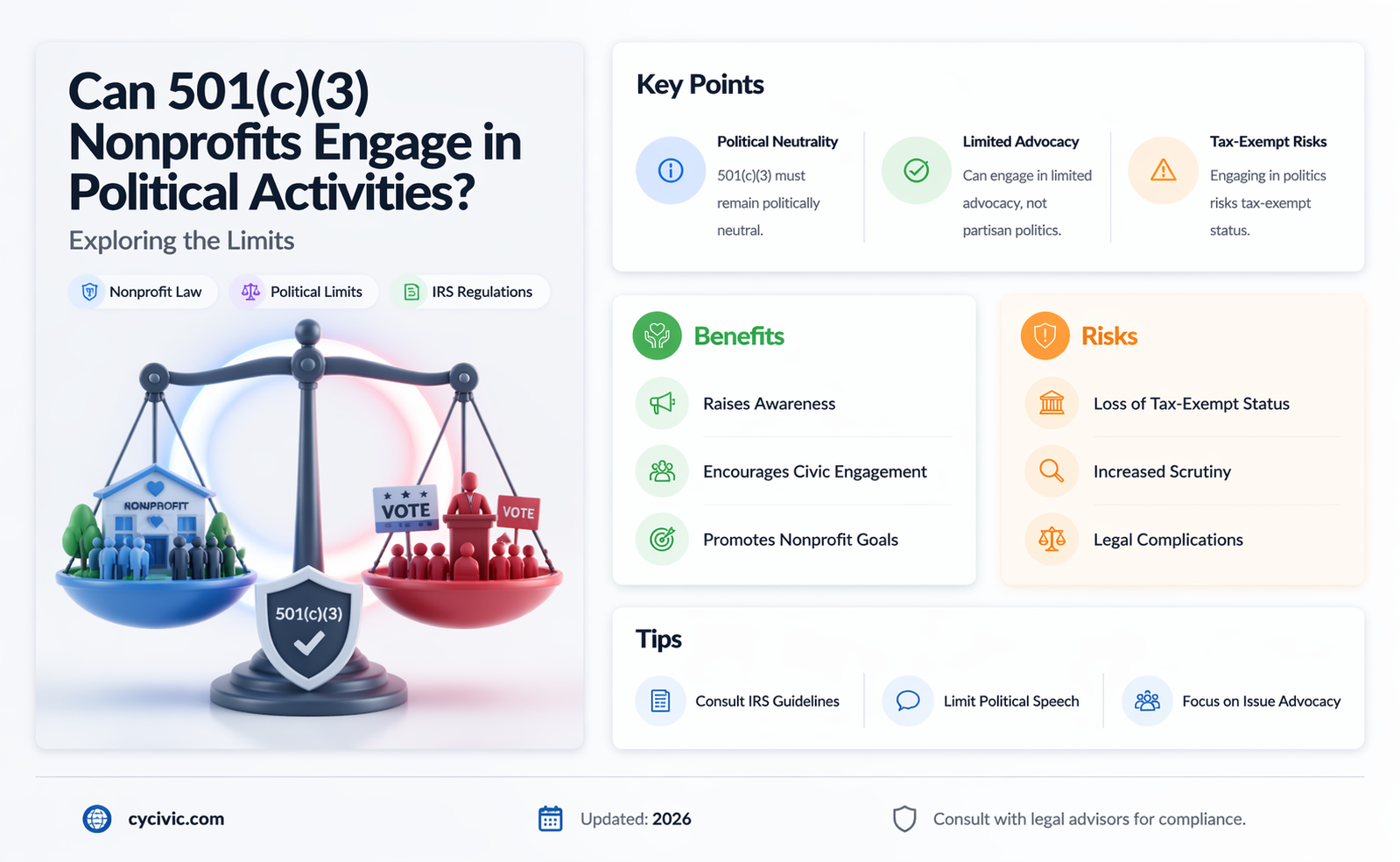

The question of whether 501(c)(3) organizations are political is a nuanced and often debated topic. Under U.S. tax law, 501(c)(3) organizations are primarily charitable, religious, educational, or scientific entities that enjoy tax-exempt status and the ability to receive tax-deductible donations. While these organizations are prohibited from engaging in substantial political campaign activities, such as endorsing or opposing candidates, they are permitted to participate in limited lobbying and advocacy efforts related to their mission. This distinction often blurs the line between permissible issue-based advocacy and impermissible political intervention, leading to confusion and scrutiny. As a result, understanding the boundaries of political involvement for 501(c)(3) organizations is crucial for both compliance and effective mission fulfillment.

| Characteristics | Values |

|---|---|

| Political Activity Allowed | Limited; 501(c)(3) organizations can engage in some political activities but cannot endorse or oppose candidates. |

| Lobbying Restrictions | Permitted but must be insubstantial compared to overall activities; excessive lobbying can jeopardize tax-exempt status. |

| Voter Education | Allowed, provided it is non-partisan and does not favor any candidate or party. |

| Endorsements | Prohibited; endorsing or opposing political candidates can result in loss of tax-exempt status. |

| Campaign Contributions | Prohibited; 501(c)(3) organizations cannot contribute to political campaigns. |

| Issue Advocacy | Allowed; organizations can advocate for or against specific issues, but not candidates. |

| Tax-Exempt Status | Maintained as long as political activities are limited and do not become the primary focus. |

| Public Perception | Often perceived as non-political due to restrictions, but can engage in issue-based advocacy. |

| IRS Oversight | Subject to IRS scrutiny to ensure compliance with political activity limitations. |

| Examples of Permissible Activities | Non-partisan voter registration drives, issue-based advocacy campaigns, and public education on policy matters. |

| Examples of Prohibited Activities | Endorsing candidates, donating to political campaigns, or distributing partisan materials. |

Explore related products

What You'll Learn

- IRS Rules on Advocacy: Limits on lobbying and political campaign intervention for 501(c)(3) organizations

- Grassroots Lobbying: Permitted activities and restrictions for 501(c)(3)s in grassroots advocacy efforts

- Electioneering Ban: Prohibition of 501(c)(3)s from supporting or opposing political candidates

- Nonpartisan Education: How 501(c)(3)s can engage in voter education without political bias

- Consequences of Violation: Penalties for 501(c)(3)s that engage in prohibited political activities

![]()

IRS Rules on Advocacy: Limits on lobbying and political campaign intervention for 501(c)(3) organizations

C)(3) organizations, often referred to as charities, are primarily established for religious, educational, charitable, scientific, or literary purposes. While these organizations play a vital role in addressing societal needs, their involvement in political activities is strictly regulated by the Internal Revenue Service (IRS). The IRS imposes clear limits on lobbying and political campaign intervention to maintain the tax-exempt status of these entities. Understanding these rules is crucial for organizations to navigate their advocacy efforts without jeopardizing their nonprofit status.

Lobbying Limits: The 501(h) Election

For 501(c)(3) organizations, lobbying is not entirely prohibited but is subject to strict limitations. The IRS allows two methods to measure lobbying activities: the "insubstantial part" test and the 501(h) expenditure test. The insubstantial part test is vague and risky, as it does not provide clear thresholds. In contrast, the 501(h) election offers a more defined framework. By making this election, organizations can spend a specific percentage of their annual exempt purpose expenditures on lobbying, with the limit increasing based on their budget size. For example, organizations with expenditures under $500,000 can spend up to 20% of that amount on lobbying, while those with expenditures exceeding $17 million can spend $1 million plus 5% of the excess over $17 million. This election provides clarity and reduces the risk of exceeding IRS limits.

Political Campaign Intervention: Absolute Prohibition

Unlike lobbying, political campaign intervention is entirely off-limits for 501(c)(3) organizations. This includes endorsing or opposing candidates for public office, contributing to political campaigns, or engaging in any activity that favors or disadvantages a candidate. Even subtle actions, such as distributing materials that implicitly support a candidate or using organizational resources for campaign-related activities, can trigger IRS scrutiny. For instance, a charity cannot allow a candidate to use its facility for a campaign event, even if the same opportunity is offered to all candidates, without potentially violating these rules. The prohibition is absolute, and violations can result in penalties, including loss of tax-exempt status.

Practical Tips for Compliance

To ensure compliance, 501(c)(3) organizations should adopt clear policies and procedures governing advocacy activities. First, consider making the 501(h) election to gain clarity on lobbying limits. Second, train staff and volunteers to recognize the difference between permissible advocacy and prohibited political activities. Third, maintain detailed records of all advocacy efforts, including expenditures and activities, to demonstrate compliance during IRS audits. Finally, consult legal counsel when in doubt about the permissibility of specific actions. Proactive measures can help organizations maximize their advocacy impact while staying within IRS boundaries.

The Balancing Act: Advocacy vs. Politics

While the IRS rules may seem restrictive, they are designed to preserve the integrity of 501(c)(3) organizations as nonpartisan entities focused on their charitable missions. Advocacy, when conducted within these limits, can be a powerful tool for driving social change. For example, a health-focused charity can lobby for policies that improve access to healthcare without endorsing a specific candidate. By understanding and adhering to these rules, organizations can effectively engage in advocacy while maintaining their tax-exempt status and public trust. The key lies in striking a balance between pursuing policy goals and avoiding political entanglements.

Understanding International Politics: Key Concepts and Defining Frameworks

You may want to see also

Explore related products

![]()

Grassroots Lobbying: Permitted activities and restrictions for 501(c)(3)s in grassroots advocacy efforts

C)(3) organizations, often referred to as nonprofits, are primarily known for their charitable, educational, or religious missions. However, they are not entirely barred from engaging in political activities. The key lies in understanding the distinction between lobbying and political campaign intervention. While 501(c)(3)s are strictly prohibited from participating in political campaigns or endorsing candidates, they can engage in lobbying, provided it is not their primary activity. Grassroots lobbying, in particular, allows these organizations to mobilize public support for or against specific legislation, but it comes with strict rules and limitations.

Grassroots lobbying involves encouraging the general public to contact legislators about pending legislation. For 501(c)(3)s, this activity is permitted but must be conducted within IRS-defined boundaries. The IRS employs a two-pronged test to determine if an activity qualifies as grassroots lobbying: the communication must refer to specific legislation, and it must reflect a view on that legislation. For example, a nonprofit advocating for environmental protection can urge its supporters to contact their representatives about a bill related to clean water regulations. However, the organization must avoid using inflammatory language or making direct calls to action that could be construed as partisan.

One critical restriction for 501(c)(3)s is the "no substantial part" test, which limits the amount of lobbying they can engage in. While there is no specific percentage cap, exceeding a reasonable threshold can jeopardize their tax-exempt status. To stay compliant, organizations often track their lobbying expenditures and ensure they remain a minor part of their overall activities. Additionally, 501(c)(3)s must refrain from using public funds, such as grants or donations, for lobbying efforts unless explicitly permitted by the funding source. This requires careful budgeting and transparency in financial reporting.

Practical tips for 501(c)(3)s engaging in grassroots lobbying include clearly separating advocacy materials from educational content, avoiding direct calls to contact legislators in mass communications, and providing balanced information on legislative issues. For instance, instead of saying, "Tell your senator to vote no on this bill," an organization might say, "Learn more about how this bill could impact our community and consider sharing your concerns with your representative." This approach ensures compliance while still empowering supporters to take action.

In conclusion, grassroots lobbying is a powerful tool for 501(c)(3)s to influence policy and advance their missions, but it requires careful navigation of IRS rules. By understanding permitted activities, adhering to restrictions, and implementing practical strategies, nonprofits can effectively engage in advocacy without risking their tax-exempt status. This balance allows them to remain politically active while staying true to their charitable purpose.

Capitalizing Identity Politics: Rules, Respect, and Representation Explained

You may want to see also

Explore related products

$125 $123

![]()

Electioneering Ban: Prohibition of 501(c)(3)s from supporting or opposing political candidates

C)(3) organizations, commonly known as charities, are prohibited by law from engaging in electioneering activities. This means they cannot support or oppose political candidates, a restriction rooted in the Internal Revenue Code. The ban ensures that tax-exempt entities remain focused on their charitable missions rather than becoming vehicles for political influence. Violating this rule can result in severe penalties, including loss of tax-exempt status and potential excise taxes.

Consider the practical implications for a 501(c)(3) organization. Suppose a nonprofit dedicated to environmental advocacy wants to endorse a candidate who champions green policies. Despite the alignment of values, the organization cannot publicly back the candidate, even through subtle means like sharing campaign materials or using organizational resources for political ads. The IRS scrutinizes activities closely, and actions like these would likely trigger an audit or enforcement action.

The electioneering ban also extends to less obvious actions. For instance, a nonprofit leader cannot use their title or organizational email to endorse a candidate, even in personal communications. Similarly, hosting a political rally or fundraiser at the nonprofit’s facility, even if rented, could be seen as indirect support. Organizations must carefully navigate these boundaries, often consulting legal counsel to ensure compliance.

Critics argue the ban stifles free speech, while proponents maintain it preserves the integrity of nonprofits and taxpayer trust. A middle ground often involves 501(c)(3)s engaging in nonpartisan voter education or advocacy on issues, which is permitted. For example, a nonprofit can host a candidate forum as long as all viable candidates are invited and treated equally. This distinction—between issue advocacy and candidate endorsement—is critical for staying within legal bounds.

In practice, organizations can still influence policy by lobbying, but only within limits. The "substantial part test" restricts lobbying to a small portion of overall activities. Pairing this with the electioneering ban creates a framework where nonprofits can advocate for systemic change without becoming political actors. For instance, a health-focused nonprofit can lobby for healthcare legislation but cannot endorse a candidate who supports the same policies.

Ultimately, the electioneering ban serves as a guardrail for 501(c)(3)s, ensuring they remain mission-driven rather than politically motivated. While it requires careful navigation, it also fosters public trust by keeping charities above the fray of partisan politics. Organizations that adhere to these rules not only maintain their tax-exempt status but also strengthen their credibility as impartial agents of social good.

Equality's Role in Shaping Political Decisions and Societal Progress

You may want to see also

Explore related products

![]()

Nonpartisan Education: How 501(c)(3)s can engage in voter education without political bias

C)(3) organizations, by law, must remain nonpartisan to maintain their tax-exempt status. Yet, they can—and should—play a vital role in voter education, a cornerstone of democratic engagement. The challenge lies in navigating the fine line between informing the public and endorsing political candidates or agendas. To achieve this, organizations must focus on issues, not ideologies, and on processes, not parties. For instance, explaining how a ballot initiative works or detailing the mechanics of voter registration is inherently nonpartisan. These efforts empower citizens to participate in democracy without steering them toward any particular political outcome.

One effective strategy for 501(c)(3)s is to adopt a strictly educational framework that emphasizes civic literacy. This involves creating resources that break down complex political processes into digestible, unbiased information. For example, a nonprofit could develop a voter guide that outlines the steps to cast a ballot, explains the roles of elected officials, or provides a glossary of political terms. Such materials should avoid loaded language and focus on factual accuracy. Additionally, hosting workshops or webinars on topics like the history of voting rights or the structure of local government can engage audiences without crossing partisan lines.

Another key approach is to partner with diverse community groups to amplify reach and credibility. By collaborating with organizations that represent various demographics, 501(c)(3)s can ensure their voter education efforts are inclusive and culturally relevant. For instance, a nonprofit might work with local schools, faith-based groups, or civic leagues to distribute voter information in multiple languages or tailor content to address specific community concerns. This collaborative model not only broadens impact but also reinforces the nonpartisan nature of the initiative by demonstrating a commitment to serving all citizens equally.

However, organizations must remain vigilant to avoid even the appearance of bias. This means scrutinizing every piece of content, event, or partnership for potential political undertones. For example, inviting speakers from both sides of an issue or providing balanced resources on contentious topics can help maintain impartiality. Similarly, tracking and documenting all activities ensures transparency and accountability, which are essential for preserving trust and compliance with IRS regulations.

In conclusion, 501(c)(3)s have a unique opportunity to strengthen democracy through nonpartisan voter education. By focusing on civic literacy, leveraging community partnerships, and maintaining rigorous standards of impartiality, these organizations can empower voters without compromising their tax-exempt status. The key lies in staying rooted in facts, processes, and inclusivity—principles that transcend politics and serve the public good.

Does PBS Enhance Political Knowledge? Exploring Public Broadcasting's Impact

You may want to see also

Explore related products

![]()

Consequences of Violation: Penalties for 501(c)(3)s that engage in prohibited political activities

C)(3) organizations, granted tax-exempt status by the IRS, are prohibited from engaging in substantial political activities. This restriction is rooted in the Johnson Amendment of 1954, which aims to maintain the integrity of charitable organizations by preventing them from becoming vehicles for political campaigns. Violating this rule triggers severe consequences, ranging from financial penalties to the potential loss of tax-exempt status. Understanding these penalties is crucial for any 501(c)(3) to ensure compliance and protect its mission.

The IRS employs a spectrum of penalties for political violations, starting with corrective measures and escalating to more severe actions. For minor infractions, such as inadvertent political statements, the IRS may issue a warning or require the organization to take corrective steps, like retracting the statement or educating staff on compliance. However, repeated or deliberate violations can lead to excise taxes imposed on the organization and its managers. These taxes, outlined in Section 4955 of the Internal Revenue Code, can amount to 10% of the expenditure for the first violation and 100% for subsequent violations, creating a significant financial burden.

The most drastic consequence for a 501(c)(3) engaging in prohibited political activities is the revocation of its tax-exempt status. This penalty is reserved for organizations that engage in substantial or repeated political campaigning. Losing tax-exempt status not only exposes the organization to corporate income tax but also jeopardizes its ability to receive tax-deductible donations, which are often critical to its survival. For example, the IRS revoked the tax-exempt status of a church in 1995 after it took out newspaper ads opposing a political candidate, setting a precedent for enforcement.

Beyond IRS penalties, 501(c)(3)s face reputational damage and loss of donor trust when involved in political controversies. Donors, who often contribute based on an organization’s nonpartisan mission, may withdraw support if they perceive political bias. Additionally, state attorneys general may investigate and penalize organizations for violating state laws governing nonprofits. For instance, a California-based charity could face state-level fines or legal action if found to be engaging in political activities prohibited under both federal and state law.

To avoid these consequences, 501(c)(3)s must implement robust compliance measures. This includes training staff and volunteers on the boundaries of permissible advocacy versus prohibited political activity, maintaining clear policies, and seeking legal counsel when in doubt. Organizations can engage in issue advocacy, voter education, and lobbying within strict limits, but they must avoid endorsing or opposing candidates or political parties. Proactive compliance not only safeguards tax-exempt status but also preserves the organization’s credibility and mission-driven impact.

Polite Order Cancellation: A Step-by-Step Guide to Refunding Gracefully

You may want to see also

Frequently asked questions

501(c)(3) organizations are prohibited from engaging in substantial political campaign activities, such as endorsing or opposing candidates for public office. However, they can engage in limited lobbying and non-partisan voter education activities.

If a 501(c)(3) organization violates the political activity rules, it risks losing its tax-exempt status. The IRS may impose penalties or revoke the organization’s 501(c)(3) designation, which can have significant financial and legal consequences.

501(c)(3) organizations can engage in limited lobbying activities to support or oppose legislation, as long as such activities are not a substantial part of their overall operations. They cannot, however, directly or indirectly participate in political campaigns.